INTRODUCTION

The year 2016 began with unsettling volatility in financial markets, fueled by fears – perhaps overwrought – of at least a partial global economic slowdown. This notion itself was sparked, in part, by declining oil and other commodities, often attributed to a slowing growth rate in China. Yet macroeconomic forecasts, for the most part, have remained remarkably stable.

The global economy is projected to grow between 2.7 percent to 3.6 percent this year, marginally higher than 2015. Still, volatility in the financial markets could create drag on the real economy: the question is how much. In view of such uncertainty, procurement leaders need to stay on top of business conditions and determine the implications for their role. In this report, we have identified five supertrends that will impact global business dynamics and help determine the agenda for procurement leaders at global organizations over the next year.

TABLE OF CONTENTS

SUPER TRENDS FOR 2016

IMPLICATIONS FOR PROCUREMENT LEADERSHIP

SUMMARY OF TRENDS AND IMPLICATIONS

CATEGORY TRENDS

Business Services – Travel

Business Services – Human Resources

Energy & Utilities

Facilities Management

Information Technology

Telecom

Logistics

CAPEX & Construction

Maintenance, Repair & Operations (MRO)

Packaging

Marketing – Advertising & Digital Agencies

SUPERTRENDS FOR 2016 AND THEIR IMPLICATIONS FOR PROCUREMENT LEADERS

Heightened Impact of Geopolitics

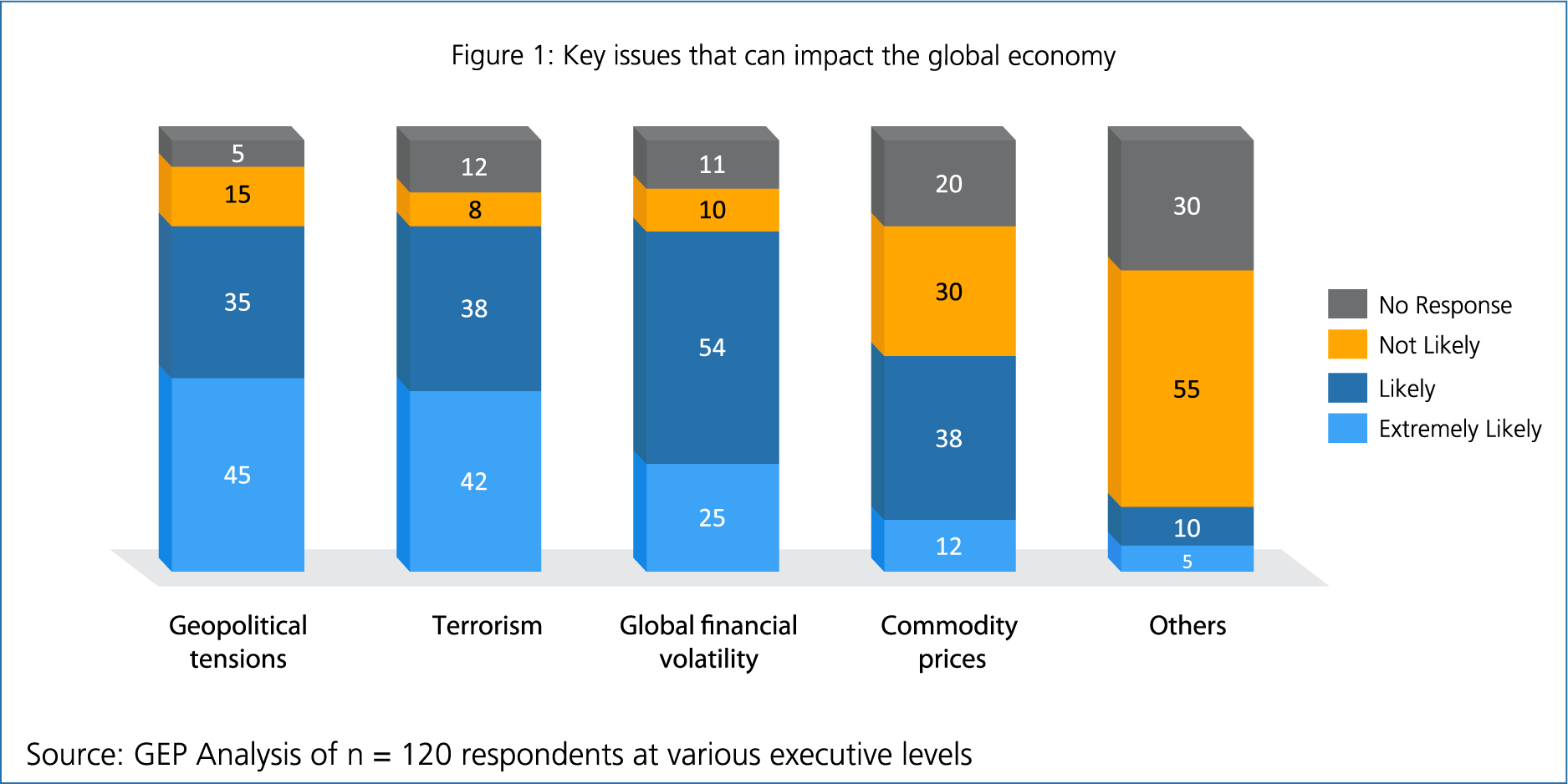

A recent GEP study of global executives conducted on issues that can potentially impact the global economy clearly indicates that geopolitical instability and terrorism are top-of-the-mind concerns (See Figure 1).

Since 2008, regional powers have increased their political influence and played a larger role on the world stage. In addition, these rising economic powers are creating new institutions that reinforce their expanding economic clout and political ambitions — the New Development Bank (formerly the BRICS Bank) is a case in point.

At the same time, the perception of rising violent extremism is dampening global political and economic integration. Regional conflicts have mushroomed, triggering involuntary mass migrations, heightened nationalism, as well as the closing of borders and imposition of travel restrictions.

According to the World Economic Forum’s (WEF) most recent Global Risks Perception Survey, the greatest likely risk in 2016 is continued large-scale involuntary migration. Experts at the WEF said that events, such as the refugee crisis in Europe and terrorist attacks worldwide have increased the global political instability to its highest point since the Cold War, intensifying the atmosphere of uncertainty in which global enterprises will make their strategic decisions. Thus, it is even more important for business leaders to consider the impact of these risks on their company’s reputation, footprint and supply chain.

In 2016, we believe geopolitical instability will translate into greater supply chain risks, with implications on everything from labor markets to air and ocean shipping. In addition, we anticipate governments worldwide will adopt more nationalistic postures, which have the potential to spill over into the business sector. This would be reflected in increased protectionism in key industries and sectors around the world.

Shift of Economic Power to the U.S. and to the ‘New’ Emerging Economies

The crash in the Chinese stock market, at the very outset of 2016, reflected decreasing confidence in China’s ability to quickly revive its slowing economy. While a slowdown in China will certainly impact overall global growth, we believe that the U.S. economy will remain resurgent and this will somewhat mitigate the impact of global headwinds in the United States and economies closely linked to it. Recent consensus predictions for U.S. economic growth range between 2.5 percent to 3.0 percent in 2016.

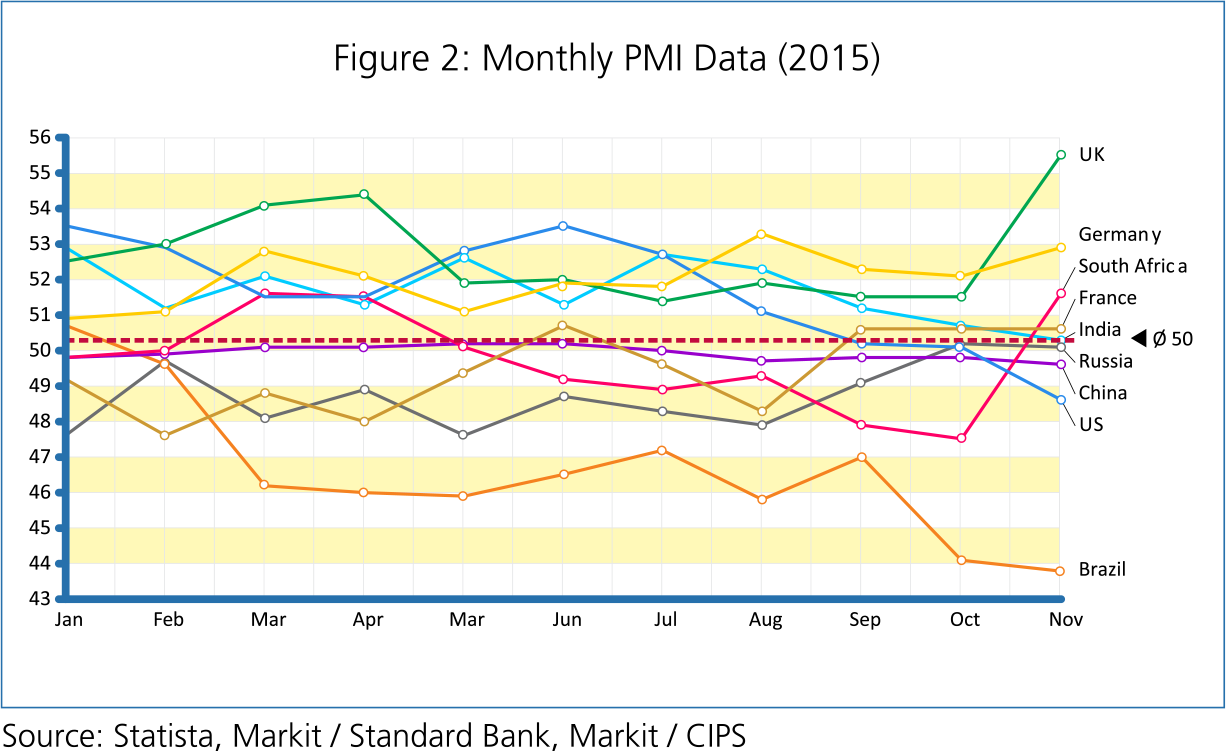

The emerging markets’ share of global GDP grew to almost 57 percent in 2015. To date, emerging market growth has been dominated by the BRICS (Brazil, Russia, India, China and South Africa) nations; but this does not appear likely over the next few years. In fact, among the BRICS, only India and South Africa show optimism as reflected in the Purchasing Managers Index (PMI) trend (see Figure 2). China, Russia and Brazil all show pessimism, with Brazil being the worst of the lot.

However, there are new ‘frontier economies’, such as Malaysia, Poland, Philippines, Mexico and the Sub-Saharan Africa, that are now accelerating and providing the next level of economic growth among emerging markets. While they are nowhere close to the BRICS nations in terms of size or growth rates, they will be the economies to watch out for in the longer term.

In 2016, the growth in the U.S. economy will provide opportunities to many businesses. A stronger dollar will lower the cost of imports but will erode export competitiveness. At the same time, higher domestic demand and lower energy costs will be a big boost for the U.S. manufacturing industry. Similarly, the emerging markets will continue to offer a variety of business opportunities. Despite slower growth, many markets — including BRICS — will offer opportunities to sell to a growing middle-class consumer group. These economies will also bring challenges in the form of increasing diversity.

Continued Decline in Global Commodity Prices

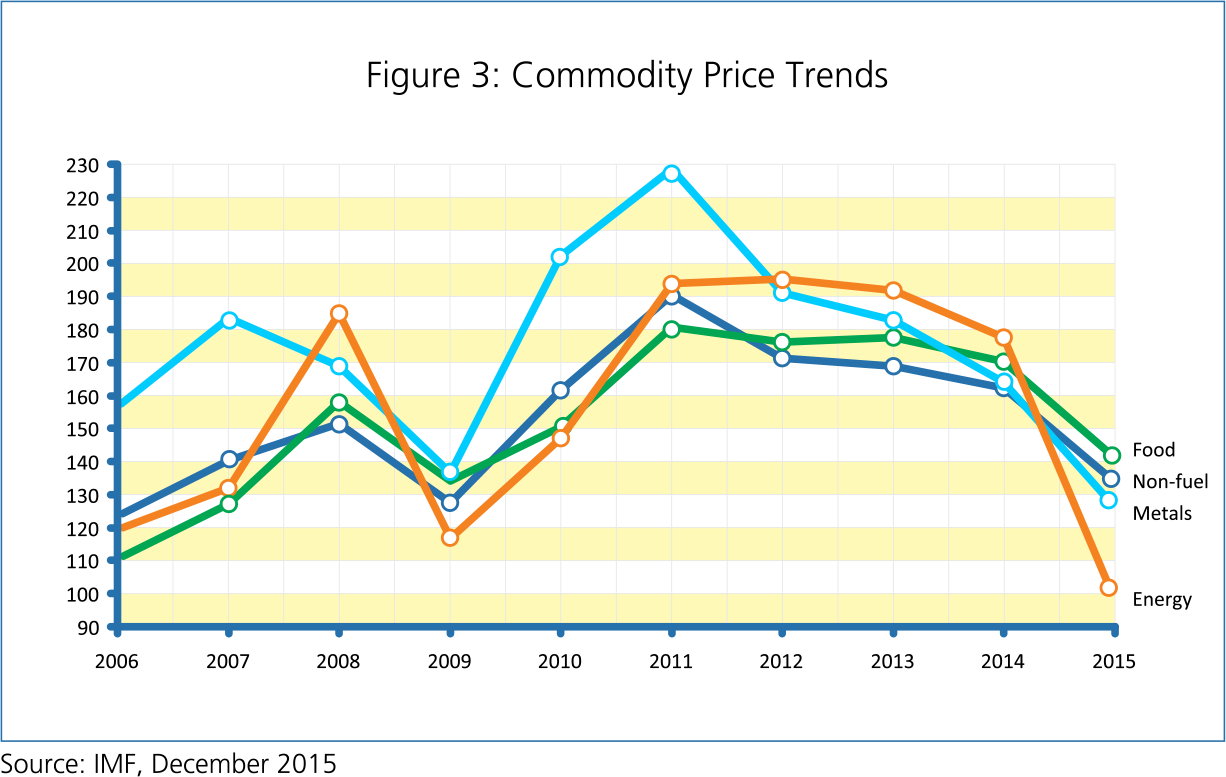

The global economy has hit a ‘resource slump’ as seen by the dramatic drop in oil prices. The resource slump is also characterized by drops in prices of metals and food (see Figure 3).

The decline in commodity prices has been driven by both supply- and demand-side factors. Rising production of oil enabled by new technologies, the impact of Iran’s re-entry to world markets, and sustained production levels by OPEC members have all contributed to supply-side factors.

On the demand side, China’s slowdown has reduced the import demand for oil. The IMF and World Bank expect the slump to continue until the end of this decade. The slump in commodity prices will have a strong impact on economies driven by commodity exports, including Russia, Venezuela, Middle Eastern economies and North African countries.

Still, overall, we expect the global economy to benefit from the lower commodity prices, generating higher growth in resource-intensive industries. Also, household real income will continue to increase due to lower energy prices with possible knock-on effects on spending.

We expect that in 2016, lower commodity prices will help resource-intensive industries, such as petrochemicals, paper and aluminum. Overall, businesses will see their input costs reduced primarily through lower commodity prices and transportation costs.

Increased Impact of Climate Change

Climate change and the struggle to limit CO2 emissions is a slow-motion crisis but one that is increasingly making itself felt. Climate change has implications for food prices, which in turn puts pressure on the social fabric of countries. The frequency and severity of extreme weather events are also increasing around the world and impacting economic growth. China and India remain the two countries at the greatest risk of climate-change impact.

Climate change is also causing the Arctic polar ice caps to melt. The resultant rising sea levels have serious repercussions on coastal communities and economies. Those looking for silver linings may point to easier access to the natural resources in the region or more accessible or even new shipping lanes. But these “benefits” are far outweighed by the risks of global warming.

Greater volatility in weather patterns may also disrupt supply chains and consumption patterns. Expect rising insurance costs and increased regulation.

Governments across the world will ratchet up stricter regulations to achieve their environment control targets. In 2016, we project a lot of focus on sustainability initiatives across businesses. Enterprises will incorporate green and sustainability initiatives as part of their business strategy. Consumers and markets will reward businesses that take tangible steps in this direction. In addition, businesses will invest in increasing energy efficiency and consumption reduction.

Push to Digital

In 2015, we saw the continuing development and application of technology to drive productivity and change the way work is done. Gartner projects that the Internet-of-Things (IOT) devices will continue to grow rapidly from less than 4 billion devices in 2014 to a projected 25 billion by 2020. These devices are being used in newer areas, including manufacturing, supply chain automation and consumer electronics.

In 2016, the big trend will be the increased ‘push to digital’. As more devices get Internet-enabled, the digitization of products will have huge impact on traditional industries, such as automotive, industrial manufacturing and even home construction. Internet-enabled kitchens, home appliances and cars will be more common.

These technological advancements are being manifested in information technology products and services too. Business software is not only reducing requirements for manual human intervention, but armed with artificial intelligence and predictive capabilities, it is enabling greater, more accurate forecasting, planning and resource allocation.

At the same time, our increasing dependence on technology increases our vulnerability to cyberthreats, including crime, espionage and terrorism. Data security breaches are increasing — 2015 saw some large breaches at Blue Cross Blue Shield, Kaspersky Lab, and the U.S. Federal Government (Office of Personnel Management).

The growing interconnectivity among software, devices and systems will increase our vulnerability to cyberattacks. The 2015 Fortune 500 CEO Survey revealed that cybersecurity was considered as the second biggest challenge for enterprises. Awareness of this is growing among business leaders and will increasingly factor into business planning.

In 2016, we predict continued expansion of Internet-enabled devices across the value chain in businesses. We also predict increased use of decision-support tools in procurement, marketing and finance where decisions will be supported by ‘AI-enhanced software’. This is already being seen in the widespread use of ‘procurement software’ that encompasses the entire source-to-pay (S2P) cycle. S2P tools will now be strengthened by machine-learning algorithms to detect patterns and support faster and enhanced decision-making. These changes will be accompanied by increased awareness and requirements for data security.

IMPLICATIONS FOR PROCUREMENT LEADERSHIP

Focus on Supply Chain Risks and Business Continuity

In 2016, geopolitical turmoil will result in greater focus on managing and mitigating supply chain risk. GEP believes that procurement leaders will be expected to develop strategies that ensure redundancies in the supply side, analyze and assess risks across each segment of the supply chain, and develop fail-safe mechanisms to ensure continuity. For example, a change in the geopolitical situation in a region will affect not only the supplier location, but also the logistics network used for transporting the material from the supplier location to the business plants.

Procurement will need to work with internal partners (manufacturing, sales) and external partners (suppliers, logistics, regulatory authorities) to address these issues. Category strategies will need to incorporate supply chain risk management plans.

Build Relationships in the ‘New’ Emerging Economies and Revitalize Relationships in the U.S.

As new emerging markets take center stage, businesses will expand their presence in these regions. Procurement will be expected to support this growth by establishing supply bases in new markets and implementing supply chains to support businesses in these areas. Similarly, with the U.S. economy growing in strength, along with the softening of the Chinese economy, procurement organizations will need to review their established supply chains in these regions.

Procurement and supply chain leaders will need to evaluate opportunities for restructuring their relationships in the U.S. and China to take advantage of the economic conditions. This will translate into potentially reshoring some of the supplies to the U.S. from China as well as strategic restructuring of established supply bases in China.

Take Advantage of the ‘Resource Slump’ in Commodity Prices

The commodity price slump will introduce new opportunities for the procurement function. In 2016, procurement functions of organizations with substantial commodity spend will need to look at developing and maintaining a reliable supply base. In addition, procurement leaders should use this opportunity to restructure relationships with their supply base, taking advantage of the lower resource prices and reducing the overall cost of inputs.

Factor Sustainability Initiatives into Supply Programs

GEP anticipates sustainability goals to be a key focus area for organizations in 2016. Use of renewable energy solutions, increased recycling or reusability drives, carbon-neutral programs and demand-management campaigns — an increasing number of enterprise procurement leaders will look to implement some or all these types of initiatives, in partnership with their strategic suppliers. Negotiations with suppliers and long-term category strategies will need to incorporate these sustainability projects. These will become important components in the ‘total cost of ownership’ analysis used by the procurement function to determine the optimal supply structure.

Embrace Technology to Drive Disruptive Innovation – Both in Procurement and Beyond

Procurement organizations will not be immune to the adoption of technological advancements — in devices as well as in software systems. In 2016, procurement leaders will need to actively explore how they can use disruptive technologies to improve the business user experience and simplify the overall process — reducing their overall costs. Procurement teams will need to support the IT function to ensure data security with all supply-side partners. Procurement leaders can also leverage the developments in procurement technology to drive efficiencies and help them make better decisions. Use of cloud-based integrated S2P software that provides an end-to-end view of the procurement landscape as well as ‘predictive spend analytics’ will help procurement leaders to increase their reach and impact on business strategy.

SUMMARY

Projections and Strategy Recommendations for the Procurement Function in 2016

| Trend | Prediction | Procurement Strategy |

|---|---|---|

| Heightened impact of geopolitics |

Governments worldwide will adopt a more nationalistic posture that has the potential to spill over into the business sector Increased risk of protectionist policies in key industries and sectors around the world Geopolitical instability will translate into greater supply chain risks with implications on everything from labor markets to shipping |

Increase focus on supply chain risk management and business continuity planning |

| Shift of economic power to the U.S. and new emerging economies |

U.S. economic growth will provide opportunities to many businesses. High domestic demand and lower energy costs will boost the U.S. manufacturing industry Emerging markets will continue to offer a variety of business opportunities. Many markets — including BRICS — will offer opportunities to sell to a growing middle-class consumer group, bringing challenges in the form of increased diversity |

Explore new opportunities for establishing supply bases in the ‘new’ emerging markets Restructure relationships with existing supply bases in the U.S. and China to take advantage of changing economic conditions |

| Continued decline in global commodity prices |

Lower commodity prices will help industries, such as petrochemicals, paper and aluminum Businesses will see their input costs reduced primarily through lower commodity prices and reduced transportation costs |

Restructure relationships with supply base — take advantage of the lower resource prices to reduce the overall cost of input |

| Increased impact and awareness of climate change |

Increased focus on sustainability initiatives across businesses Enterprises will incorporate green and sustainability initiatives as part of their business strategy Volatility in weather conditions may disrupt supply chains and consumption patterns |

Design and implement sustainability programs into procurement initiatives — for example, as part of supplier relationship management programs Include climate and sustainability related costs into negotiations and contract structures Assess climate-related supply risks and develop plans/strategies to mitigate them |

| Push to Digital |

Continued expansion of Internet-enabled devices across the value chain in businesses Growing interconnectivity among software, devices and systems will increase vulnerability to cyberattacks Increased use of decision-support tools in procurement, marketing and finance where decisions will be supported by ‘AI-enhanced software’ |

Leverage technology advancements — in partnership with suppliers — to increase ease of use, reduce costs and improve overall business user experience Review data security (with support from IT function) with all external partners Shift to cloud-based, integrated S2P solutions to drive greater performance and value beyond savings |

CATEGORY TRENDS

Business Services – Travel

The demand for global business travel remained buoyant in 2015 due to an optimistic economic environment. The past year also witnessed record high investments (~$5.4 Billion) in travel-related apps with leading online booking platforms, such as Concur, Serko and Amadeus making major headway. Yapta’s fare analyzer tools — FareIQ and RoomIQ are gaining traction with cost-conscious customers.

The concept of shared economy and ‘bleisure’ (combining business travel with leisure travel) is expected to take center stage in the coming years, with millennial corporate travelers riding the wave. The rise in shared economy will be expedited by apps, such as Airbnb, HomeAway and HotelTonight, which would increasingly find a place in enterprise travel policies.

Ride-sharing apps, such as Uber and Lyft, have also started to have a disruptive impact on the travel industry, with Uber offering a standalone service for its corporate clientele called ‘Uber for Business’. Airbnb has also launched a suite of services for corporate users called Airbnb Business Travel. Numerous apps, such as Lyft and HotelTonight, have partnered with online travel booking tools, such as Concur, to rope in more corporate travelers to their customer portfolio.

Gamification as a tool to revitalize policy compliance and bring cost savings will gain popularity in the coming years. Travel Management Companies (TMCs) and enterprises will continue encouraging corporate travelers to use travel-related apps to drive cost savings and compliance.

Safety and security of travelers will be a key focus area for travel portfolio managers, post the Paris attacks. Travel managers must look for Travel Risk Management (TRM) programs that bring crisis support, proactive trip details, travel alerts and comprehensive travel policy norms, to the table.

Business Services – Human Resources

By 2020, millennials would account for nearly half of the global workforce. Millennials are tipped to trigger the growth in temp-related jobs over the next five years. Several other factors, including economic downturn, requirements for specialized skill sets, demands for a flexible workforce, and the chances of getting permanent positions are likely to boost the temp labor market in the coming years.

In the U.S. alone, driven primarily by healthcare reforms, the temp staffing industry added nearly 1.24 million new jobs (12.3 percent of all jobs created in the private sector) since the recession. The ACA (Obamacare) finally materialized last year and had a notable impact on staffing firms, pushing them to increase their markup rates and pass on the additional costs to customers. The situation is expected to be more intense in 2016 with an increase in regulatory pressures. The advent of flexible workforce is likely to drive the need for integrated human capital management systems, popularly termed as total talent management, among HR sourcing managers.

Skills shortage will be a challenge in 2016, with one in four hiring managers planning for openings related to STEM (Science, Technology, Engineering & Math) in the coming year. Talent shortage surveys indicate that recruiters are facing difficulty sourcing specific talent groups, including engineering and skilled trades.

Demographic shifts will emerge as a key concern for many enterprises, with many countries encountering a stagnant or shrinking labor force.

Online staffing and crowdsourcing will witness strong growth, driven by the increasing role of technology in employee engagement. Talent sourcing managers must explore online labor exchanges, such as Elance and Freelancer to tap into highly skilled lower-cost resources, virtually on-demand.

There is also an emerging concept of “enterprise-workforce-as-a-service,” or eWaaS, which simply involves “dialing up” talent when needed. Using innovative hiring platforms, such as Elevate Direct and People Per Hour, recruiters can search for and interact directly with prospective hires.

Energy & Utilities

Global primary energy consumption decelerated sharply in the past two years and will continue to decline in 2016. Natural gas, coal and crude oil continue to be the primary energy sources in the U.S. with support from nuclear and renewable sources. Oil will remain the primary fuel for transportation and industrial sectors.

Oil prices declined throughout 2015 driven by continued excess supply from OPEC, combined with lower-than-expected decline in the U.S. shale oil output and a slowdown in the global economy. With an almost stagnant domestic demand, the U.S. plans to export oil enabled by lifting the 40-year oil embargo. Lifting of economic sanctions on Iran have further added to the oil surplus. With excess inventory and slower growth expected in emerging and developed markets, oil prices will continue to decline in 2016.

In 2015, natural gas supplanted coal as the leading fuel source for U.S. power plants for the first time ever. Gas prices reached 16-year lows, providing a cost advantage for utilities and other energy buyers. With current gas inventory levels well above the five-year average and uncertainty over climate change forecasts, downward pressure on natural gas prices will continue in 2016. The above trends in the energy commodities market highlight the need for a robust procurement strategy, adaptable and flexible to current market conditions. Attaining cost savings amid lower commodity prices and changing interest environment in the U.S. will be key strategy for U.S. energy and utility companies.

With lower commodity prices expected to persist in 2016 and increased volatility in global markets, category managers should opt for short-term contracts to procure energy commodities like oil, natural gas, coal and electricity. Energy-intensive businesses, such as transportation, cement, chemical and manufacturing industry can leverage low energy commodity prices by reprising their existing energy/fuel contracts commensurate with current market prices.

Implementation of technology-based platforms, such as the “Internet of Things” (IoT), will drive savings for category managers. Increased adoption of technology will result in further streamlined procurement processes and grid modernization, thus delivering improved efficiencies and savings.

Facilities Management

The highly competitive facilities management market, together with increased focus on security and sustainability has been pushing service providers toward innovation. Introduction of integrated/total facility management, along with the demand for services, such as energy management and real estate management, is driving this market toward consolidation.

The market is gradually shifting from single service to bundled services, and further toward total facility management. Increasing number of companies have consolidated their global facilities management spend with a single supplier, thus enabling the convenience of a single point of contact, savings based on volume consolidation, etc. The facilities management market is dominated by large global players, accounting for nearly half of the market. These players are rapidly increasing their footprints into regions, such as APAC and LATAM.

With the focus shifting toward consolidation, acceptance of subcontracting or vendor-managed contracts is also increasing. This gives buyers as well as service providers increased flexibility and more options to choose. Subcontracting or vendor-managed sub-contracting also allows service providers to offer more services, while ensuring increased geographical coverage.

There’s also a shift in the choice of the outsourcing contract model. While fixed-price contract and guaranteed maximum price continue to be the most widely accepted contracting models, performance-based contracts with gain sharing or outcome-based fee are also gaining traction.

In line with the current market trends, enterprises must look at consolidating their spend to a few vendors and explore new outsourcing contract models.

Information Technology

As the initial concerns about the practicality, reliability and security of the cloud have almost entirely evaporated, more and more companies are now expected to move to the cloud. New research from International Data Corporation (IDC) suggests that the worldwide spending on private cloud services will grow at a compound annual growth rate (CAGR) of 13.8 percent and public cloud services will grow at a 19.4 percent (CAGR), nearly times six times the rate of overall IT spending growth — from nearly $70 billion in 2015 to more than $141 billion in 2019. Spending on IT infrastructure for cloud environments will grow at a compound annual growth rate (CAGR) of 15.5 percent and will reach $54.3 billion by 2019, accounting for 46.6 percent of the total spending on enterprise IT infrastructure.

Implementing out-of-the-box (OOTB) functionalities will gain prevalence to reduce costs, increase application connectivity and boost the ability to utilize optional Software-as-a-Service (SaaS) implementations of applications. Software-as-a-Service (SaaS) will remain the dominant cloud computing type, capturing more than two-thirds of all public cloud spending until 2019.

IT buyers will limit utilization of “Tier 1” IT Professional Services (ITPS) providers to strategy and design work in an attempt to reduce costs. The cost-friendly lower-tier providers capable of delivering reliable enablement services will do the bulk of the heavy lifting and hence gain from this shift. In some cases, Tier 1 consultants will just play supervisory roles to ensure the design integrity throughout the course of the project, helping buyers lower their overall costs by up to 25 percent.

Growth in the IT Enterprise Software (ESW) segment will be dominated by the individual requirements of various companies utilizing ESW applications. To support the growing need of interoperability of data between systems, many firms are undertaking evaluations of their existing ESW portfolio. Many firms who have been putting off their decisions to replace aging ESW applications are being forced to evaluate and migrate to newer technologies to reduce overall maintenance and support costs, and to take advantage of the capabilities available in new ESW applications.

IT Infrastructure and Automation

With an increasing demand for flexibility and agility, and the reducing capital dollars for IT assets, many enterprises will seek Infrastructure as a Service (IaaS) and the supply base for IaaS will continue to mature. When evaluated across critical capabilities, Amazon Web Services currently dominates the IaaS market.

In 2016, network security will continue to challenge consumers, enterprises and even governments as hackers attempt to penetrate even the most sophisticated firewalls. Enterprises will have to continue investing in stronger, multi-layered security measures to protect sensitive information and customer data or strategic corporate data.

Big data analytics is maturing at a rapid pace as enterprises demand insightful, real-time analysis to capture new trends as they evolve or to develop capabilities of reacting to emergencies that require activation of alternative strategies. However, big data analytics require larger servers and powerful mainframes, capable of retaining huge amounts of data in memory to facilitate faster processing. Hence, growth in big data analytics can contribute to the growth of IaaS.

In 2016, computer automation and robotics segment will target to deliver on the promise of greater operating efficiencies for IT integrated systems suppliers. Major providers will seek capabilities to resolve incidents without human intervention, replace code that is susceptible to problems and develop new applications with more automated functionality – each with the ultimate aim of mitigating higher IT labor costs. Procurement organizations need to assess which suppliers are making the heaviest investments and which are offering to pass these savings back over the life of the agreement.

Firms operating with aging ESW applications must look to migrate to newer, cloud-based applications that are scalable and flexible, and reduce the overall maintenance and support costs.

Telecom

The outlook for 2016 looks favorable for telecom enterprises, with a drop in prices driven by technological improvements at the supply side and higher operating efficiencies. But traditional competitors will be challenged by new players, such as Amazon, Google, and cable companies. In 2016, 4G wireless, unified communications and cloud services will continue to mature and offer capabilities that will stimulate the demand for voice, data and video services.

IDC’s latest report on public cloud services expenditure states that the telecommunications industry will see the fastest growth in cloud investments till 2019, with a worldwide CAGR of 22.2 percent.

With the wireless market continuing to grow, it is beginning to take on an increasingly global posture. AT&T commenced wireless operations in Mexico and finalized the DIRECTV deal that significantly diversifies the company’s revenue mix, products, geographies and customer bases. Verizon continues to focus its growth on U.S. Wireless, entertainment and now, internet advertising. Its acquisition of AOL moves Verizon into the number three spot for internet advertising, just behind Google and Facebook.

The company also appears to be positioning itself to exit the network business. Competitors, such as Orange, BT and Vodafone could potentially acquire the business from Verizon to enhance their global footprint, especially in the U.S. where Sprint and T-Mobile will continue to fight it out for the number three spot.

The European market for wireless services is set to change in 2016 and 2017 as regulators have set a June 2017 deadline to eliminate roaming charges across Europe. Vodafone and the consortia, FreeMove, led by Orange, are aggressively pursuing the pan-European business to secure market share early in the consolidation process.

Continued double-digit rate increases for “local” services across all geographies are expected in the coming years. Aggregators, such as Granite and MetTel have developed mature businesses that not only offset rate increases but can actually reduce costs by 25 to 35 percent. Telecom equipment sales will remain flat or decline as more services will be offered through software.

The number of cloud and communication service providers deploying Software-Defined Networking (SDN) for the first time — or expanding its use — in the data center will increase from 20 percent this year to 60 percent in 2016, according to a recent survey by research firm IHS. The increase in deployment of SDN will further enable and drive the shift to cloud, with the enterprise adoption rate expected to grow from six percent to 23 percent. Enterprises must leverage the opportunities presented by these new technological developments and develop a clear, holistic strategy to shift to the cloud. Procurement must look at consolidating communications suppliers to optimize spend wherever possible.

Wireless commitments should be restricted to two years with a possible year three as an option. International carriers should be included in any global network RFPs. Enterprises must focus on consolidating the local services, utilizing aggregators in combination with one significant local exchange carrier (LEC). Procurement professionals should evaluate softwaredefined services before future telecom hardware purchases and consider third-party hardware maintenance partners to extend network equipment life.

Logistics

The transportation and logistics market for 2016 is expected to be predominantly driven by three distinct factors: lower fuel costs, global economic challenges, and mergers & acquisitions (M&A). These factors will impact the logistics operations of every organization, regardless of its logistics spend.

Ocean Freight

The slower global economic growth rate of 2015 has impacted ocean freight. With the Baltic Dry Index hovering around historic lows since mid-November, indicating slower demand for commodities, the weak growth trend in ocean freight is expected to continue in 2016.

Ocean liner companies are looking at various options to cut costs and stay afloat – though they have limited room to reduce the operational expenditure other than fleet idling and workforce reductions. Leading liner company, Maersk has announced a reduction of nearly 16 percent of its workforce during 2016. The excess capacity and lower price of crude oil is expected to persist till the end of 2016, causing the container shipping industry to prepare itself for a year of lower freight volume, utilization and idling of fleet.

In terms of lanes, as compared with trans-Atlantic lanes and lanes in and out of Africa and Pacific, the Europe-Asia lane is expected to witness very weak growth. The demand arising out of China will be impeded by China’s slow growth. Beyond just considering the rates, supply chain planners would also need to factor in longer transit times and timely delivery of cargo shipments. Large buyers would focus on engaging with the right service partner to balance their supply chain needs.

Among alliances, 2M would continue its dominance in the Europe-Asia lane. CKYHE would be a leading player in the trans-Pacific lane. The recent CMA CGM’s acquisition of Neptune Oriented Lines (APL) is expected to increase the competition at the top, reducing the gap between CMA CGM and the market leader Maersk to about two percent in terms of market share.

Overall, with lower rates and weak growth in demand, the outlook for liners in 2016 is grim. However, the rates are expected to pick up in the latter half of 2016.

With factors like slow growth projections for China, upcoming elections in the U.S., and significant downturns in countries, such as Russia, Venezuela and Brazil, the global economy is predicted to grow at 3.3 percent in 2016 — a marginal growth above the estimated 2.9 percent witnessed in 2015. The lower growth will impact global ocean freight — both containerized and bulk — as 90 percent of the global trade is dependent on ocean shipping.

Newly merged logistics companies eye fresh customers to feed the combined firm. Hence, the significant M&A activity being witnessed across all modes (and geographies) can help buyers to reduce costs and drive more value.

Crude rates are expected to be below the $45 per barrel mark throughout 2016. The impacts of lower fuel cost are significant – beyond the lower gas/diesel costs enjoyed by consumers, it has also increased the capacity of U.S. rail providers. It has also resulted in a fundamental change to the underlying cost components of road/air providers.

Given the lower fuel costs, truckload shippers would look to leverage the cost reduction opportunity by revising fuel surcharges and renegotiating rates. The outlook for rail is mixed, with a weaker coal demand and lower oil production dealing a heavy blow to the industry.

Ocean freight rates will continue to decline and buyers should renegotiate lower ocean freight contracts to gain from falling prices. The air freight market is expected to remain subdued. Hi-tech and life sciences companies must consider shifting some of their movements to air to reduce lead times and achieve efficiency in their supply chains. Parcel volumes, rates and surcharges will witness a rise in 2016 due to the increasing ecommerce success. However, the introduction of “Amazon Air” and expanded acceptance of drone delivery could cause some disruption in the market. In 2016, it will be critical for organizations to optimize their transportation and logistics to counter the slow trade growth. Establishing a streamlined network strategy and adopting technology solutions to optimize processes will be the focus.

U.S. Warehousing Market Outlook

The demand for warehouse space in 2015 outgrew the supply and remained strongly driven by consumer demand, increase in jobs and modest growth in wages. The demand for large warehouse spaces witnessed a considerable increase in the past year.

There is an increase of speculative construction in the major warehouse markets and a marginal drop in the secondary markets. Despite the increased speculative construction, the demand growth is expected to outpace the supply in 2016. The vacancy in 2016 is expected to drop to 6.4 percent.

The ownership of industrial and distribution properties in the U.S. has gradually been concentrated with fewer owners/institutions as a result of investor interest in commercial real estate segments. For the buyers, it means increase in the power of suppliers with larger assets and higher negotiating power.

With 14 states and major cities increasing the minimum wages from January 2016, labor costs are expected to register a considerable increase in the warehouse sector. This will prompt 3PL firms and end-users to evaluate additional investments in warehouse automation and material handling systems. The Panama Canal is expected to open in April 2016 and would increase demand for warehouses near the eastern ports. Rentals in these regions could outgrow average market rates.

In 2016, this market is expected to be driven by the opening of Panama Canal, demand for ultra-large warehouses and sustained demand growth in the U.S.

CAPEX & Construction

The global capital project and infrastructure market is expected to be over $9 trillion per year by 2025, nearly double from $4.7 trillion in 2015. Capital project expenditures are expected to increase in countries like China, Philippines, Indonesia, Ghana and Nigeria. Issues affecting capital programs remain consistent across all industries and geographic zones with risk management topping the list. Large capital projects are usually outsourced to Engineering, Procurement & Construction (EPC) firms who have a transactional approach to procurement, resulting in various risks, such as cost overruns, schedule delays and quality issues.

Labor shortage is another key challenge for capital projects across the world. Many suppliers use labor brokers to provide the capacity but such labor force is more likely to have issues with productivity and safety. An improperly designed project will significantly impact the schedule and cause cost overruns. Understanding your project’s labor requirements with regard to both professional and craft labor can reduce delays and, more importantly, enhance safety. Enterprises must seek complete transparency into billing rates, man-hours and qualifications of the workforce on the project.

Steel vs. Polymers

Historically, the cost of steel and polymer resin (if applicable) have been “minor” negotiation points during large capital equipment purchases. In the last couple of years, steel has mostly stayed flat. But polymer resin, a by-product of crude refining, is going down with crude prices.

With the record low oil prices now looking like a sustainable medium-term trend, original equipment manufacturers (OEMs) must seriously consider investing R&D dollars to use more polymers in their products.

This trend is likely to be limited in its impact – heavy industries cannot utilize polymers, food processing or pharma product contact equipment cannot use anything other than food-grade stainless steel, etc. However, a significant portion of capital equipment and parts are up for evaluation.

Robotics and automation will mitigate some of the labor shortage problems for many manufacturing industries. The growth rate of the robotics and automation industry is expected to reach 10 percent by 2020. Also, the cost per hour of flexible, generic production line robots is expected to fall from $28/hour to $20/hour. Robotics has moved beyond the early adopters, such as automotive and technology, and is increasingly being used in the CPG, pharma and other industries. New 3D visual inspection systems have solved issues that traditionally prevented robot use in areas, such as trimming/cutting, defect removal, warehouse pick and pack, palletization of variable sized cases, etc.

Volatile material prices and delays in delivery are common risks associated with capital projects. Many companies do not leverage material spend across their capital projects. Manufacturing sites/plants and business units routinely purchase material for their capital projects individually, without considering the spend in other projects.

Bundling material spend across the capital projects is an emerging trend in the industry. As materials are marked up through the value chain of secondary and tertiary suppliers, leveraging volume is an effective way to reduce costs on purchases. Developing a capital project program that shares knowledge across projects, with visibility into the schedule, will enable a coordinated approach for material purchases. During the project lifecycle, materials are required to be on site at different times throughout the construction process. Aligning the purchase of materials with market conditions can help drive further drive savings in a capital project program.

MRO

Amid economic slowdown, falling oil prices, and increased demand for outsourced MRO, the real challenge for category managers is to identify direct and indirect saving opportunities. The rising awareness of the benefits of outsourcing will continue to drive demand for outsourced MRO, with key challenges being the inherent complexity of the category and a highly fragmented spend. These challenges have led enterprises to adopt various levels of outsourcing, based on their category maturity, capability and criticality.

Current market slowdown, economic turmoil and record low oil prices have led to a number of oil and gas projects getting delayed or shelved, thereby weakening MRO demand. With weak MRO demand, and lower metal and lubricants prices, category buyers can cash-in on the resultant direct unit cost reduction on parts and spares. The current slowdown and weaker metals and crude oil prices are expected to continue through most of 2016, with some recovery in prices expected later in the year.

The MRO market has its own regional dynamics. For example, North America is one of the most mature markets in terms of supplier capabilities. Suppliers’ coverage and service offerings are further evolving toward innovation and value-added offerings. On the other hand, APAC and LATAM are still in their early stages of adoption of MRO outsourcing. Suppliers are still focused toward basic service offerings, MRO supplies consolidation and building capabilities in terms of increased product, services and geographical coverage.

While outsourcing MRO, enterprises must to take into account these regional dynamics and the category strategy must be flexible enough to accommodate these regional challenges. Buyers can leverage these market conditions to achieve some short- to mid-term savings. With a clear understanding of their MRO spend and adoption of an outsourcing model customized for specific requirements, MRO sourcing managers can drive direct cost savings of 10 to 20 percent, enable process improvements, improve efficiency, and ensure strategic alignment with business goals.

Packaging

The overall demand for packaging in 2016 is expected to be moderate, mainly due to the volatile global economic environment. Emerging markets will be the largest contributors to growth. Raw material prices are expected to continue on a downward trend, leading to lower packaging prices in the first two quarters of 2016. However, in the second half of 2016, prices are expected to stabilize, resulting in an upward growth trajectory, supported by the marginal recovery of crude oil prices.

Packaging companies will focus on innovation in terms of new environment friendly materials, shapes and printing, apart from delivering short-run lengths economically. Additionally, the focus will be on strategic acquisitions to increase global presence, especially in emerging countries, and to expand product portfolio, realize synergies in operations and increase financial prowess.

With growing environmental concerns and regulations, packaging buyers need to focus on supply chain transparency to avoid potentially costly environmental and legal violations. Systemic changes are required to shift the global plastic value chain and this will require major collaboration between all stakeholders across the value chain – right from consumer goods companies, plastic packaging producers and manufacturers, businesses involved in collection, sorting and reprocessing, policy-makers and even NGOs. Procurement leaders will have to lead and drive this change.

In 2016, companies with a global footprint will seek to consolidate their packaging spend and achieve greater process efficiency. Procurement professionals will need to align with these changes to control costs and boost growth by developing a comprehensive understanding of key cost drivers and monitoring raw material prices.

Marketing – Advertising & Digital Agencies

Global advertising spend reached $540 billion in 2015, with an increase in marketing budgets across sectors. Advertising spend grew at a CAGR of five percent, with the trend likely to continue in 2016. One of the key highlights of 2015 was the increasing shift in spend from print to digital. According to the Standard Media Index, 2015 saw a 26 percent increase in digital advertising globally. Television still contributed about 42 percent of the global ad spend but grew at a sluggish rate of 3.6 percent.

Spend on digital media is likely to make up to 24 percent of the advertising budgets in 2016. Shortage in creative talent is expected to drive up the prices for creatives by three percent. With increasing costs, we expect more digital work to be outsourced to Latin America (LATAM) and Asia Pacific (APAC). Major advertisers with high spend have established their creative hubs in LATAM (Brazil) and APAC (India).

With an increasing spend on digital channels and programmatic media buying, companies are also investing on ROI tracking tools. Adoption levels of performance-based models are expected to increase in 2016, with 80 percent of the agency fee on retainer and 20 percent calculated on the KPIs set in the contract. While the average contract duration for creative agencies has always been long (four to five years), marketers continue to face difficulties in building a digital agency roster as the supply landscape remains highly dynamic.

With several media consolidations happening in 2015, we expect similar account switches and consolidations for creative and digital in 2016. Major holding companies, such as WPP, continue to acquire agencies that are strong in digital tracking and analytics as there is an increased push from the marketers to move toward digital and a performance-based approach.

Overall, 2016 looks very positive for marketers, with a lot of push for account consolidations, agency transparency and performance-based approach, and a notable shift in spend from print to digital advertising platforms.

Theme: Digital Transformation

RECOMMENDED

Featured

The Cost-Plus World of Supply Chains: The Macroeconomic and Geopolitical Environment

As geopolitical and macroeconomic concerns increase, this survey-based Economist Impact-GEP report looks at what companies are doing to manage the resultant supply chain challenges.

Case Study

How a Global CPG Company Saved 20% on Packaging Costs by Partnering With GEP

GEP helps leading U.S.-based CPG company optimize its packaging spend, improve inventory management and its forecasting capabilities.