Chemicals & Plastics Procurement: What to Expect in the Second Half of 2022

- Chemicals & plastics industry has the most diversified end-use market across all manufacturing industries.

- The industry returned to growth in 2021 but a supply chain crunch prevented it from becoming stronger.

- The market is likely to stabilize in the second half of 2022 with a supply-demand balance.

June 16, 2022 | Sourcing Strategy 5 minutes read

Chemicals and plastics are used across all manufacturing industries as first- or second-tier materials. So, it is imperative for companies to keep a tab on the supply and demand of each C&P family and the competitive position in each region to define long-term business strategy.

Purchasing managers need to educate themselves at a granular level on each C&P family they buy to select suppliers that best fit long-term needs and also identify opportunities to source lower-cost materials.

Here are Some Trends Defining the C&P Market:

- The chemical industry returned to growth in 2021 but a supply chain crunch has prevented it from becoming stronger.

- With logistical obstacles clearing, expect stronger growth in 2022.

- The 2021 nightmare is likely to end by the second half of 2022 and prices are expected to stabilize.

How the Chemicals and Plastics Industry has Changed Since 2020

The demand for chemicals and plastics fell in 2020 amid the pandemic, and companies reduced their operating rates accordingly. By the end of the year, they lowered their inventory to show better numbers on the balance sheets.

Also Read: 12 Strategies To Diversify Your Supply Chain For Chemicals

To complicate things, January 2021 saw snowstorms in Texas and Louisiana, shutting down C&P plants for some weeks. Then the region faced four tropical storms from July to September (Elsa Fred, Nicholas and Ida), all of which wreaked havoc on plants across the region.

Understandably, chemical producers were saddled with low inventory, and plants were struggling to ramp up production, with the entire supply chain affected by the same conditions.

And during this period of supply disruption, demand for chemicals and plastics shot up. Prices naturally went up, with sales controls in place and product allocation affected across the board.

The recovery process put heavy demands on transportation — sea, rail, and truck — but as capacity was fixed, this took a long time to ramp up. The results were that a 40-feet container that cost around $7,000 in June 2021 jumped to more than $10,000 in September 2021, according to Drewry’s composite World Container Index. Vessels queued up in long lines at the ports; rail cars faced delays and trucking firms had loaded trucks without drivers.

Also Read: Covid-19 Impact on The Chemical Industry

When Will the Market Return to Normal?

The chemicals industry has two unique characteristics.

First, it has the most diversified end-use market across all manufacturing industries.

Second, its biggest customer is the chemical industry itself (27%).

Consequently, everything that is happening in C&P will affect all other industries.

Global C&P revenue fell 10% in 2020, according to the European Chemical Industry Council or CEFIC. However, it is likely the demand will increase at a compound average growth rate of 5% between 2020 and 2025.

Market Analysis Background

Our analysis will be restricted to chemicals that are consumed the most in the industry, also known as “commodity chemicals” (solid, liquid and gas). These include 136 products such as caustic soda, ethylene, propylene, methanol, and sulfuric acid.

For plastics, we have included 43 polymers (large molecules composed of repeated subunits), thermoplastics or thermosets, elastomers, rubbers, copolymers, or resins in any form (pellet, powder, liquid, etc.). Plastics products include polyethylene (LDPE, LLDPE, HDPE), PET, PP, PVC, amino resins, natural rubber, PS, ABS, PC, PVA, epoxy, silicone, and acrylics.

About the regions, the data was aggregated as North America, Latin America, Europe, the Middle East & Africa, and Asia-Pacific.

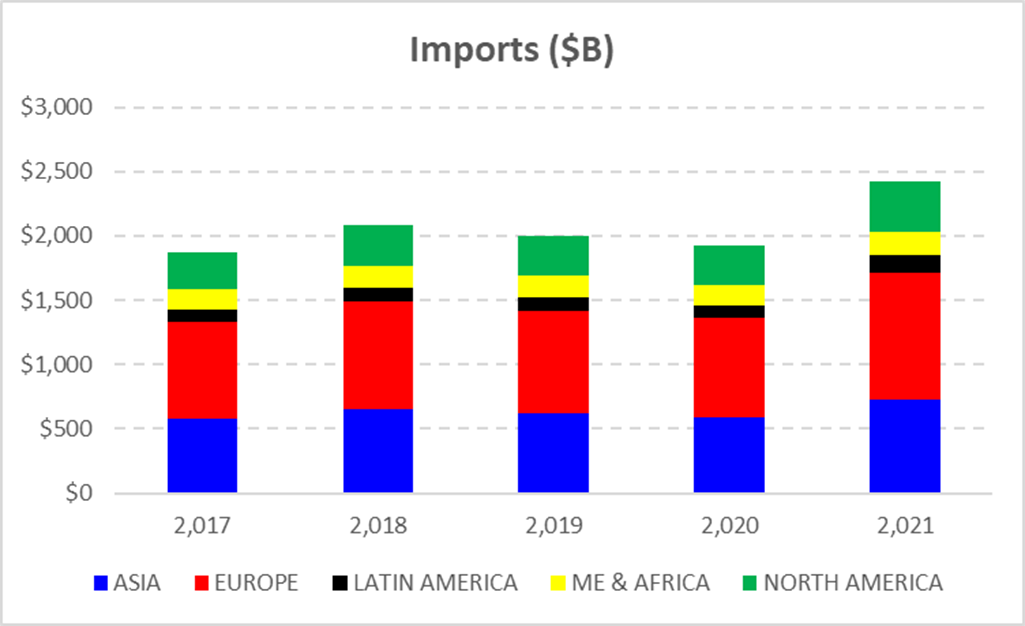

C&P Trade Has Been Growing

According to Trade Map, around $1.9 billion of C&P was traded in 2020, 5% lower than in 2019.

However, in 2021, C&P worth $2.4 billion was traded, which was 26% higher than in 2020.

Chart 1

Source: Trade Map

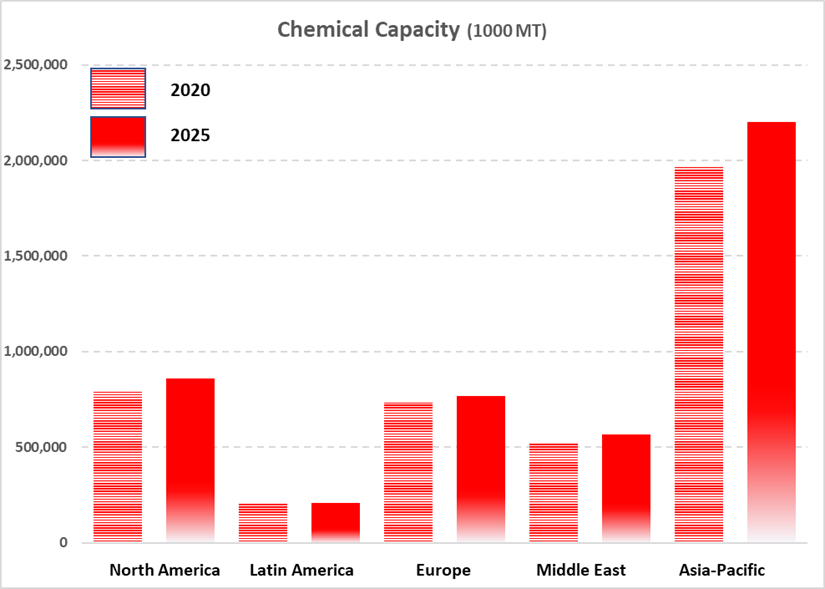

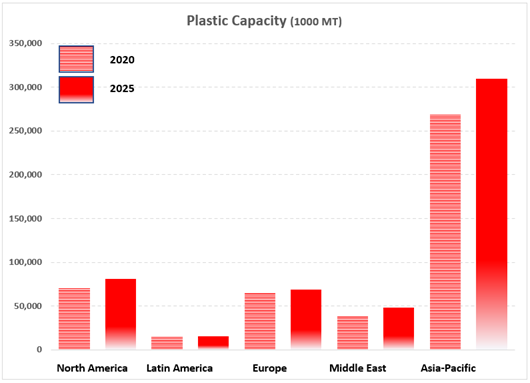

More Capacity for C&P

The global capacity for all chemicals in 2020 was around 4.2 billion metric tons (MT) (0.7% higher than 2019), where the Asia-Pacific region represented the highest capacity (48%) among regions (chart 4). The global capacity for all plastics families was around 492 million MT (7.6% higher than 2019), where Asia-Pacific again represented the highest capacity (59%) of all regions together. Note the difference in the scale of magnitude between chemicals and plastics.

Chart 2

Chart 3

As seen in charts 2 and 3, the installed capacity in the Asia-Pacific region was 49% of global capacity in 2020, followed by North America (18%), Europe (16%), the Middle East (12%), and Latin America (5%).

The high capacity, of course, means a high market demand in the region, but it also represents an alternative for purchasing officers to import from that region.

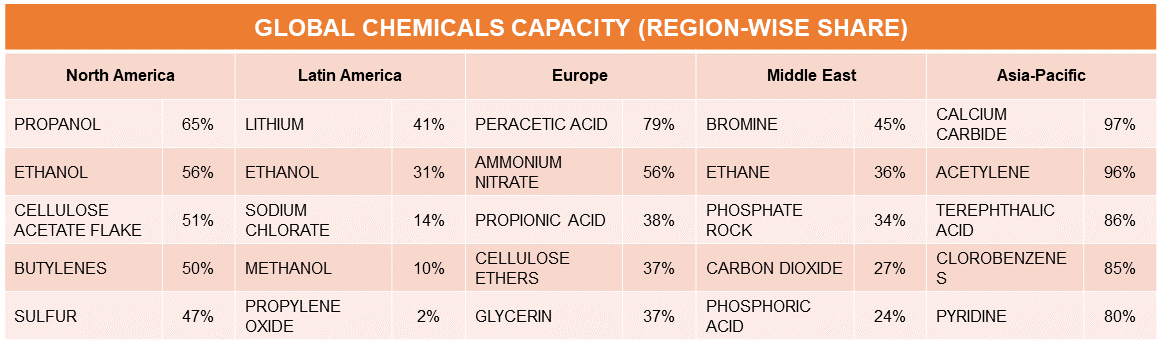

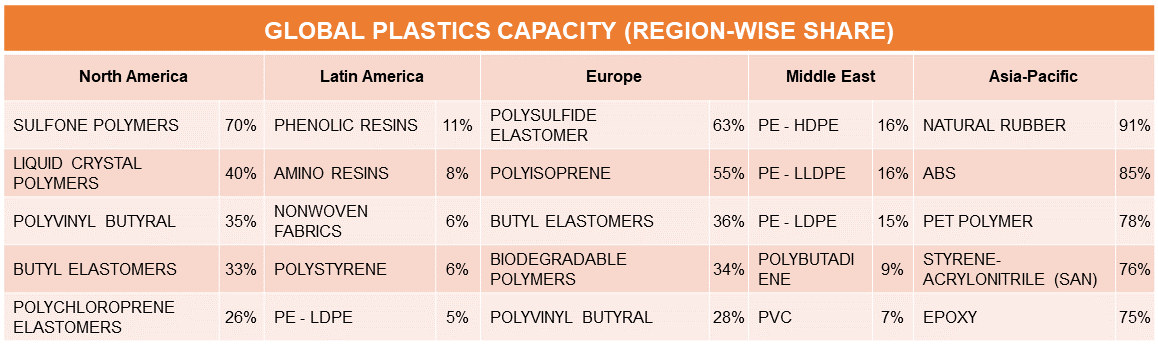

Some C&P capacities show higher concentrations in specific regions.

Table A shows, by region, which C&P has the highest concentrations of capacity (local capacity/global capacity).

Having a higher capacity concentration may mean that the region has an abundance of — and likely lower costs for — that specific feedstock. It could also mean lower total unit fixed costs (manufacturing and expenses) because of higher production volumes.

Consumers of these products should consider sourcing from these regions.

Table A

As expected, the operating rate for chemicals was 74% in 2020 versus 76% in 2019. For plastics in 2020, it was 68% in 2020 versus 74% in 2019.

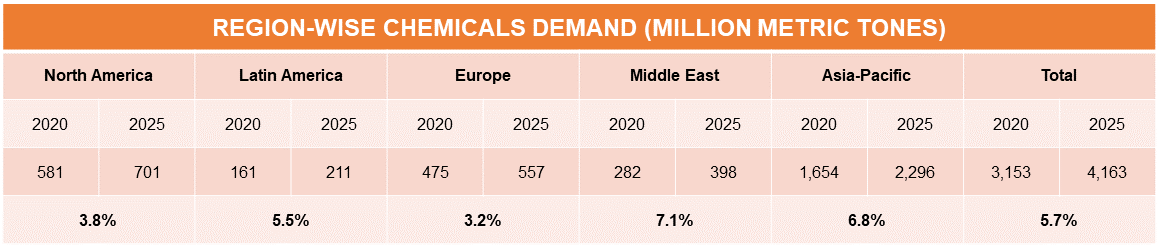

Changing Regional Demand Patterns

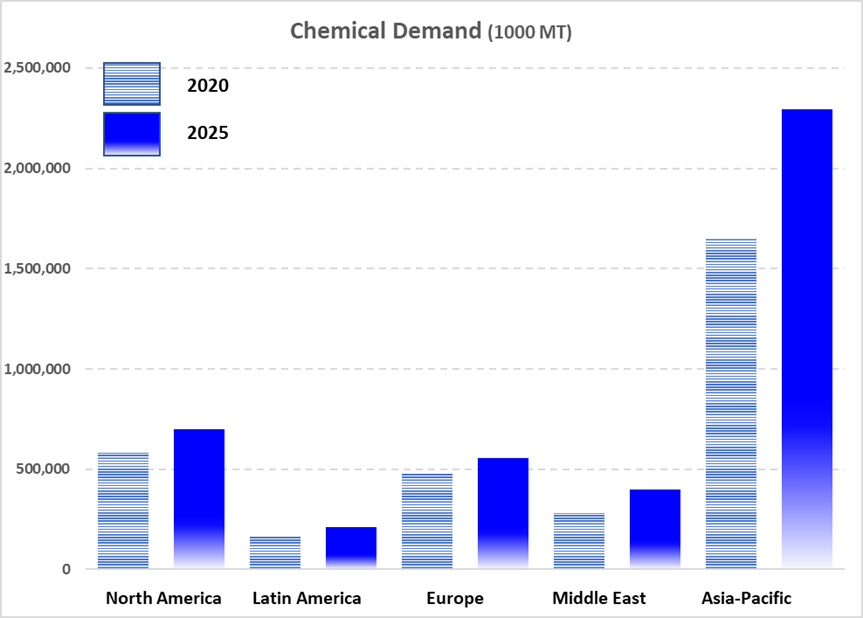

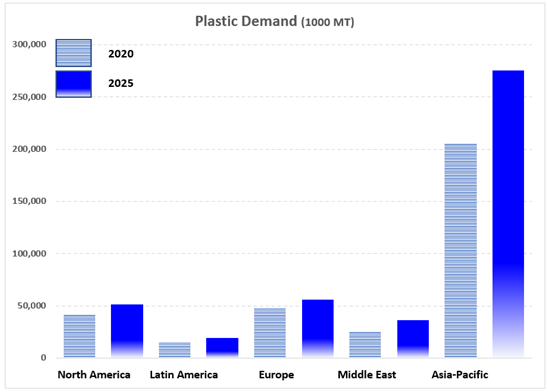

Charts 4 and 5 show the aggregated demand for chemicals and plastics in each region in 2020 and the estimated demand for 2025.

Chart 4

Chart 5

Like the capacity chart, the demand chart shows the same patterns between regions. The graphs above look very similar, but the scales are very different.

Ten plastics represent 84% of global demand: PET, HDPE, PVC, LLDPE, LDPE, amino resins, natural rubber, polystyrene, nonwoven fabric, and ABS.

In chemicals, 10 products represent 50% of global demand: sodium chloride, sulfuric acid, ammonia, ethylene, propylene, ethanol, urea, sulfur, methanol, and caustic soda.

Volumes Increasing

The compound annual growth rate (CAGR) is the growth rate in percentage year over year for a specific region. It reflects the growth of all end-use applications of that specific chemical or plastic in a region. Besides specific drivers, it is also driven by the overall growth of the region’s GDP and GDP per capita.

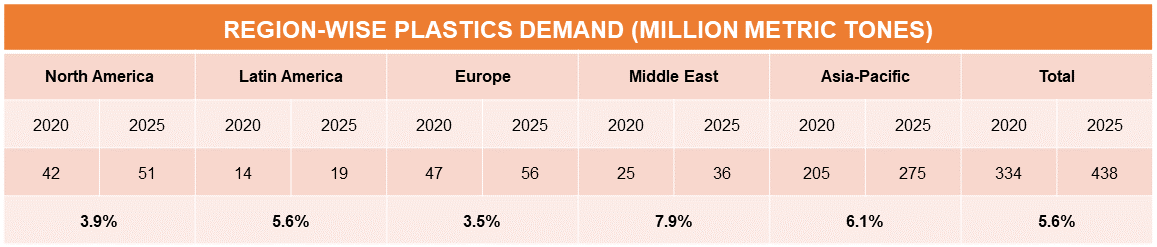

Table B shows the demand for 2020 and 2025 (predicted) with their respective CAGRs. The biggest volume increase for chemicals and plastics is in Asia, with the biggest growth in the Middle East.

Table B

Specifically at the product level, the biggest growth areas in chemicals will be rare earth minerals (13.1%), lactic acid (11.5%), lithium (8.8%), naphthalene (8.5%), and methanol (8.4%). Growth in plastics will be in biodegradable polymers (13.4%), styrenic block polymers (8.0%), non-wovens (7.7%), acrylic resins (7.5%), and silicones (7.4%).

Conclusion

High prices and shortages will continue up to the second quarter of 2022 but the second half of the year is likely to return to normal patterns in supply-demand balance and prices.

Paulo Moretti, the author of this blog, is a consultant with GEP and a veteran of the chemicals industry.