For most companies, Scope 3 emissions represent the largest source of greenhouse gases (GHG) emissions. These emissions stem from assets that are neither controlled nor owned by the organization, which means they can also be the most difficult to address. Yet, the global push for Net Zero coupled with looming government legislation has brought Scope 3 emissions to the forefront of sustainability and corporate strategies.

What are Scope 1, 2 and 3 Emissions?

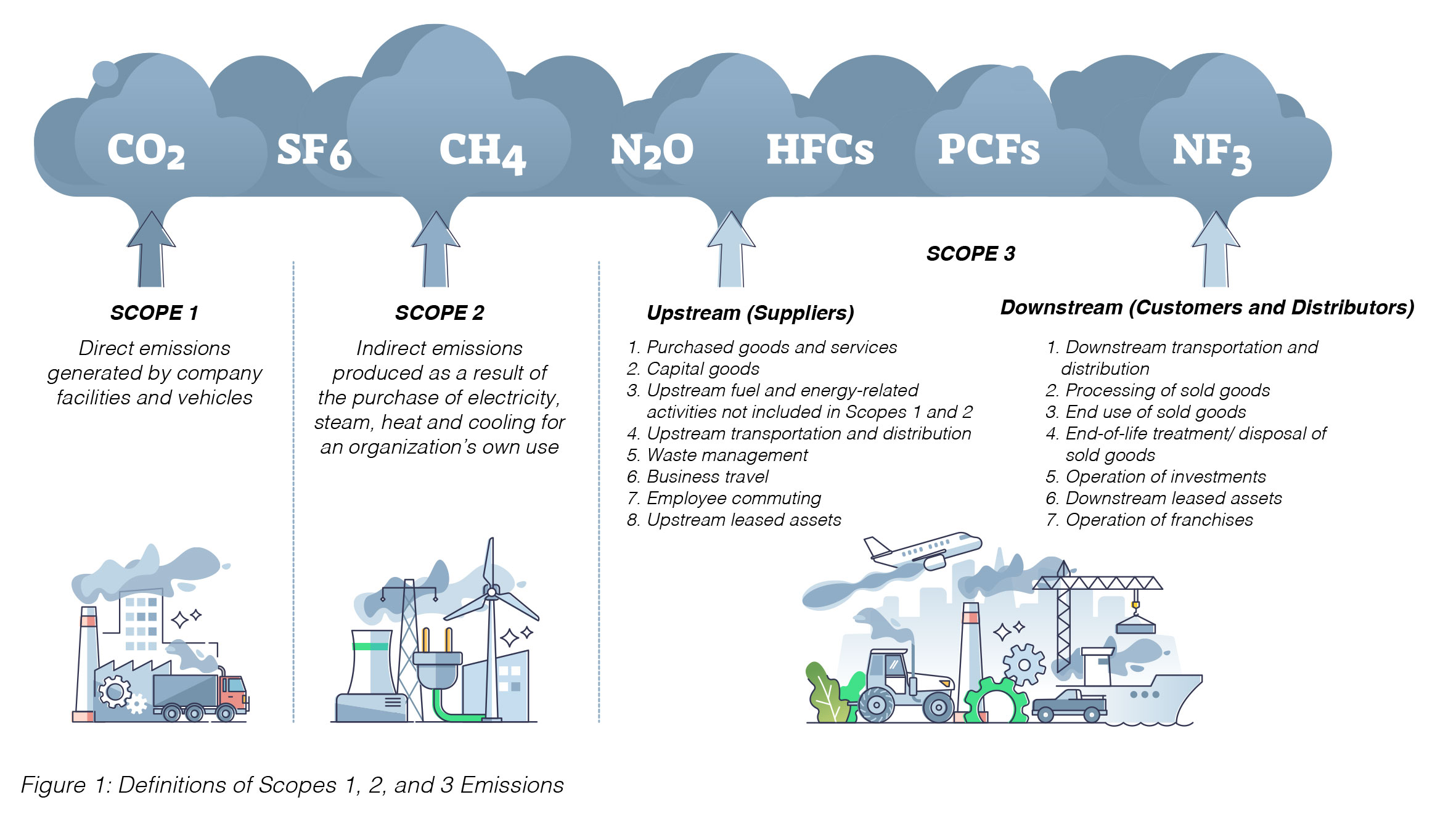

Corporate GHG emissions are tracked in the following categories.

Scope 1

Scope 1 emissions are direct emissions from owned or controlled sources.

Scope 2

Scope 2 emissions are indirect emissions from the generation of purchased energy.

Scope 3

This covers GHGs that occur in an organization’s value chain – such as purchased goods and services, employees commuting, and waste generated at various points in a supply chain.

Importance of Tracking Scope 3 emissions

Scope 3 emissions tracking has become imperative for supply chain organizations facing mounting regulatory requirements and stakeholder expectations. These indirect emissions, occurring throughout the value chain, typically represent over 70% of a company's carbon footprint, making them essential to meaningful sustainability initiatives. As regulatory frameworks such as the EU's Corporate Sustainability Reporting Directive and the SEC's climate disclosure rules expand, organizations without robust Scope 3 tracking face significant compliance risks.

Beyond regulatory concerns, customer and investor demands increasingly require transparent emissions reporting. Major enterprises now evaluate suppliers based on carbon performance, making Scope 3 tracking essential for maintaining market position. Forward-thinking organizations recognize that comprehensive emissions tracking identifies efficiency opportunities that simultaneously reduce environmental impact and operational costs.

Supply chain professionals understand that effective Scope 3 monitoring establishes the baseline necessary for credible reduction targets and enables comparative supplier evaluation based on carbon intensity. This data supports strategic sourcing decisions that prioritize environmentally responsible partners. Without accurate Scope 3 measurement, organizations cannot substantiate sustainability claims, risking reputational damage from greenwashing accusations. As carbon pricing mechanisms expand globally, quantifying these emissions becomes financially prudent, enabling organizations to anticipate future costs and implement preemptive mitigation strategies.

Currently Available Scope 3 Emission Categories

Scope 3 or value chain emissions are usually the largest of an organization’s total GHG emissions.

Scope 3 emissions are broken into 15 categories that include both upstream and downstream sources of emissions. Here are a few:

Purchased Goods and Services

- This category includes all upstream emissions from the production of products purchased or acquired by an organization.

- Products include both goods (tangible products) and services (intangible products).

Business Travel and Employee Commuting

- Business travel emissions include employees traveling for business-related activities in aircraft, trains, buses and cars.

- Employee commuting emissions include employees commuting between their homes and workplaces.

Scope 3 Upstream and Downstream Transportation and Distribution

- Scope 3 upstream transportation and distribution include emissions from the transportation and distribution of materials purchased using vehicles/facilities not owned or operated by the business.

- Scope 3 downstream transportation and distribution include emissions from transportation and distribution of products sold to the customer, using vehicles and facilities not owned or controlled by the business.

Waste Generated in Operations

This Scope 3 category is the waste generated from a company’s owned or controlled operations and the GHGs emitted from treating and disposing of that waste (including solid and wastewater) by a third party.

Why are Organizations Measuring Scope 3 Emissions?

In addition to proposed regulations and national targets, demonstrating a commitment to sustainability deep into the supply chain provides organizations with a true competitive advantage. However, you can’t measure what you don’t measure. So, organizations are looking into their value chain to measure Scope 3 emissions by fostering close collaboration with value chain partners and supplier networks and transparently sharing emissions data relative to the benchmarks set. The value chain approach to looking at carbon footprint focuses on reducing emissions from upstream activities and overall emissions from the business’s supply chain operations, thereby improving efficiency, resilience, and lowering costs.

Reducing scope 3 emissions is not just a crucial aspect of corporate sustainability strategies, but it’s an effort to preserve the world for future generations. While companies continue to make significant efforts to cut scope 3 emissions , there’s still a lot more to be milestones along the way to achieve net-zero carbon emissions. To this end, global businesses are increasingly seeking the help of scope 3 consulting services to identify and reduce their indirect emissions.

Scope 3 Carbon Accounting

Carbon accounting is the process of quantifying and reporting greenhouse gas emissions. It refers to estimating the amount of carbon dioxide equivalents a business emits, known as carbon credits – a commodity that is traded on carbon markets.

Current software systems provide carbon-accounting platforms that calculate emissions by assessing utility bills, travel, and logistics patterns; some platforms also link carbon footprint insights to offsetting marketplaces.

How Can Carbon Measurement Technology Help Supply Chain Companies?

Carbon measurement technology provides supply chain organizations with unprecedented visibility into emissions across complex global networks. Advanced platforms automatically collect and process carbon data from diverse sources including supplier systems, transportation providers, and facility operations. This automation eliminates the resource-intensive manual calculations that previously made comprehensive carbon accounting prohibitively expensive for many organizations.

This technology enables granular measurement down to individual product carbon footprints through sophisticated allocation methodologies and life-cycle assessment capabilities. This product-level transparency supports informed decision-making and enables carbon labeling initiatives that meet growing consumer demands for environmental information. Artificial intelligence and machine learning components identify patterns within carbon data, highlighting optimization opportunities that might otherwise remain hidden.

Scenario modeling capabilities enable supply chain professionals to evaluate carbon implications of network changes before implementation, supporting strategic planning that balances environmental and economic objectives. Real-time emissions dashboards provide immediate visibility into carbon performance against targets, enabling timely interventions when deviations occur. For multinational organizations, these systems incorporate region-specific emission factors and regulatory requirements, ensuring accuracy across diverse operating environments.

Beyond measurement, advanced platforms facilitate supplier engagement through collaborative data-sharing portals and capability-building resources. Integration with procurement systems enables carbon consideration during sourcing decisions by incorporating emissions data alongside traditional criteria like cost and quality.

As carbon taxation expands globally, these technologies will continue to provide the detailed accounting necessary for accurate financial planning and compliance reporting. Organizations leveraging these capabilities gain competitive advantages through improved operational efficiency, enhanced brand reputation, and demonstrated environmental leadership across their supply chains.

Conclusion

Climate change poses an existential threat to all, and the climate crisis could cause extreme damage to people, property, businesses and supply chains. Eighty-one percent of executives agree that businesses should make even greater efforts to protect the environment. This transformation means those who don’t adapt will be left behind, as is the case with Scope 3 emissions – primarily because the private sector is responsible for addressing this threat.

Furthermore, accurate scope 3 emission reporting has become essential for companies to not just understand their carbon footprint, but also to track their progress toward meeting emission reduction targets. Ultimately, effective management of scope 3 emissions is not only crucial for addressing the global climate crisis but also for achieving long-term business success and resilience.

Frequently Asked Questions

Scope 3 emissions are organized as upstream and downstream emissions.

Upstream emissions: Purchased goods and services, capital goods, fuel and energy-related activities not included in Scopes 1 and 2, upstream transportation and distribution, waste management, business travel, employee commuting and upstream leased assets.

Downstream emissions: Downstream transportation and distribution, processing of sold goods, end use of sold goods, end-of-life treatment/disposal of sold goods, operation of investments, downstream leased assets and operation of franchises.

In Scope 3 accounting, companies evaluate their end-to-end value chain emissions and their impact, and identify the focus areas for reduction.

Scope 3 emissions are typically the largest of an organization’s carbon footprint, so reporting Scope 3 emissions per global standards, such as GHG Protocol, Global Reporting Initiative (GRI) and Carbon Disclosure Project (CDP) transparency benchmarks, is essential. By reporting Scope 3 Emissions, businesses adhere to future regulatory requirements, create value for their stakeholders, and ensure reduced cost and enhanced efficiency.

Scope 3 Emissions cover indirect GHGs generated by an organization’s value chain – from purchased goods and services (upstream), employees traveling to and from work (downstream) to waste generated in supply chain operations (downstream).