AI Growth Hits a Wall: Power, Not Chips, Limits Scale

- Power shortages delay AI infrastructure and data center expansion.

- Supply chains struggle with equipment, tariffs, and grid constraints.

- Procurement must shift toward power-aware, orchestrated decision-making.

March 30, 2026 | Risk Management 6 minutes read

Early 2026 forced a reset. Computing capacity was no longer the bottleneck. Power availability took its place.

Global data center electricity demand is set to exceed 1,000 TWh this year, roughly equal to Japan’s annual consumption. The scale is hard to ignore because it reflects physical limits. Electricity cannot be scaled the way software can.

The industry spent years worrying about chips. That concern has not disappeared, but it no longer leads the conversation. Power does.

The gap is already visible. In North America, the difference between planned data center capacity and available grid power could reach 19 GW by 2028, according to a report by the Financial Times. Projects move forward. Power connections do not.

That gap carries financial weight. Each month of delay can cost about $3.1 million per 100 kW rack in lost revenue. Time-to-power now shapes returns in a direct way.

Looking for Ways to Protect Your Business from Disruptions

GEP can help you navigate unpredictability and protect margins with confidence

From Silicon Limits to Physical Infrastructure Gaps

The shift from chips to power exposes a deeper issue. Digital systems scale quickly. Physical systems do not.

Data centers can be designed and built in 18 to 24 months. Power transmission infrastructure can take 10 to 12 years from proposal to operation. That gap does not close easily. Regulation, approvals, and fragmented processes slow everything down.

Interconnection queues keep growing. As of early 2026, they exceed 2,000 GW in major markets, according to the Federal Energy Regulatory Commission. Projects wait in line while demand keeps rising.

Site selection has changed as a result. Energy availability now matters more than labor or tax incentives. That would have sounded extreme a few years ago. It no longer does.

Equipment Bottlenecks Are Getting Worse

Grid expansion depends on equipment that is increasingly hard to source.

High-voltage transformers have become a major constraint. Lead times have stretched from 16 weeks in 2021 to between 115 and 140 weeks in early 2026. Prices have increased to nearly four times 2021 levels.

The issue runs deeper than manufacturing capacity. Transformers depend on grain-oriented electrical steel, a material produced by only a few mills globally. That concentration creates fragility.

Procurement teams cannot resolve this with traditional sourcing tactics. The constraint sits upstream.

Trade Policies Add Another Layer of Pressure

Energy transition plans run into geopolitical realities.

Solar supply chains remain uneven. Tariffs and trade restrictions have pushed U.S. solar hardware costs about 40% higher than in Europe and three times higher than in China.

With some duties getting exponentially high for specific exporters. That effectively removes suppliers from the market.

Enterprises respond by locking in long-term partnerships instead of relying on spot purchases. They secure capacity years in advance to avoid sudden disruptions.

That approach reduces exposure, but it also ties up capital and limits flexibility.

Check out GEP’s AI-Powered Supply Chain Management Software

Efficiency Gains Help, But Do Not Close the Gap

Rising demand has pushed companies to rethink how energy is used inside data centers.

Rack density has increased from 15 kW in 2023 to more than 100 kW in advanced AI clusters. Traditional cooling methods struggle at that level.

Direct-to-chip liquid cooling is becoming standard. It brings power usage effectiveness down to around 1.05–1.1. In practical terms, that frees up close to 20% more power for computing.

Some operators go further. They capture waste heat and reuse it in nearby industrial processes. That reduces overall energy waste.

These improvements matter. They still operate within the same physical limits.

Where Current AI Tools Fall Short

Most AI tools in procurement focus on process efficiency. They improve sourcing, automate workflows, and enhance forecasting.

Those capabilities help. They do not address constraints outside the system.

AI models assume supply can respond once demand is identified. That assumption breaks when infrastructure takes years to build.

They also depend on clean, integrated data. Multi-tier supply chain visibility remains limited in many organizations. Risks often sit with Tier 2 or Tier 3 suppliers, where data is incomplete.

Policy-driven disruptions create another blind spot. Tariffs and regulatory changes can shift cost structures quickly. Historical data does not always prepare models for those shifts.

The result is a gap between insight and execution. Teams see the problem but cannot act fast enough.

A Shift Toward Infrastructure-Led Procurement

Procurement is moving beyond supplier selection. It now intersects with infrastructure planning.

Companies are starting to take control of power access. Some co-invest in substation upgrades to move ahead of utility queues. Others build onsite generation and storage to reduce reliance on the grid.

This approach changes the role of procurement. Decisions now include energy availability, equipment lead times, and regulatory exposure alongside cost.

Coordination becomes harder. More variables enter the process. Timelines stretch across multiple domains.

A Unified Strategy & Blueprint for AI Power Readiness

Explore how time-to-power is shaping investment and site selection

How AI Agents Fit Into This Shift

AI agents operate differently from traditional tools. They connect decisions across functions instead of optimizing isolated tasks.

They map dependencies across supply chains, infrastructure, and regulatory processes. A delay in transformer supply can trigger adjustments in project timelines and sourcing strategies early.

Cost modeling becomes more dynamic. Agents track materials like copper and aluminum, update should-cost models, and flag deviations before they escalate.

Energy sourcing also changes. Agents evaluate supplier networks, tariff exposure, and production timelines together. That supports long-term contracting decisions rather than short-term purchases.

Risk visibility improves when data is connected across tiers. Disruptions can be identified earlier, even when they originate deep in the supply chain.

Check Out GEP's Should Cost Modeling Software

Building Operational Independence

Some companies are moving toward partial independence from traditional grids.

“Bring your own power” models combine on-site generation with energy storage. This allows companies to deploy capacity without waiting for grid readiness.

Virtual power plants add another layer. Stored energy can be fed back into the grid, creating an additional revenue stream.

These models require coordination across procurement, engineering, and operations. AI agents help manage that complexity by aligning data and timelines.

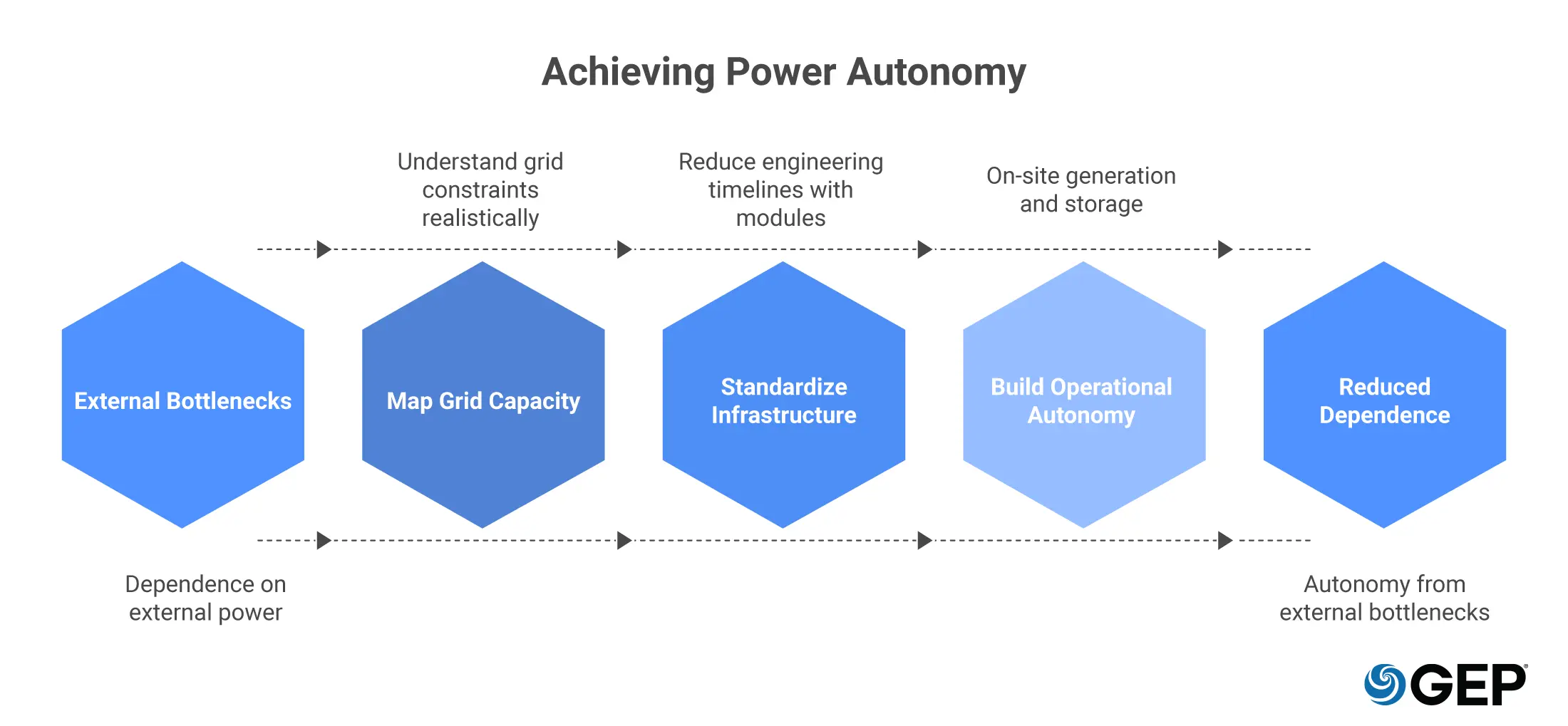

A Practical Path Forward

The shift to power-aware procurement does not happen all at once.

Initial steps focus on mapping grid capacity, equipment availability, and interconnection timelines. That creates a realistic view of constraints.

The next phase involves standardizing infrastructure components. Modular designs can reduce engineering timelines by around 40%.

Longer term, companies build operational autonomy through on-site generation and storage. Some explore nuclear options such as small modular reactors to support continuous demand.

Each step reduces dependence on external bottlenecks.

The New Reality for Procurement

Computing capacity and power capacity are now tightly linked. One cannot scale without the other. Companies that secure power early gain an advantage. Estimates suggest up to 30% faster time-to-compute for those that bypass grid delays.

That advantage compounds over time.

Procurement teams sit at the center of this shift. Their role now includes managing physical constraints, not just commercial ones.

The tools are changing as the expectations get higher. Power is no longer a background consideration. It defines what gets built and when.

FAQs

Power has become the primary constraint because AI infrastructure now scales faster than energy systems can support. Data centers can be built within 18–24 months, but power infrastructure such as transmission lines can take 10–12 years to develop.

This mismatch between rapid compute expansion and slow energy infrastructure development has shifted the bottleneck from chips to electricity availability.

Procurement teams need to expand their scope beyond supplier sourcing and include infrastructure readiness in decision-making. This includes evaluating power availability, equipment lead times, and regulatory delays alongside cost.

Advanced procurement platforms with AI agents help by connecting data across supply chains, infrastructure, and risk layers. Teams are also adopting new models such as co-investing in grid infrastructure or building on-site power capacity to reduce dependency on utilities.