How the Russia-Ukraine War is Changing Capex Strategies in Energy and Metals

- The reliance on Russia and Ukraine for oil and gas, nickel, palladium, titanium and neon are likely to create supply constraints

- This is boosting capital expenditure in other regions and sectors as buyers try to find alternative sources of supply

- Investments are expected to increase in renewable energy sources in the EU and in specialty metals mining in Asia

June 23, 2022 | Supply Chain Risk Management 5 minutes read

The Russia-Ukraine war is, expectedly, taking a heavy toll on both the economies. The Russian economy is projected to shrink by 7-15% as compared to the forecasted 2% growth before the February invasion.

The trade sanctions on Russia will create further supply chain issues, primarily in oil & gas and specialty metals — the core of Russian exports.1

The companies, whose supply chains are exposed to input materials from Russian and Ukrainian, are under pressure to invest in alternatives.

Energy: EU capital investments in LNG and renewables

Until 2021, the European Union and the U.K. relied heavily on Russia for oil & gas which made up 45% of their gas imports.

By end of 2022, the EU intends to look at alternative sources of gas from Norway and the U.S. This will be possible only with significant capital investment in liquified natural gas (LNG) terminals and interconnectors to reach consumers2.

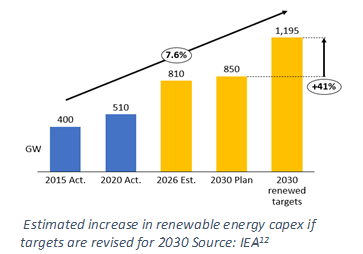

To further reduce reliance on Russian gas, the EU is also considering an ambitious renewable energy production target of ~45%9 instead of the earlier target of 32% by 2030. The accelerated targets could lead to significant investments in renewable energy upwards of 50 billion Euros and higher imports than previously forecasted.

The EU estimates that by accelerating the deployment of wind and solar projects, it would be able to reduce gas consumption by 6 billion cubic meters within a year3.

In addition to the above efforts, the EU also plans to incentivize replacement of gas-based heaters with heat pumps for household usage to further reduce its reliance on gas consumption and meet sustainability targets.3

Specialty metals: Investments to secure alternative nickel and palladium sources

Nickel is a critical element for steel production and batteries used in electric vehicles. There is a threat to the specialty metal’s supply with Russia being the third-largest supplier of nickel globally (20% of global nickel requirement).

Sourcing managers globally are now looking at other nickel reserves to replenish their stocks.

Indonesia, with its largest reserves, has augmented investments to build the country into a battery manufacturing hub.

In 2021 alone, Indonesia saw an investment of $5 billion10 from Chinese companies in nickel mining, purification, and battery manufacturing.4

Palladium is another key metal that Russia produces. It is used in automotive exhaust systems to mobile phones and even in dental fillings. Prices for palladium reached a lifetime high when the Ukraine war began but have since cooled after the consuming industries managed to find alternatives to the metal.

On the other hand, titanium, a key input metal for the aerospace industry, has its largest manufacturer, VSMPO AVISMA, based in Russia.

With more than 50% market share, and long-term contracts with key consumers such as Boeing and Airbus stretching up to 202811, it is imperative that buyers look for alternative titanium sources soon.

It will witness supply disruptions till the alternative sources based in Japan and the U.S. ramp up their ability to meet the demand.

With U.S.-based manufacturers such as TIMET, ATI, and Howmet Aerospace struggling with labor shortages and increasing costs following the pandemic, their ability to significantly hike production in the near term is uncertain.5

Neon gas: Will the balance shift from Ukraine to Asia?

Another key area with significant implications is the supply of neon gas, primarily used in chip lithography. Nearly 65% of global production of neon gas comes from Iceblink, a Ukraine-based refiner, which has halted production due to the war.

With most of the chipmakers overstocking for 1-2 months of the neon gas requirement, this hasn’t yet been identified as a concern.

But chipmakers are likely to face supply disruptions hitting the chip production at some point.

Ukraine has perfected the purification technology making it a major supplier of neon gas. The technology for purification of neon, which is a by-product of steel production, is not a secret, though perfection and scaling of the process can only be achieved over time with significant capital investments. 6,8

With China and India producing 62% of the world’s steel, neon gas could be harvested with the required capex.

Is it possible we see the scales of neon production tipping over from Ukraine to another economy in Asia? China could gain from this war in terms of technology and sourcing destination, helping it become a semiconductor powerhouse in the coming years.7

Conclusion

With supply chain reliance on Russia for key elements like oil and gas and metals, the constraints on supply will create some distress.

However, this will boost capital investments in other regions as buyers try to find alternative sources of supply. We foresee capex investments for renewable energy which will be the driving force to achieve the steep green energy targets.

At the same time, Indonesia and The Philippines might see enhanced investments to harvest their titanium and palladium reserves.

Apart from being cautious about the geopolitical situations on product supply, procurement managers can take this opportunity to explore alternative sources of supply, substitution, and product rationalization.

The blog has been authored by Chirag Murdeshwar, Abhinav Singh and Shashank Mohapatra of the GEP Capital Category Advisory Group.

To learn more about how GEP can help enterprises with capex strategies, please reach out to vipin.gupta@gep.com or chirag.murdeshwar@gep.com.

References:

1. Renaud Foucart, "The cost of war: How Russia's economy will struggle to pay the price of invading Ukraine", The Conversation, PTI and The Economic Times, March 14, 2022 | https://economictimes.indiatimes.com/news/international/world-news/the-cost-of-war-how-russias-economy-will-struggle-to-pay-the-price-of-invading-ukraine/articleshow/90194979.cms?

2. "Where does the crude oil come from?", Eurostat, June 07, 2022 |https://ec.europa.eu/eurostat/en/web/products-eurostat-news/-/ddn-20200507-1

3. "How Europe can cut natural gas imports from Russia significantly within a year," Press Release, IEA, March 03, 2022 | How Europe can cut natural gas imports from Russia significantly within a year - News - IEA

4. Isabelle Huber, "Indonesia’s Nickel Industrial Strategy", Center for Strategic and International Studies, December 8, 2021 | https://www.csis.org/analysis/indonesias-nickel-industrial-strategy

5. Fiona O'Neill, "Titanium and planes: Ukraine conflict spells new hit for global supply chains", Fidelity International, April 04, 2022 |https://www.fidelityinternational.com/editorial/article/titanium-and-planes-ukraine-conflict-spells-new-hit-for-global-supply-chains-cd01c8-en5/

6. “How is neon extracted and why does one country have a 90% monopoly (in this specific grade)?”, news.ycombinator.com (industry forum) | https://news.ycombinator.com/item?id=30457626

7. Global Neon Gas Market - 2021-2028, DataM Intelligence 4Market Research, June 2021 |https://www.marketresearch.com/DataM-Intelligence-4Market-Research-LLP-v4207/

8. Geoffrey Ozin, "Understanding the science behind the neon shortage", Advanced Science News, Mar 15, 2022 | https://www.advancedsciencenews.com/understanding-the-science-behind-the-neon-shortage/

9. "EU 'considering raising renewables targets'", RENEWS.BIZ.COM, April 20, 2022 | https://renews.biz/77297/eu-considering-raising-renewables-targets/?

10. "Indonesia says China's CATL plans to invest $5 billion in lithium battery plant", Reuters, Dec 15, 2020 | https://www.reuters.com/article/us-indonesia-nickel-china-idUSKBN28P0MK?

11. "Titanium supply threatened by Ukraine conflict: Update", Argus Media, Feb 28, 2022 | https://www.argusmedia.com/en/news/2304842-titanium-supply-threatened-by-ukraine-conflict-update

12. "Renewables 2021", IEA | https://iea.blob.core.windows.net/assets/5ae32253-7409-4f9a-a91d-1493ffb9777a/Renewables2021-Analysisandforecastto2026.pdf