How the Strait of Hormuz Crisis Could Reshape Your Supply Chain Strategy

- Disruptions in the Strait of Hormuz have led to sudden rise in energy, freight, and input costs across global supply chains.

- Companies relying on single-region sourcing or lean inventory models will face the highest risk of delays and cost spikes.

- Real resilience comes from diversified sourcing, better visibility, and coordinated action powered by AI-driven procurement systems.

April 14, 2026 | Supply Chain Strategy 5 minutes read

Ongoing tensions around the Strait of Hormuz have pushed supply chain leaders back into crisis mode. Energy prices are swinging fast. Freight markets are reacting within days. And as this unfolds, procurement teams scramble for alternatives that were never fully mapped.

Many organizations assumed geopolitical shocks would stay regional. That assumption no longer holds. A disruption in one maritime choke point now hits manufacturing, logistics, and sourcing decisions at the same time.

Teams feel the strain because execution gaps already exist. Procurement and supply chain may align on resilience goals, but coordination is more likely to break under pressure, leading to slower decisions and higher costs. Hormuz exposes those cracks quickly.

Lead with Agentic AI

Build smarter and resilient supply chains through enterprise-proven technology

Why the Strait of Hormuz is Critical to Global Trade and Supply Chains

The Strait of Hormuz handles roughly one-fifth of global oil trade. Liquefied natural gas shipments also depend on it. That alone would make it important. The real issue sits deeper.

Energy flows shape everything else. Manufacturing costs, transportation rates, even supplier pricing models all tie back to fuel. When oil supply tightens, cost structures shift across entire value chains.

Asia depends heavily on crude shipments through this route. Europe relies on it to balance LNG requirements. The United States absorbs the shock through global pricing mechanisms rather than physical shortages. No region stays isolated.

Shipping lanes around Hormuz also connect key trade corridors between Asia, the Middle East, and Europe. Any disruption therefore forces rerouting. This adds time as well as cost. It also reduces available vessel capacity.

Procurement teams often underestimate this interconnectedness. Energy sits in indirect spend for many categories. Yet it quietly drives total cost.

When volatility spikes, contracts tied to stable assumptions start to fall apart.

Current Status of the Strait of Hormuz Crisis and Its Immediate Effects

Tensions and escalations in the region have led to increased military presence and have raised concerns over potential blockades or targeted disruptions. Even without a full shutdown, uncertainty alone has triggered market reactions.

Oil prices have seen sharp intraday swings. Freight insurance premiums for vessels crossing the region have climbed. Some carriers have begun contingency planning for alternate routes.

Short-term effects show up fast, such as:

- Spot freight rates increase

- Shipping schedules become less predictable

- Inventory buffers start rising

- Suppliers pass through fuel surcharges

Manufacturers that rely on just-in-time models are most likely to come under immediate pressure. Delays ripple through production schedules. Procurement teams face urgent renegotiations.

This pattern mirrors tariff shocks seen in recent years. Costs jump quickly, while supplier alternatives take longer to secure. Companies without visibility into supplier exposure struggle to respond in time.

The situation may not escalate into full disruption. But this uncertainty nonetheless creates its own problem. Teams often hesitate between reacting too early and reacting too late.

How AI & Predictive Analytics Strengthen Supply Chain Resilience in E&U

A must-read whitepaper for leaders to predict risks, reduce disruptions, and boost resilience

Ripple Effects on Energy, Commodities, and Industrial Supply Chains

Energy sits at the center, but the impact spreads wider.

Petrochemicals face direct exposure. Plastics, resins, and synthetic materials all depend on oil derivatives. Price volatility feeds straight into manufacturing inputs.

Metals and mining follow next. Extraction and processing depend heavily on energy. Rising fuel costs invariably push up aluminum, steel, and copper pricing.

Agriculture too does not have any escape route. Fertilizer production relies on natural gas, while transporting crops depends on the availability of diesel. Any shortage and food supply chains begin to absorb higher costs within weeks.

Industrial supply chains feel compounded effects, such as:

- Higher input costs

- Longer lead times

- Reduced supplier reliability

- Increased working capital needs

Companies with concentrated supplier bases face higher risk. Those relying on single-region sourcing struggle to pivot.

The lesson echoes from tariff disruptions. Supply chains built purely for cost efficiency fail under stress. Resilience requires structural changes, not temporary fixes.

Check Out GEP’s Supply Chain Consulting Services

Strategic Actions to Adapt Your Supply Chain Strategy During the Hormuz Crisis

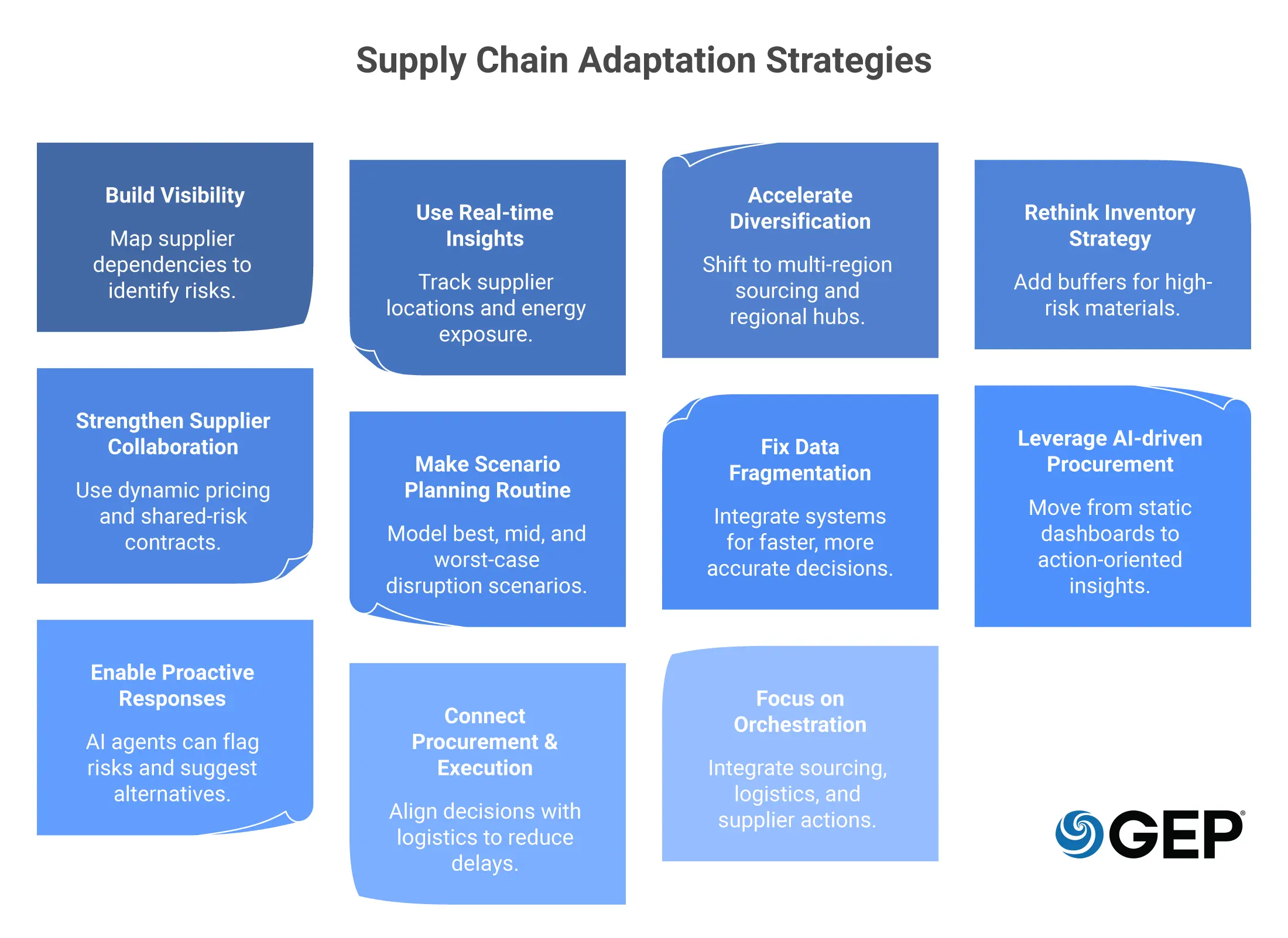

Start with visibility. Many organizations still lack clear mapping of supplier dependencies across tiers. Without that, risk remains theoretical.

Real-time insights into supplier locations, logistics routes, and energy exposure change response speed. Teams can identify which categories face immediate risk and which can wait.

Diversification needs to move faster. Multi-region sourcing is no longer optional for critical categories. Nearshoring and regional hubs reduce dependency on single trade corridors.

Inventory strategy needs adjustment. Lean models break under volatility. Strategic buffers for high-risk materials provide breathing room when disruptions hit.

Supplier collaboration has to be more active. Static contracts cannot handle rapid cost swings. Dynamic pricing models and shared risk clauses reduce friction during renegotiation.

Scenario planning must become routine. Teams should model best-case, mid-case, and worst-case disruption scenarios. This includes transport delays, fuel cost spikes, and supplier shutdowns.

Technology plays a role, but only when data is ready. Many organizations still operate with fragmented systems. More than half report incomplete data integration, limiting their ability to act quickly.

This is where procurement platforms with AI agents begin to matter.

Traditional tools provide dashboards. They show what happened but rarely guide action in real time.

AI agents can monitor geopolitical signals, track supplier risk, and trigger predefined responses. They can recommend alternative suppliers, adjust sourcing events, and flag contract exposures as conditions change.

More importantly, they connect procurement with supply chain execution. That alignment reduces delays between insight and action. It cuts cycle times and limits cost escalation.

Orchestration becomes critical here. It connects sourcing decisions, logistics adjustments, and supplier collaboration into one flow. Without that coordination, even good insights fail in execution.

Stay ahead of disruptions with actionable insights from GEP’s Hormuz Advisory.

FAQs

The crisis in the Strait of Hormuz has disrupted energy flows, leading to higher fuel costs, freight rates, and input prices. This has led to delays, increase in procurement costs, and reduced supplier reliability across industries.

Although there is no industry completely unaffected by the disruption, energy, petrochemicals, manufacturing, automotive, agriculture, and logistics face the highest impact due to direct or indirect dependence on oil and gas.