Industrial Maintenance Services in North America

October 03, 2016 | MRO 2 minutes read

One of the key services used by the manufacturing and process industries in the MRO space is industrial maintenance services, comprising of mechanical, electrical, construction, industrial cleaning, scaffolding, welding and fabrication services. Over the years, end users have increasingly resorted to outsourcing of these services, as they were non-core and outsourcing enabled them to reduce costs by eliminating unnecessary equipment.

The North America industrial maintenance services market is valued at USD 186 billion in 2016 and is expected to grow at a compound annual growth rate of 4% during the next few years. When compared with other regions like Europe, LATAM and APAC, this segment is fairly mature in the US and Canada in terms of offerings from the suppliers and geographical coverage.

Some of the key players in the North American market are Johnson Controls, Jacobs, Flour, EMCOR, Safway, Brand, Veolia, MMR Group, Brock, Turner Industries. These are players with a wide geographic scope and service offerings.

Even the though the North American market is mature in comparison, the market is still highly fragmented. We expect the slow aggregation of smaller players by regional and nationwide firms to continue as end clients increasingly outsource end-to-end functions in maintenance services.

Players in this segment are expected to be highly competitive, as there is a lack of differentiation of service providers. Large integrated service providers are smaller in number and face stringent competition from local/regional players.

Lead with Agentic AI

Drive smarter procurement and resilient supply chains through enterprise-proven technology

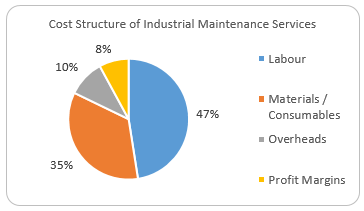

Key Cost Drivers

Two key drivers of cost are labour and consumables.

Margins are around 8 to 12%, depending on types of services. Scaffolding services are expected to have a higher margin than others, while mechanical services margins are expected to be about 5% with labor components around 35%.

Electrical services generally have a higher component of consumables. Electrical works which are control-based have higher raw material costs for control systems like motors and subassemblies, compared to non-controls.

In engaging with suppliers, the following are some of the key negotiation levers.

- Consumables Cost: Tools, spare parts and bolts constitute significant portions of purchases for mechanical services. Prices of such purchases are driven by commodity prices (aluminum, copper, steel). Spare parts are purchased from OEMs or wholesale distributors, depending upon the level of requirement. Though volume discounts from wholesale purchases are common, certain rare OEMs and selective spares can shoot up costs.

- Volume based: Large companies with higher bargaining power can negotiate for pricing based on service volumes and existing supplier relationships.

- Visibility of labor costs: Understanding the labor team structure and wages for different tasks will provide more visibility into the spend.

- Markup rates negotiation: Understanding the markup rates for different services and negotiation on the markup rates can bring the overall rates down.