The Path to Stable and Compliant Banking Procurement Services

- Procurement becomes the bridge between operations, technology, and regulation.

- Banking resilience depends on how well third-party dependencies are governed.

- The safest move is one that detects risk early, not the one that reacts fastest.

March 24, 2026 | Procurement Strategy 6 minutes read

Most people think banks run on capital. But in reality, they run on decisions made far away from trading floors and credit committees. These could be decisions about vendors, software, services, or risks associated.

Every contract signed and renewed, and every supplier chosen, quietly defines cost, resilience, and compliance long before quarterly results. With rising regulatory scrutiny, procurement risks high operating costs.

Banking procurement has long gone beyond managing transactions. Today, it governs how technology is introduced, how third parties access sensitive data, and how operational risk accumulates over time. Which means execution matters more than intention. Because in banking, risk rarely begins with a market event. It begins with an unnoticed dependency.

This article explores how procurement operates inside financial institutions, where it weakens at scale, and how AI is changing the way those decisions are made.

What Are Banking Procurement Services?

Everyday operations rely on software providers, payment networks, data processors, consultants, facilities vendors, and hundreds of other third parties. Operational purchases extend into complex technology platforms and specialized advisory services.

Banking procurement is the function that decides who those partners are and how they are controlled.

In banking, a supplier is never just a supplier. It’s a lot more. A cost decision, a security decision, and a compliance decision at the same time. The primary purpose is to always keep the bank operating safely, consistently, and within regulations.

Bring Control Back to Banking Procurement

Explore how to reliably modernize procurement with a purpose-built solution

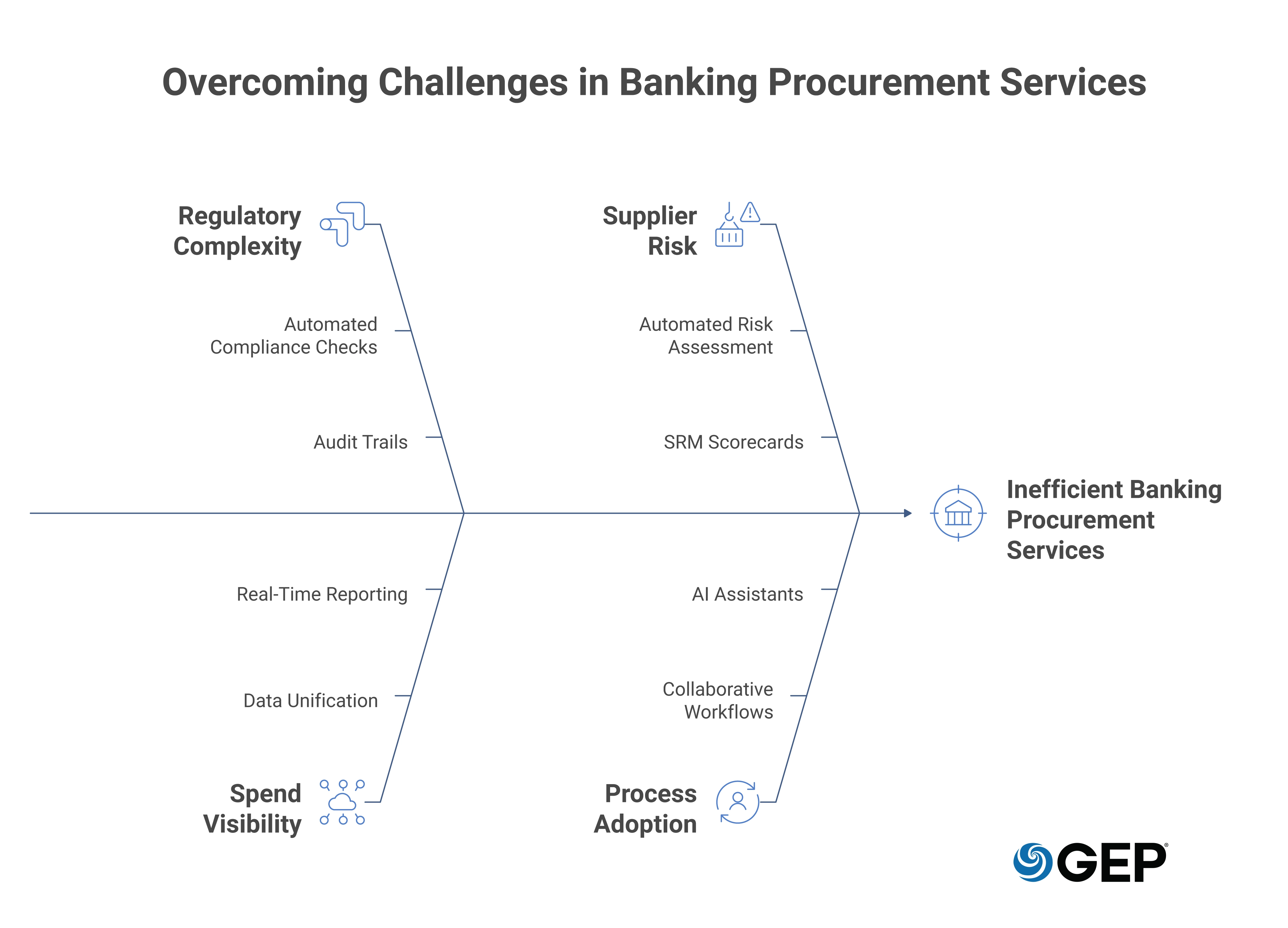

Critical Challenges Impacting Banking Procurement Services (And Why They Matter)

Banking procurement carries more responsibility than most functions appear to hold.

Every supplier choice touches regulation, cost, and operational stability at the same time. And the pressure builds from several directions at once.

Regulatory Complexity

Frameworks such as Basel III and Anti-Money Laundering (AML) requirements turn supplier decisions into compliance decisions. Every contract must be defensible and traceable.

It’s not enough to follow policy. The bank has to prove it followed policy every time. The only sustainable response is to embed policy checks, due diligence, and audit trails directly into daily workflow.

Non-compliance can result in hefty fines and regulatory sanctions.

Data Security and Privacy Challenge

Every vendor connected to the bank becomes part of its security perimeter.

Sharing sensitive financial data with third-party vendors creates significant security vulnerabilities and privacy concerns. Cloud platforms, data processors, and service partners handle sensitive financial information.

Vendor security incidents can expose sensitive customer data, and violations can trigger severe penalties. Make security validation contractual. The contract must cover all risk management protocols the vendor will be responsible for if such an event occurs in the near future.

Limited Visibility Hinders Timely Damage-Control

Banks often cannot see their own purchasing behavior clearly. Spend data builds across disconnected systems, business units, and contracts, and teams often don’t see the full picture.

Without a unified view of centralized data processed and structured in real time, duplicate suppliers and uncontrolled spending will go unnoticed.

Supplier Risk Follows Dependence

Banks rely heavily on technology and service partners, but it’s not unknown that reviews occur periodically. Performance degradation, financial instability, or cybersecurity exposure develops gradually between those reviews.

Vendor failures can disrupt core banking services. Breaches reflect directly on the bank's reputation. Moreover, overreliance on single vendors increases operational risk and weakens negotiating positions.

Make risk monitoring continuous, and use structured performance scoring as leverage to differentiate between reactive and preventive suppliers.

Process Adoption and Talent Management

Controls only work if people use them. When procurement workflows are slow or complex, business teams bypass them. Each workaround reduces compliance and visibility even when policies are well designed.

Assisted decisions and streamlined workflows encourage participation, restoring governance with usability.

Cost Pressure and Sourcing Tradeoffs

Banks must reduce spend without reducing reliability. Effective sourcing requires understanding demand patterns, negotiating from data, and evaluating tradeoffs before contracts are signed, not after budgets tighten.

Capacity Limits Execution

Banking services are expected to run seamlessly 24/7. Legacy systems don’t let teams handle large-scale, high-volume work. Automation handles repetitive tasks so people can focus on evaluation and decision-making.

Strategic sourcing supported by AI-assisted negotiation reshapes how cost tradeoffs are evaluated. Let human effort concentrate on evaluation, critical exceptions, and strategic choices.

The challenges facing banking procurement are complex and interconnected. Success in banking procurement won’t come from addressing one issue in isolation. Procurement leaders must redesign workflows to affect how decisions are executed at speed, in real-time, and at scale.

Is Your Spend Strategy Ready for 2026?

Respond to supply shifts faster with data-led, strategic guidance

Advantages of Procurement Services in the Banking Industry

You don’t usually notice strong procurement in a bank. But your customer will notice the absence of disruption. Internally, teams notice when costs stop fluctuating unexpectedly, and day-to-day operations move without friction.

Cost Savings

When purchasing is consolidated and informed by real spend insight, pricing stabilizes and contract terms align. Savings stop appearing as isolated wins and start appearing as predictable outcomes.

As manual handling disappears, work accelerates. Digital requests, automated approvals, and integrated invoicing shorten cycles and reduce error. Teams spend less time moving transactions and more time evaluating them.

Consistency

Working with vetted suppliers and measuring performance against clear expectations prevents quality from drifting. Problems surface early, often before business teams feel them. Supplier relationships shift from transactional to deliberate, which strengthens cooperation and negotiating position over time.

Governance

When approvals and documentation live inside the workflow, compliance no longer depends on reconstruction. The organization can demonstrate control as decisions happen rather than after review.

Visibility

Real-time insight into spending patterns informs budgeting, sourcing, and forecasting. Procurement becomes a source of operational awareness rather than a record of past activity.

Innovation

New technology and services move from evaluation to deployment faster because onboarding no longer stalls inside administrative delay.

Resilience

Continuous supplier vetting, financial and cybersecurity checks, and diversified sourcing reduce exposure to disruption. When issues occur, they remain contained instead of becoming operational crises.

In banking, effective procurement doesn’t simply manage purchasing. It creates stability which allows the entire organization to move with confidence.

Also Read: Sourcing Diversity: Beyond the Usual Suppliers

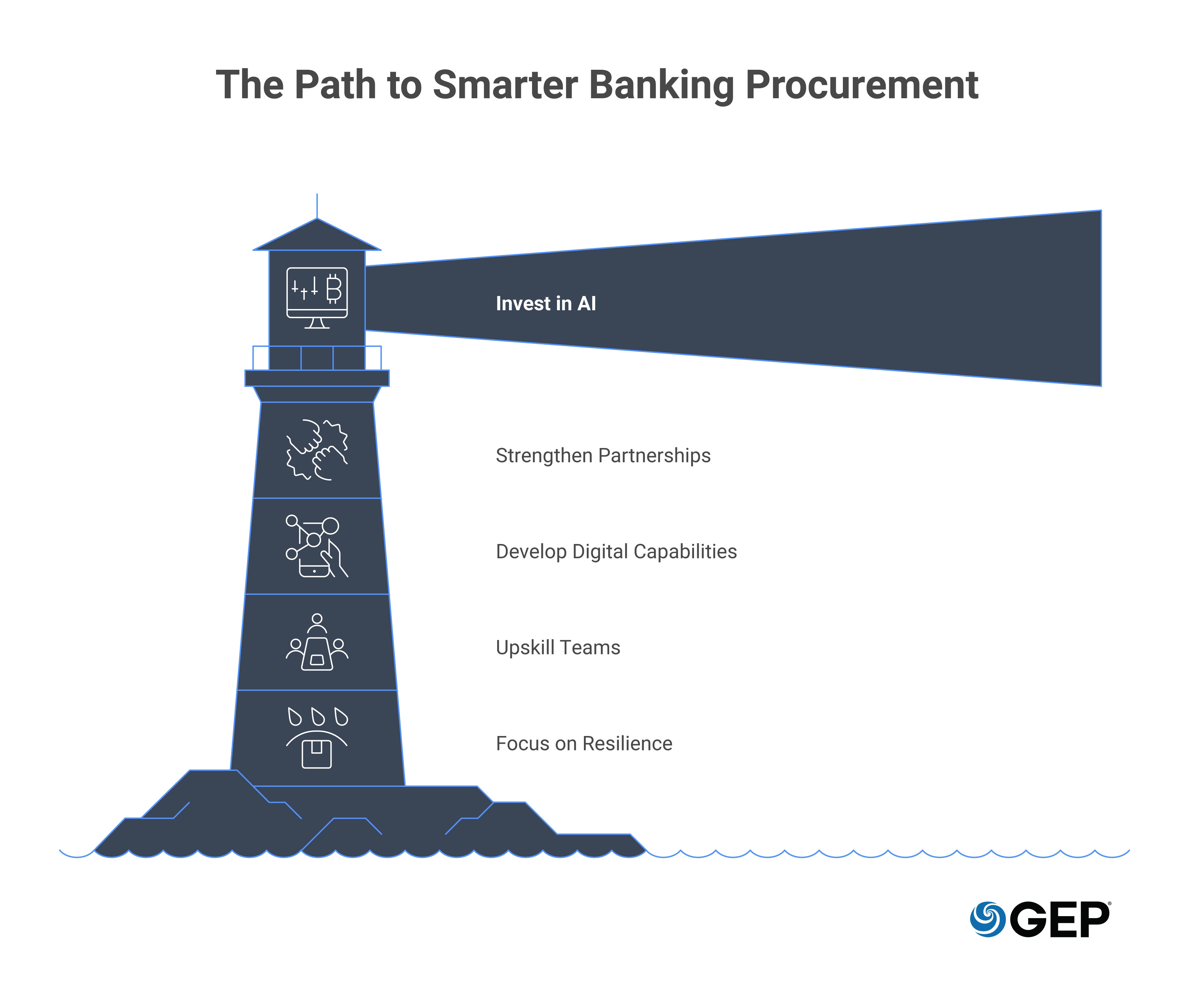

Future Trends in Banking Procurement

The future of banking procurement will focus on preparedness through agile technology and self-governing workflows.

AI emerges as the primary trend. Routine evaluation and monitoring won’t wait for review cycles. Systems will continuously interpret data and prepare decisions before teams look for them.

Procurement will become fully digital and truly autonomous. The integration of blockchain and public cloud services is expected to enhance procurement efficiency within the banking sector. Requests, approvals, contracts, and payments will begin moving through a single connected flow.

Supplier strategy changes, too. Banks rely on fewer partners but manage them more closely, treating them as operating extensions rather than interchangeable vendors.

Firms will adopt AI agents and agentic AI to make procurement seamless, compliant, and self-governing.

Instead of reacting to disruption, sourcing decisions will include monitoring and contingency planning from the start. Teams will spend less time gathering and analyzing information and more time evaluating trade-offs, risks, and impacts.

Begin Optimizing Your Banking Procurement Services

Banking procurement services need more control with minimal disruption and maximum compliance.

As AI takes on routine decisions, the real question is, can you trust how it acts?

Strong data and clear governance must be designed before automation begins. The institutions that benefit will be those that automate deliberately.

If you want procurement to reduce uncertainty instead of reacting to it, start by choosing technology built for financial oversight, not generic purchasing.

See how GEP helps banks design control into banking procurement services from the start.

FAQs

Integrated platforms connect sourcing, contracting, risk checks, and payment into one flow, while AI continuously monitors spend, supplier performance, and compliance signals. Teams see issues forming early and act before they become operational or regulatory problems.

Banks track total cost of ownership, contract compliance rates, cycle time, supplier performance reliability, audit readiness, risk exposure levels, and percentage of spend under management.

Every supplier decision carries regulatory responsibility. Due diligence, data security validation, and audit traceability influence vendor selection as much as cost or capability. Procurement, therefore, prioritizes defensibility and continuity, ensuring contracts, access, and performance can withstand regulatory review and operational stress before agreements are signed.