The Big Picture

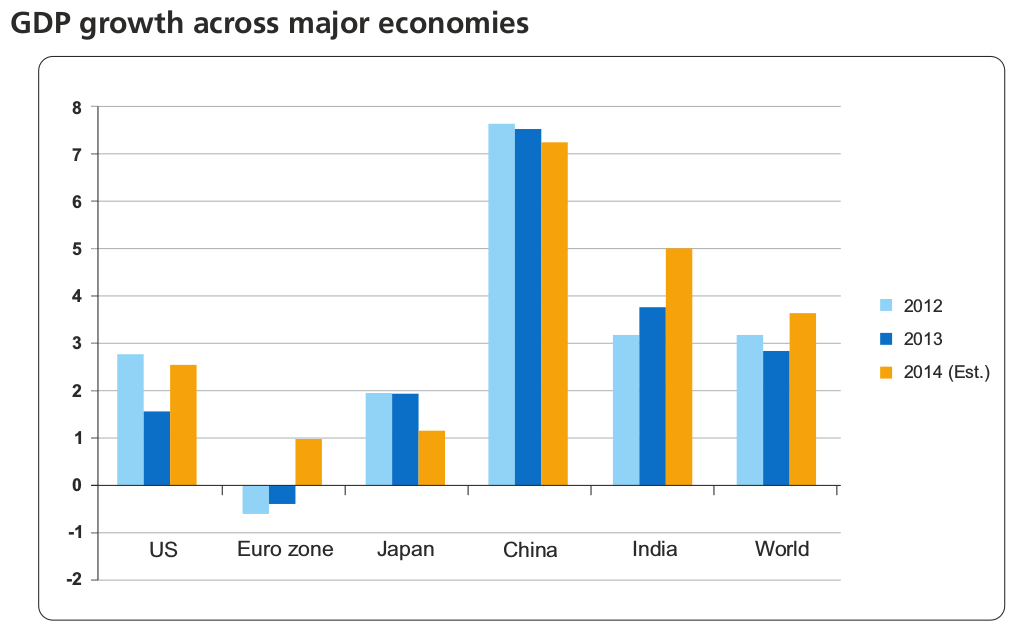

Global macroeconomic risk began to shift in 2013 from the more mature economies of the United States, Western Europe and the Pacific Rim (OECD nations) to emerging markets, including most vital BRICS countries (Brazil, India, Russia, China, South Africa).

The major advanced economies are stabilizing, even growing, while powerhouse BRICs nations are seeing their typically stellar growth rates continue to slow. In many cases, this lackluster growth is stemming from structural bottlenecks in infrastructure, labor markets and investment. Still, it should be noted that improving conditions in developed economies often can — and do — deliver knock-on benefits to emerging markets.

In the United States, consumer confidence continues to strengthen, while the political climate seems to be improving with a recent budget deal. However, the Federal Reserve Bank is widely expected to taper off its “Quantitative Easing” program in 2014 — the impact of this on the global financial markets is unknown. At the same time, the euro zone region is expected to finally see some modest growth in 2014, as will Japan, which will continue its economic reforms under “Abenomics”.

Overall, the global economy is expected to grow by 3.6 percent in 2014 and global trade is expected to grow by more than 5 percent — the strongest expansion since 2011.

Prediction is very difficult, especially if it’s about the future

- Niels Bohr

We see 2014 as a potentially pivotal year in the overall global economy, where a number of key business and technological factors will more profoundly influence global economic activity. Among them:

- Slow, steady improvement in business conditions will increase global trading activity, putting pressure on the delivery capabilities of supply chains and supply partners.

- Innovations in small-scale manufacturing, better connectivity, volatility in developing countries, and shifting labor markets will disrupt complex, global supply chains.

- Rapid technological advances in the collection, storage, processing and analysis of massive data sets will make Big Data solutions mainstream.

- Continued rise of social technologies and mobile platforms will accelerate change in long-established work flows, work patterns and work styles.

And for enterprise sourcing, procurement and supply chain professionals, Procurement Trends in 2014

Trend 1: From Cost Focus to Value Focus

The past few years have seen enterprise procurement teams playing a critical role in achieving cost savings targets for market-leading organizations worldwide. As global trade expands and business conditions improve, procurement organizations — while continuing to focus on the bottom line — will increasingly see themselves evaluated as “value centers”, accountable to the shareholders to deliver specific and measurable ROI targets.

Leading procurement organizations will meet this challenge by changing the way they operate. Suppliers will no longer be seen as “the opposing party”, who need to be cajoled or threatened to deliver cost savings. The procurement function will increasingly actively collaborate with strategic suppliers to drive innovation, new product development and improve overall supply service levels. Hard-ball tactics will increasingly be displaced by fact-based negotiations; short-term discounts will be replaced by long-term partnerships and “value addition”.

Similarly, focus will shift from “identified improvement” to “profit and loss statement impact”. In other words, implementation and realization of benefits will be key.

From a delivery perspective, top procurement organizations will identify areas within their function that can be outsourced to an external partner. Procurement transactions are already being outsourced by high-performance procurement operations, but 2014 will increasingly see the next level of outsourcing. Companies will identify non-core categories whose category management activities can be outsourced to an expert third party, enabling the internal procurement resources to focus their time and energy on more strategic activities and category management closer to core.

Trend 2: From Complications to Managed Complexity

As trade picks up in 2014, the globalization of supply chains is expected to continue with renewed vigor. And as supply chains become more complex, so will the demands on the procurement team.

Indeed, enterprise procurement teams will be called to manage complexity in many forms and flavors. For instance, products and product requirements are becoming more complex, so companies need to create diverse sets of options, packaging designs and logistical arrangements. Customers increasingly want customized solutions and have specific logistics delivery requirements. This means that companies need to have more facilities in more countries, with more suppliers, greater diversity in product and packaging, more e-commerce and other market channels, and more part numbers.

On the sales side, increases in local delivery requirements are driving complexity in distribution logistics. Layer on top of this increasing urbanization, economic volatility in the growth markets, political disturbances (India, China, and the Middle East) and you have a powerful and varied set of potential headaches.

Procurement leaders will move to identify ways to reduce the supply chain complexity and manage their costs accordingly. They will partner and collaborate closer with sales, manufacturing, new product development and suppliers to achieve this. Sources of complexity and the corresponding value impact will be measured and tracked to identify corrective action.

Trend 3: From Unknown Unknowns to Strategic Risk Management

Game of Thrones has made famous the foreboding phrase, “Winter is Coming.” This sentiment is likely appropriate for 2014.

Weather-related incidents, natural disasters and man-made catastrophes are on the rise. The epic typhoon in the Philippines, off-schedule flooding in India and “polar vortexes” in the US are all examples of just how costly and disruptive extreme weather can be.

If weather is becoming more volatile, so is the global political environment.

Supply chains passing through the Middle East, Ukraine and Thailand are being impacted by social and political unrest in these regions. In 2014, India is undertaking national elections and is widely expected to replace the incumbent government with a possible coalition party of regional players – this means high uncertainty, especially with respect to the local business and regulatory environment.

Business scandals — involving everything from clinical research to corrupt sales practice — are igniting new waves of government regulation, thereby increasing the pressure on procurement to manage third-party activities with high transparency and ample audit trails.

But with risk comes opportunity. For example, the Single Euro Payments Area (SEPA) is expected to take effect in February 2014, standardizing payment and collection codes across the euro zone, which will make it easier and cheaper to pay suppliers.

In summary, “supply risk management” will be a hot button issue for procurement in 2014. Risk models will need to be upgraded to identify critical areas in the supply base and logistics points. Data feeds need to plug into these models on a real-time basis and procurement will need to develop short and long-term mitigation strategies to address these risks.

Trend 4: From Desk-bound to Cloud-based

The global cloud computing market will grow at a compound annual growth rate (CAGR) of 36 percent till 2016, reaching a market size of $19.5 billion. A lion's share of this will go to Amazon, Google and Microsoft. While Amazon and Google are primarily targeting retail consumers, Microsoft is focused on the enterprise market and is adding nearly a thousand customers a day with revenue exceeding $1 billion.

Microsoft's cloud platform offers several advantages to developers. Many leading software companies are building procurement-specific apps on Microsoft's Windows Azure cloud platform. The adoption of these apps was limited in 2013 due to security concerns. Microsoft has taken cloud security to the next level — Office 360, a highly successful cloud-based product is a good example of this. 2014 will be the year when fears of cloud security will disappear and adoption of cloud apps will become mainstream.

Trend 5: From Data Analysis to Data Insight

We saw both “big data” analytics and social media gain a lot of ground in 2013. In 2014, they will no longer be just buzzwords.

An increasing number of global enterprises are deploying strategies, tools and tactics that exploit massive data sets and powerful new computing tools. With each success, big data gains enthusiastic acolytes. If they are not in your organization yet, they will be.

While customer relationship management and marketing have driven the early adoption of big data tools and technologies, procurement will begin to slowly but surely catch up in 2014. Among other things, we expect procurement professionals to track supply risks, commodity price and capacity trends, swings in demand affecting supply patterns, and discover new supply partnerships.

Social media will help the enterprise procurement organization to engage beyond its own four walls – with suppliers, peers, market – to generate insights through benchmarking, collaborative sourcing and innovative problem solving. The technology will also be used to provide visibility at the most granular level – what is being purchased from whom, why and at what cost as well as comparing this with others within the organization and outside it.

Trend 6: From Enabler Technology to Integral Technology

Worldwide shipments of 3D printers are expected to grow by 75 percent in 2014 and 150 percent in 2015. This amazing technology could ignite a potential shift of manufacturing base from low-cost regions back into the United States and Europe, with potential radical impacts on supply chains and supplier relationships.

At the same time, the number of internet-connected devices has reached 12 billion – more than the number of humans on the planet. Payments by mobile phones are racing towards the $1 trillion mark. The impact of social technologies on commerce is being experienced every day. Now, many global organizations increasingly relying on distributed problem solving, tapping the brain power of customers and experts from within and outside the company for breakthrough thinking.

Procurement leaders too will embrace social and analytical technologies to generate greater value in 2014. Procurement teams in manufacturing organizations will start to explore the use of 3D printing to quickly deliver on-demand materials, thereby eliminating the need for complex supply chains and supplier relationships.

Similarly, procurement will leverage the powerful analytical tools and techniques now available on mobile platforms – which, for example, provide better transparency into commodity price trends – to make faster, more informed decisions and drive the “fact-based negotiations” referenced earlier.

Implications for Procurement

What impact will these trends have on sourcing, procurement and supply chain executives? We believe that in this era of ubiquitous connectivity and rapid, disruptive changes, procurement leaders must focus on:

- Organizational Transformation: Procurement teams must adapt their processes to leverage new technologies, manage high-risk global supply chains and make actionable intelligence from the information glut they confront daily. This will mean that a larger portion of time will need to be dedicated towards strategic planning, while the tactical activities will need to be automated to a large extent. At the same time, procurement will need to expand its role into a wider range of spend areas, as well as work in a higher degree of collaboration with new product development and sales. “Procurement Transformation” is the key here – enterprise procurement teams will now need to recast their organizations, people and processes to meet these new challenges and to thrive in a new environment.

- Talent Competition: In an environment of permanent rapid change, procurement professionals must continually upgrade or add to their skill set – this is a priority. To better utilize internal resources, procurement leaders should identify which competencies are best sustained in-house and which competencies are best achieved through use of expert external providers. A sober evaluation of where, when and how procurement outsourcing can support both procurement strategy and operations is critical not just to achieve business and financial objectives in the short run but also to develop a sound sourcing and procurement talent strategy over the long haul.

- Collaboration: Complexity, volatility and aggressive targets will need to be managed by procurement professionals through tighter integration with allied business and supply chain functions, as well as external partners, including suppliers and logistics partners. This means that procurement pros will need to play an increasingly important role in ensuring the integrity of the sales and operations planning process, within and outside the organization.

Category Trends in 2014

GEP has hundreds of local, regional and global category experts on staff, helping manage more than $50 billion in spend for leading global enterprises worldwide. We are pleased to share some insights from this accomplished team. We have highlighted some broad themes that stand out across categories to help procurement teams better prioritize their efforts over the next 12 months.

Information Technology

Continued economic recovery in the US and EU is expected to revive the weakened demand for IT consulting/outsourcing services. Depreciating currencies in emerging markets, especially currencies of heavyweight IT/ITES services exporters, such as India, opens up opportunities for deeper discounts from IT services providers in short- and medium-term deals.

Additionally, changes in leadership at giants like Infosys, will focus the battle on market share at the cost of margins, as competition intensifies among the big four IT/ITES providers.

As in 2013, CIOs will continue to challenge their teams to reduce their IT infrastructure costs by focusing on greater adoption of public/private cloud PaaS and IaaS. Amazon Web Services (AWS) remains a clear leader in the public cloud space, but it continues to face strong competitive headwinds from capable challengers with cost- and technology-competitive cloud solutions, and innovative pricing mechanisms. Repetitive price reduction announcements by all players in 2012-13 are expected to continue, thereby creating a somewhat strong buyer's market for businesses to operate in.

Smartphones and tablets are expected to further retard long-term growth in personal computer sales and shipments, pressuring both the top and bottom lines of erstwhile PC behemoths such as HP and Dell. Companies considering an enterprise-level PC refresh can take advantage by seeking deeper discounts through aggressive sourcing exercises, focusing on reducing servicing costs and negotiating directly with OEMs.

Telecom

The North American telecom wireline sector will continue its transition to IP in anticipation of the FCC's deregulation of POTS. Wireless services continue to migrate to LTE as data to smart phones (inclusive of video and applications) is now a driving force.

Industry consolidation will continue. Look for a Sprint and T-Mobile merger to become a strong #3 player as SoftBank continues its push into the US market. AT&T may launch a friendly acquisition of Vodafone's EU business as the next wave of wireless consolidations shifts north and overseas. The “Big Four” in cable will become the “Big 3” as Time Warner Cable ultimately accepts a deal from Charter, Comcast or Cox. Cablevision could be next.

Infrastructure investments are crucial for all mobile players — spectrum wars will increase. For businesses, the top two trends to watch are Bring Your Own Device (BYOD) and security. With the future of Blackberry in question, many procurement leaders are planning alternatives.

More companies are expected to adopt BYOD practices, while ensuring adequate security protocols. Senior leaders at many firms are already being allowed to use their own tablets for work purposes, and these changes need to be built into any service provider relationship. Network security investment will be significant as privacy regulations and penalties become more onerous and companies recognize the potential resulting brand damage.

Business Travel

The global economy should pick up steam in 2014 and we expect business travel demand to follow suit. However, corporate travel demand grew slower than expected in 2013, so it is unclear as to how significantly businesses will step up their travel in 2014.

This looming question mark will keep suppliers cautious about pushing up fares. Barring any significant economic changes, overall price increases in the air, hotel and car sectors should be moderate, in line with inflation.

Buyers should focus their energies on higher transparency of the global travel data, consolidating the travel program to a single travel management company and fewer suppliers/alliances. Companies should also negotiate for the total cost of travel –including ancillary services — and use modern technology and social media platforms to engage business travelers to use contracted/preferred suppliers.

Energy & Utilities

Natural gas has largely reshaped the global energy market in the last few years and will continue to significantly impact the energy dynamics in the decades to come. In 2013, we saw many utilities and other energy-intensive industries increasingly choosing natural gas over traditional fuels like coal to achieve low emission targets and to move to a more versatile and affordable fuel. By around 2035, natural gas is expected to outstrip coal as the leading energy source for electricity generation, while oil remains the fuel of choice for transportation. Nuclear and renewable energy including – wind, solar, hydro and biofuels – will continue to support electricity needs and help industries meet targets for climate change mitigation.

In 2014, North American natural gas production driven by Marcellus shale gas output will likely be higher than the total demand, keeping electricity prices under control. In Northwestern Europe, the proposed Power Price Coupling to boost integration in the European power market would be a significant development to monitor. In addition to these developments, global liquefied natural gas (LNG) pricing may see increased linkage to gas over conventional oil price linkage.

As utilities respond to these changes, procurement professionals should take advantage of the market conditions – timing of procurement will continue to drive increased cost benefits and successful energy procurement decisions.

Equipment investment in 2014 is expected to grow across most verticals as economic fundamentals are looking strong and business confidence continues to recover.

Consumer spending growth is stable, households have low debt burdens and their wealth position is improving. Businesses are well positioned to make new investments in structure and equipment. With the euro zone coming out of recession, export activity is likely to pick up and boost business sentiment. MAPI forecasts that manufacturing production will increase 3.2 percent in 2014; high-tech production is forecast to grow by 7.6 percent and traditional manufacturing will grow by 3.1 percent in 2014.

The incipient housing market rebound will help wood products, nonmetallic mineral products, HVAC, household appliances, furniture and construction machinery. Mining and drilling equipment production should post modest gains in 2014, while high-tech industries (semiconductors, electronic computer equipment and communications equipment) should see accelerated growth. With this increase in spending, buyers will feel the need more than before to implement effective cross-function procurement practices and get involved early in the capital decision-making cycle.

Logistics

Shippers are facing conflicting pressures to manage complex, attenuated global supply chains while at the same time continually reducing the delivery time to customers. As the global economy continues its tepid and uneven recovery, shippers are expected to manage these competing priorities, while at the same time, holding fast or even reducing costs.

Traditional levers to reduce costs such as strategic sourcing, mode optimization and network optimization, are quickly becoming standard operating procedures for most organizations. To meet the increasing demands, shippers will need to focus on developing close partnerships with key global and regional carriers that can help shippers execute their business strategy.

Managing these partnerships will be key to ensuring success in 2014 and beyond. Shippers would be well-served to build a strategy to identify the right partners, build partnerships that are fair to both parties, and develop a network that is flexible enough to evolve as business needs change to help manage the overall cost of transportation.

Marketing

Agencies: Limited barriers to entry have allowed an ever-increasing number of specialized marketing technology and service providers to open shop and pitch their business. Marketers have endless options in constructing the optimal support model to fit their company culture and future brand goals. This is even more critical with the shift in channels, as seen in increased spending on digital ad agencies. Savvy marketers have a great opportunity to take advantage of this competitive landscape by evaluating their current service provider roster and making necessary changes to increase the efficiency and effectiveness of all partners throughout the value chain.

Improvements in technology also offer marketers the ability to better measure the results of their efforts. This allows companies to hold their agencies more accountable for the work they deliver. Procurement professionals should partner with marketing stakeholders to implement incentive-based compensation plans to ensure marketing targets are met and agencies are rewarded for pushing the limits and exceeding expectations.

Print and Promotions: We have seen many developed markets (including those stalled for years in Europe) begin to make progress in overcoming tough economic and financial challenges (for instance, a budget surplus in Greece). In 2014, we will continue to see increases in consumer confidence.

Companies will continue to see revenues rise as sales increase, supported by more advertising and promotion programs aimed at luring customers away from competitive products and cheaper substitutes. We believe that we are going to see a more active, more aggressive competitive environment in 2014, but smart deals can still be worked out, as the continued recovery anticipated in 2014 is (a) in its youth and (b) likely fragile.

To be sure, enterprise procurement teams should find themselves again in closer collaboration with enterprise sales and marketing teams, retail stores and suppliers to ensure the cost effectiveness of sales and promotional strategies, as these multiply in 2014.

HR Services

With economic upturns of one degree or another in the offing in North America and Europe, companies will turn their attention from cost control measures to expansion and growth in 2014, with higher demands on human resources organizations.

Some trends to incorporate into your thinking: the continued evolution of HR organizations from process managers and staffing facilitators to business partners; the continued transitioning of established processes to a shared services model; and increasing impact of social media platforms as recruitment engines, which is causing companies to expand their HR recruitment force, as opposed to relying on recruitment agencies. The contingent or temporary labor sector will also continue its recovery, driven by employers' need for flexibility, support for rapid expansion and limited internal capability to recruit skilled workers.

Moving to Master Service Providers (MSPs), implementing Vendor Management Solutions (VMS) and Human Resource Information System(HRIS) technologies will be top priorities to support companies' need for increased visibility and analytics-driven decision-making in the new HR organization framework.

Government regulations, such as the Affordable Care Act in the United States, and the Enterprise and Regulatory Reform Bill in United Kingdom, will require companies to adapt and adjust to reform. Thus, we foresee the demand for consulting services rising, as companies seek assistance to (a) adapt to regulatory change, (b) continue transitioning to a global shared services model, and (c) create operational centers of excellence.

Consulting companies, for their part, will try to pass on fee increases to their clients. With all these things in motion, there is ample opportunity for enterprise procurement teams to collaborate with human resources organizations on a significantly broader scale and help them actualize their transformation by identifying the right partnership model and suppliers for consulting, technology and outsourcing services.

Concluding Thoughts

The demand for procurement professionals will continue to rise in 2014 as corporations rely heavily on procurement and suppliers to add strategic value to their bottom line through increased savings and supplier-led innovation. Strategic relationships with suppliers and supplier risk management will continue to be key focus areas for procurement leaders.

Cloud and mobile procurement apps will allow increased automation of transactions and other procurement activities, and play a strategic role in taking procurement to the next level.