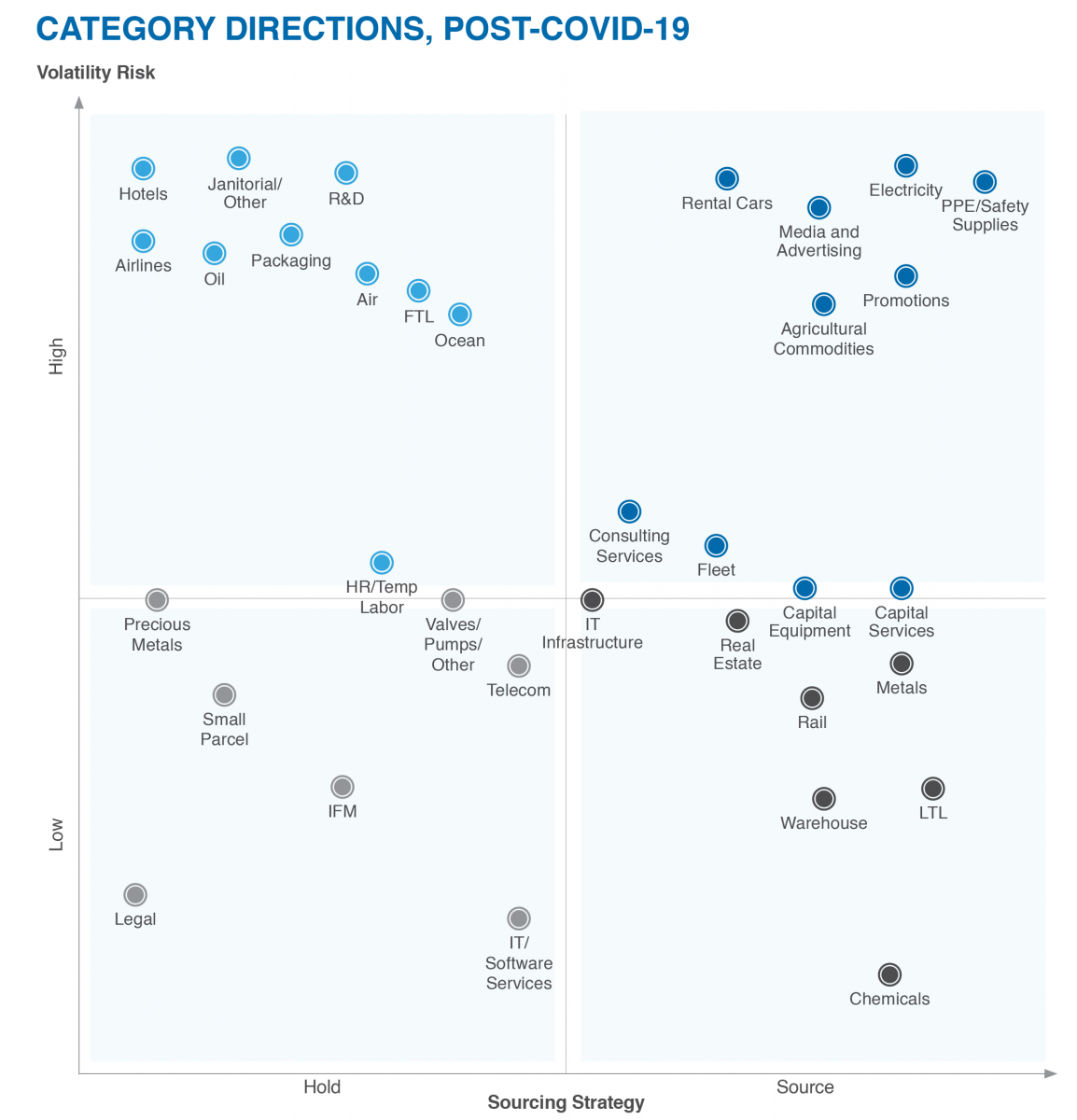

Everything you thought you knew about managing your key spend categories has just gone out the window, thanks to COVID-19. You need new information and guidance, fast.

What’s changed? What hasn’t? What should you do right now? What about in three or six months?

We provide critical insights, facts and figures in our special post-COVID-19 Category Outlook & Market Intelligence Report. Authored by GEP’s world-class category experts, this report examines changes in the top direct and indirect spend categories, helping you get a fast, firm grasp of the new market dynamics.

What’s Inside:

- Trends and insights into 15 indirect and direct spend categories

- Impact assessment of the COVID-19 crisis and global slowdown

- Market intelligence to explore new business possibilities

A must-read for those who want to make informed decisions that will put their companies on the path toward recovery and success.

INTRODUCTION

For more than 20 years, GEP’s global team of category advisory groups has managed billions of dollars of spend for leading Fortune 500 and similar businesses in all major industries, helping to chart their course through any and every economic environment. These efforts generate unparalleled market access to a deep pool of relevant, broadly generated knowledge capital. The end result: compelling supply market intelligence, resulting in new ideas and actionable insights brought together in one report that we create and share with the procurement and supply chain community on an ongoing basis.

The impact of the COVID-19 pandemic on companies large and small has been unprecedented, with rapid and thorough disruption of our interconnected global supply chain networks. Supply chain and procurement organizations are indispensable in managing this crisis. Businesses face the intense challenge not just to survive, but create opportunities that drive positive outcomes. Robust market intelligence is more important now than ever in the effort to achieve this goal.

This edition of our Category Outlook and Market Intelligence report explores top trends, challenges, and opportunities in every major category of spend, with focused, real-time perspectives on global developments around the COVID-19 crisis. During this trying time, our experts will not only provide the latest market intelligence and informed perspectives, but will also offer practical guidance to help business leaders navigate their organizations through rapidly changing market dynamics.

Providing supply chain stakeholders across the globe with the most current insights and actionable opportunities is our goal and motivation for publishing this report. For additional advice and materials, you can visit GEP’s COVID-19 Resource Center.

DIRECT MATERIALS CATEGORIES

CHEMICALS

The start of 2020 was an optimistic period for global chemicals, which had ended 2019 with nearly 2% yearon-year growth.1 Britain exiting the European Union and a partial resolution to the U.S.-China trade war had provided impetus for the market.

However, the COVID-19 pandemic coupled with an oil price slump and increased volatility have resulted in a bleak outlook for the year. The industry is expected to grow by just 0.2%; or it may even contract if the pandemic does not end soon.2

Swelling supplies of natural gas and oil are pressurizing the prices of key feedstock, thus providing favorable opportunities for large-scale buyers. The industry is already grappling with overcapacity for key chemicals such as C2, C3s, and derivatives — mainly resins. On the demand side, an overall decline in manufacturing, including production cuts by major automobile manufacturers across all regions, will free up plenty of chemicals, resulting in a supply-demand disparity in the near term and a mid- to long-term imbalance for the market.

Regional Trends

In 2020, the United States will continue to be a major chemical producer due to massive capacity expansion of basic feedstock such as ethylene and propylene along with key derivatives due to the abundant availability of shale gas and oil. However, with a slump in key demand sectors, prices are expected to plummet with marginal stabilization by the end of the year.

The European chemical market will continue to be marred by high operating costs and not-so-attractive margins, which might result in the industry contracting further. From a U.K. standpoint, decarbonization and policies post Brexit will dictate the overall impact on the European chemical industry.

The Asia-Pacific market will be driven by China and India, with the former looking at alternative markets for many chemicals due to the uncertainty over its trade terms with the U.S. Though the Chinese chemical industry has been under tremendous pressure due to environmental policies and the COVID-19 lockdown, production is expected to return to normal by the end of the second quarter. China’s central bank is also expected to cut lending rates to boost manufacturing.

Sub-Category Trends

Polymers

Most polymers are driven by crude oil, and with oil prices not expected to recover anytime soon, most of the polymers market may remain bearish for the rest of 2020. Though the demand for PET packaging is on the rise, an overflow of cheap Asian supply offers is putting pressure on prices.

Polypropylene demand remained steady for March, but we forecast a significant drop in demand on the back of massive cancellations of orders by large-scale converters. The demand for polymers from the global automotive sector is also expected to remain poor. This will lead to a further waning of demand and escalate the oversupply situation.

Aromatics and Solvents

Major chemicals such as benzene and toluene have seen massive price drops in all regions since the beginning of March, and the implications of the harm caused by COVID-19 and the oil market crash are discernible. Benzene dropped by 70% in Europe in March — the lowest since 2002.3 Closures of automobile units globally and continued overcapacity resulting in weaker dynamics for styrene have hit the benzene market hard. Key regions beyond Europe have also witnessed similar price drops.

Higher methanol demand in the U.S. caused European supply constraints. This resulted in surging value for methanol early in the quarter up until the pandemic broke out. Methanol will still be better placed than other solvents, as prices are expected to rebound in Q2 when demand revives. Spot prices across all regions are trending at historic lows, but this looks to be a temporary phenomenon.

Inorganics

Globally, the market for liquid caustic soda is moving contrary to the typical petrochemical market as its demand remains higher than that of its co-product chlorine. Caustic soda demand will be balanced in the near term as several planned and unplanned closures have occurred during these unprecedented market conditions. Lower demand for chlorine from the PVC industry will result in a continued shortage of caustic soda in the market, resulting in higher prices. Many caustic soda manufacturers have already announced an increase in contracts for April and May, with spot prices following suit.4

Demand for ammonia will continue to remain steady across regions, resulting in a balanced market for 2020. Quarterly contracts are likely to witness a rollover to the next couple of quarters in line with market expectations.

Looking Ahead

At this time, global category managers dealing with chemicals/feedstock/derivatives should focus on leveraging reduced feedstock prices and optimizing operating rates to take full advantage of the market situation. Formulabased pricing should be the major focus for all new contracts. Also, all fixed-price contracts will need to be renegotiated and rebates agreed upon for the next contractual purchase. Choosing the right formula will hold the key to successful negotiations. Comprehensive should-cost modeling will be crucial during supplier renegotiations, especially for the ones under fixed-price contracts. With the markets volatile, large-scale buyers ought to evaluate whether they need to postpone their contractual volume purchases and look at taking advantage of the spot market. Buyers should look at contracting only 70% to 80% of their new volumes, keeping the rest open to gain advantage from the market situation.

For the rest of 2020, we expect an overall price decrease in chemicals and plastics, allowing savings for endusers. As prices trend down at the producer level, the same trend is expected at the distributor level.

From a manufacturer’s standpoint, there will be more strategic mergers and acquisitions in the chemical industry later in 2020, probably by Q4, and in early 2021. Companies will look at rationalizing their product portfolios and how to benefit from scale and synergies to remain profitable. In general, the global chemical industry will be bracing for a protracted slump resulting in long-term implications for profitability.

Outlook for Key Chemicals in 2020

| Key Commodities | Global Situation | |||

|---|---|---|---|---|

| Supply | Demand | Price | Highlight | |

| Benzene | High | Low to steady | Drop* | Price dropped 28% from January across regions.5 The U.S. is a net importer. Price expected to decrease in Q2 with an anticipated marginal increase by Q4. The price change will affect the following supply chains: styrenics, phenol, adipic acid, and caprolactam |

| Styrene | High | Low | Drop | Prices dropped in Q1 and follow the benzene trend. Demand from derivatives ABS and SBR will be low due to the slowdown in the automobile and tire industries, as well as from PS and EPS following slumps in the packaging and construction industries |

| Phenol | Balanced | Low to balanced | Drop | Price dropped 17% following benzene.6 As the U.S. is a net exporter, the product will flow to Europe and Asia. Phenol derivatives demand (bisphenol and phenolic resins) may fall somewhat due to slowdown in coatings and fibrous wood market |

| Methanol | High | Balanced | Balanced | Converting natural gas to gasoline using methanol will keep the market for methanol balanced. Price expected to be stable for the rest of the year. Methanol derivatives like formaldehyde, MTBE (gasoline) and acetic acid are not expected to be affected |

| Caustic Soda | Short | Balanced | Steady to Marginal Increase | Price dropped at the beginning of 2020 due to supply-demand imbalance. A drop in PVC demand will result in a drop in the demand for chlorine which, in turn, will result in a decline in caustic soda production. Price expected to increase in Q2 and stabilize for the rest of the year |

| TiO2 | Balanced | Balanced | Steady | Price has been stable since 2018. In 2020, demand is expected to suffer due to a fall-off in the coating industry following the drop in construction activity |

| Polymers | High | Low | Drop | All polymers (PE, PP and nylon) will be marred by high supply, low demand and price drops due to the auto industry slowdown. This would act as a major opportunity for large-scale buyers from the CPG industry from a plastic packaging standpoint. Auto production accounts for a significant chunk of nylon and PP demand. Ample supply will result in a significant price drop. PE prices saw a small decline and are expected to be stable up to the end of the year due to demand from packaging (food and cleaners). Styrenics will follow styrene. |

| Basic Feedstock — C2/C3/C4 | High | Low | Drop | Ethylene, propylene, and butadiene will be available in plenty. BD is a feedstock for SBR, which is used in tire manufacturing. With an anticipated drop in demand for automobiles, the demand for butadiene from SBR will also be low. Prices dropped in March and are expected to stabilize after Q2 of 2020 |

SOURCE: GEP

*Prices: Forecasted average for 2020 as compared to 2019 average

Market Opportunity — Chemicals

| Category | Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|---|

| Polymers | All Resins | Bulk buy for large volume buyers — take advantage of the present market conditions | Forward buying if the market situation continues to remain favorable | Extend contracts — negotiate rebates on previous fixed-price contracts if any |

| Aromatics and Solvents | All Solvents | Buyers to employ a waitand-watch approach to take advantage of any further price drop since the massive decline witnessed in early April Postpone fixed-price contractual purchases and get into the spot market |

Assess arbitrage opportunity from Asia — prices to remain low in the near term | Extend contracts — negotiate rebates on previous fixed-price contracts if any |

| Inorganics | Caustic Soda | Delay purchase if possible — market price is high due to drop in chlorine demand | Build up inventory before the market tightens due to planned turnarounds | Business as usual |

METALS, PRECIOUS METALS, AGRICULTURAL COMMODITIES

The overall macroeconomic environment, including an economic slowdown, was expected to dampen commodity demand and price outlook in 2020 even before COVID-19. The possibility of weaker-than-expected economic growth, ineffective policy stimulus, resolution of trade tensions, improved supply conditions, and lower energy and fertilizer prices were some of the risks with additional downside potential.

The COVID-19 pandemic magnified these risks, creating a substantial demand slump that has driven down prices of base metals as well as agricultural commodities such as corn and soybeans, given their use in ethanol and biodiesel production respectively. Precious metals such as gold have gained an upside potential considering their status as safe havens under these volatile circumstances.

Metals

- Aluminum

Aluminum prices were originally forecast to decline marginally in 2020 because of lower alumina prices and weak global demand for cars.7 This has now turned into a sharp anticipated decline due to a fall in construction and manufacturing demand. Sustained weakness in the aluminum market may potentially eliminate higher-cost producers.8 - Zinc

Zinc had a bearish outlook for 2020 and has seen the sharpest decline among most base metal commodities in Q1.9 Its use in white household goods and automotive is nose-diving, and even the reduced supply from Peruvian and Indian sources has not been able to sustain prices. Average zinc prices in 2020 are expected to remain below 2019 levels unless large producers cut supplies further. - Lead

Planned outages and the supply impact due to COVID-19 may not completely offset weak demand from the automotive sector, driving prices downward. - Iron Ore

Iron ore held its ground in Q1 of 2020 despite weak demand from China, primarily due to production issues in Australia and Brazil.10 With continued demand impact in Europe and the United States, prices will remain depressed as compared to 2019 levels.

Precious Metals

- Gold

Heightened global uncertainty, robust physical demand and a forecasted easing of monetary policy by the U.S. Federal Reserve were expected to contribute to gold’s upward trend in 2020. COVID-19 has given impetus to these factors. Investors’ affinity toward cash in these uncertain times has strengthened the U.S. dollar, with a potential to limit upside in the near term. - Silver

Silver prices trended upward in 2019 by 3.1%, and were expected to average 4.9% higher in 2020.11 While the trend continued in Q1 2020, mid to late March saw a sharp decline in silver prices due to diminished industrial and physical demand.12 There is current support for prices with recent COVID-19- related mine shutdowns in Mexico, the world’s largest silver producer.

In the near term, weaker physical and industrial demand is likely to be offset by supply chain disruptions.A deteriorating economic outlook and heightened uncertainty will pose an upside risk over the next 6–12 months.

Agricultural Commodities

- Wheat and Rice

Well-supplied markets and 20-year stocks-to-use highs for wheat and rice stabilized pricing for these commodities at the start of 2020.13 With countries going under lockdown starting in March to limit the spread of COVID-19, demand for bread and pasta jumped, and consequently so did wheat prices. There has also been a large spike in retail demand for rice due to significant consumer stockpiling. This, combined with the lockdown measures in major rice exporters such as India, has exacerbated perceived short supply in the market. As the coronavirus impact trends from China suggest, recent buying trends may be short-lived, eventually offset by a supply glut stabilizing prices. - Corn

Corn is expected to experience downward pressure, given that ethanol comprises 39% of corn use in the United States.14 The commodity is currently facing demand and margin pressure due to COVID-19 and the Russia-OPEC oil war. Further price pressure comes from increased acreage for the upcoming corn season.15 Ukraine and Argentina are also increasing their exports now at more competitive prices than the U.S. Barring unfavorable planting weather or a sudden uptick in ethanol demand, corn prices are expected to remain weaker compared to last year. - Soybeans

Coming into 2020, the so-called “Phase 1” deal with China and the related increase in exports were helping stabilize demand and prices for soybeans. However, the COVID-19 pandemic has raised doubts about continued strength for exports to China. This, in addition to a better-than-expected Brazilian crop, the dollar gaining strength against the real, and eroding support for soybean oil, points to high near-term volatility and perhaps some medium-term downward pressure on soybean prices.16

Looking Ahead

As procurement teams manage supply chain issues associated with the pandemic, there are opportunities to capitalize on declining base commodity prices across the globe, which drive a significant portion of direct material costs.

Companies should secure long-term contracts at current prices, which are at record lows; explore financial hedging to lock down futures pricing; and lower the effective commodity cost by averaging out purchases for 3 to 24 months from now. While commodity prices are facing downward pressure, basis pricing (differential between the commodity exchange price and the local commodity price) has seen a severe upside risk due to transportation and storage operational concerns. These must be mitigated by supply chain teams.

Simultaneously, procurement organizations will need to be proactive in securing immediate supply requirements through existing or alternative sources. They also have to manage supply-chain risk by ensuring the financial stability of their suppliers.

Market Opportunity — Metals, Precious Metals, Agricultural Commodities

| Category | Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|---|

| Metals | Aluminum, Zinc, Lead and Iron Ore | Secure long-term contracts at current spot prices Secure alternate supply if existing sources are impacted Negotiate out of minimum contract volume levels for current quarter Extend payment terms to improve working capital |

Secure partial volumes if lower futures pricing is sustained | Extend contracts — negotiate rebates on previous fixed-price contracts if any |

| Precious Metals | Gold and Silver | Secure alternate supply sources to mitigate any operational impact | Mitigate upside price risk potential due to weakened near-term economic outlook | Mitigate upside price risk due to potentially weakened economic outlook |

| Agricultural Commodities | Wheat and Rice | Secure supply to meet immediate demand spike, mitigate basis price impact | Business as usual | Business as usual |

| Corn | Secure long-term contracts at current spot prices, mitigate basis price impact | Monitor any sudden uptick in ethanol demand spiking prices Secure partial volumes if lower futures pricing is sustained |

Business as usual | |

| Soybeans | Secure long-term contracts at current spot prices | Secure partial volumes if lower futures pricing is sustained | Business as usual |

PACKAGING

Before the outbreak of COVID-19, we were closely following the Duke CFO Global Business Outlook survey results to gauge the sense among finance leaders of the likelihood of a significant slowdown or a recession. In the September 2019 survey, 67% of U.S. CFOs predicted a recession by the end of 2020 with even higher pessimism observed globally.17 We now see signs of recession in several global economies, but these are unlike past recessions which resulted from weak economic fundamentals or crisis-hit financial institutions. The current situation was precipitated by government-imposed lockdowns and a sudden stop in most economic activities due to the coronavirus.

During a recession, as sales fall (especially in retail and F&B sectors — the key drivers of packaging), demand volumes of consumer-facing and secondary packaging will shrink. In the near-term, COVID-19 will add more complications, as buyer and seller facilities are forced to shut down or reduce activity, implement additional sanitation protocols and face other interruptions to normal operations. Volumes are also shifting and evolving — distilleries are making hand sanitizers, and auto manufacturers are producing ventilators.

In the immediate term, procurement teams need to proactively review pricing structures and supplier equipment footprints to ensure these reductions and changes meet the shifting requirements of their volumes and item mix.

Knowing what packaging formats will be prevalent in the post-COVID-19 world is likely impossible at this stage. But CPOs need to stay engaged with their sales and planning teams to know changes in consumer preferences or to adapt to a changing environment. Identification of secondary sources is always critical, but needs an extra emphasis during this uncertain period.

Near- and Mid-Term Impact

It is a natural response in many organizations to cut back on costs during challenging times. However, a Harvard Business Review study has concluded that organizations focused entirely on cost reduction did not emerge stronger from a recession. In fact, they faced the highest chance of failure.18 Instead, the study indicates that strategic cost reduction works best when coupled with smart investments to defend market share during a recession while positioning for growth once the dark clouds pass.19

In the immediate term, we are seeing clients with buy-side leverage pursuing contract renewals through this period, as suppliers shore up their books of business and revenue streams. We encourage procurement teams to take advantage of this opportunity to negotiate favorable extensions as well as secure “favored customer” status for supply allocation to weather the storm.

The stay-in-place orders are driving a massive shift toward e-commerce and home delivery, which needs to be factored in — both for design (“Ships in Own Container,” or SIOC) and volume requirements, and for the availability of certain types of packaging such as corrugated boxes, foam and paper takeout containers.

Packaging types with inherently longer lead times, such as bottles and pouches, may not be as impacted unless the suppliers are subject to shutdown orders. In that case, responding with agility to production orders as well as applying buy-side leverage to maintain priority in the production queue will be critical to get through the shortterm disruptions.

Long-Term Impact

Further in the future, adaptive strategies for primary packaging (rigid and flexible containers, fiber boxes and cartons) include convening a cross-functional team to execute a redesign with new molds and labels, or exploring optimized equipment, such as corrugate-on-demand technologies, to drive agility.

For secondary packaging (corrugated, cold-chain packaging, protective packaging (foam/fiber), labels and sleeves), a full portfolio review of specifications to ensure design-to-value is critical. Secondary packaging is often designed once. Then the attention shifts elsewhere. So specifications may be over-engineered, or spend may be amassed with a maximum-performance specification, which is excessive for most products being shipped.

In both packaging categories, agile manufacturing, such as additive manufacturing (3D printing) or in-house box-making, seems poised to break out as it finds new acceptance. 3D printing and small-scale manufacturing are proving to be of significant value in COVID-19 treatment, as in a recent news story about using 3D-printed parts to keep ventilators running in Italy.20 Certain legacy players such as WestRock appear to have already invested in this vision, with its acquisition of Plymouth Packaging (“Box on Demand”) in 2017.21 Procurement leaders will need to work diligently to “sell” this vision across their own organizations as well as negotiate hard with supplier partners to buy into a long-term growth strategy that may require some short-term revenue loss.

Looking Ahead

Uncertainty is the only certainty for the near future, but with uncertainty comes the opportunity to re-evaluate the buyer-seller dynamic, strengthen partnerships and, ultimately, secure favorable commercial and supply terms. These short-term wins will endow procurement leaders with the trust and the momentum to drive designedfor- value designs, new technology adoption, and strategic spend management to protect and grow consumer share in the long term.

Market Opportunity — Packaging

| Category | Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|---|

| Secondary Packaging | Corrugated Shippers | Extreme demand volatility; some supply-side shock depending on geography | Expect volatility to continue | Eventual return to normal operations |

| Cold-Chain Packaging | Major impacts to supply due to critical pharma demand | Expect volatility to continue | Eventual return to normal operations | |

| Protective Packaging (Foam, Fiber) | Supply shock is expected in the market. Extend contracts if possible | Business as usual | Business as usual | |

| Labels and Sleeves | Extreme demand volatility; some supplyside shock depending on geography | Expect volatility to continue | Business as usual | |

| Primary Packaging | Rigid Resin Containers | Global oil price crash adding to overall volatility; lock in low price if not sacrificing supply availability | Continuing volatility in oil markets globally | Continuing volatility in oil markets globally |

| Flexible Resin Containers | ||||

| Fiber Boxes and Cartons | Extreme demand volatility; some supplyside shock depending on geography | Adapt to new world — e.g. increased food carryout | Business as usual | |

| Protective/ Miscellaneous Packaging | Pallets | Supply shock is expected in the market. Extend contracts if possible | Monitor hardwood availability and evaluate pallet strategy (used vs. new, wood vs. plastic) | Business as usual |

| Wraps, Straps, Tape | Business as usual | Business as usual |

INDIRECT CATEGORIES

CAPEX

Global corporate CapEx growth in 2019 was below expectations, up only 3.5% from 2018.22 North America, which accounts for close to 30% of global CapEx, saw a loss of momentum in 2019, with a tepid 2% year-onyear (YoY) increase.23 The slump was primarily because of the U.S.-China trade war and concerns over access to liquidity in times of crisis.

In 2020, due to the pandemic, we expect a sharp jump in capacity expansions within health care, food and beverage (F&B) and communications (digital entertainment and telecom), a result of greatly increased demand, government policies and supply chain disruptions. However, corporate CapEx in automotive, energy, industrial goods and construction could be dismal. In the short term, we expect the triple effect of coronavirus disruptions, oil prices and volatility to result in further drops in investor sentiments and delay in key engineering projects due to travel and supply constraints.

Thus, corporate CapEx, which we had earlier expected to decline by ~1% in 2020, is now expected to contract at a much higher rate in North America.24 Further, we are extremely cautious about relations between the U.S. and China, as an escalation could impact tariffs and supply of metals and other construction materials to the U.S.

Construction: Equipment, Materials and Services

Prior to the coronavirus crisis, in February, construction spending dipped 1.3% as both residential (-0.6%) and nonresidential (-1.8%) activity slipped.25 While many projects continue to proceed, hard-hit areas are shutting down construction sites and project delays/cancellations are mounting. Whether or not projects can continue depends on whether state or local authorities categorize construction as an essential business. Expect delays in supply of materials as nearly 30% of all U.S. building product imports come from China.26 Drywalls, glass, steel, lighting fixtures, flooring and curtainwall are some of the most affected items.

The construction industry has been persistently constrained by a shortfall of skilled labor, which will be exacerbated by quarantine requirements and the longer-term decline in labor mobility. At the same time, 39% of contractors have reported that nongovernment project owners had halted or canceled their construction projects.27

We expect the industry to be partially impacted by the pandemic. The heavy financial toll on almost all large corporations will affect order booking for the rest of this year and 2021, so we may see some of the smaller construction services and equipment manufacturing firms declare bankruptcy. The prices of construction materials and equipment will remain in check, but labor rates are expected to rise if uncertainty prevails.

Our recommendation is to continue with active RFx activities, laying greater emphasis on the suppliers’ financial performance. For ongoing projects, we suggest working closely with contractors to track inventory accurately, document project progress, identify alternative materials to absorb supply shock, and reschedule downstream equipment based on a realistic project plan so as to lower rental costs.

In the long term, investing in digitalization will enable the use of cloud-based building information modeling (BIM) and intelligent asset management. There will also be an increased adoption of robotics and digital twins (virtual models of physical products or processes) in the future.

Engineering and Technical Consulting Services

North America accounts for almost half of engineering services revenue globally. However, travel restrictions and site closures have impacted this category, precluding site visits for surveys or taking measurements. However, due to the availability of cloud-share technologies and robust document-control tools, consultants and project managers can manage their ongoing projects and conduct regular checkpoint conversations with clients and peers. Early reports suggest that there will be at least a 19% decline in the market size for this category against 2019, as clients will defer key engineering projects.28 We expect a talent reshuffle in the short term, as contract engineers will either be laid off or make shifts voluntarily. This can be a good opportunity to renegotiate rate cards with existing service providers.

Material Handling Equipment

We expect a demand surge in material handling equipment (MHE) in 2020 within North America. E-tailers have been ramping up their warehousing capacity as Americans have turned to online buying because of movement restrictions. For the short term, there could be a rise in demand of gas-operated forklifts, backed by lower oil prices and lower purchase costs. In order to improve throughput, many CPG and pharmaceutical companies may also invest in fully automated conveyor and sorting systems. This will compensate for lost revenue for MHE suppliers from the struggling automotive and auto ancillaries sector.

We do not soon foresee major disruption in the supply of equipment or spares, as the government is keen to increase the capacity for essential goods, including therapeutic drugs, PPEs, medical kits, health care instruments, lab equipment and canned foods. In the long run, we see a higher adoption rate of automated guided vehicles (AGVs), industrial robots and automated storage and retrieval systems (AS/RS) across manufacturing facilities in North America, to minimize the impact on production due to lack of labor mobility.

Packaging Equipment

The recent buzzwords here have been sustainability and sustainable materials, as companies have been shifting from single-use plastic materials to reusable, recyclable or compostable alternatives. The pandemic and subsequent economic decline will lead to a slowdown of these green initiatives, including investments in packaging development and subsequently in equipment investments. For the time being, plastics will become reestablished as the material of choice.

We expect a rise in the use of rotary palletizers and blister packaging, both of which were reputed for higher TCO savings, in the pharma and CPG industries. However, as sourcing packaging equipment is critical to supply chain operations, we recommend pre-evaluating alternative vendors who can supply the technology of choice, and avoid single sourcing. Where single sourcing has been the preferred option, we strongly recommend investigating further tiers of the supply chain to prevent unpleasant surprises in the future.

Processing Equipment

In addition to the ongoing oil price war between Russia and Saudi Arabia, it is expected that uncertainty and lower demand in road transport and aviation will significantly decrease investments in the oil and gas industry. Many refineries will take a good deal of time to increase their CapEx, and the demand for processing equipment will remain low.

We recommend that companies upgrade processing equipment such as air dryers and tablet presses to benefit from lower project and equipment costs. In the long term, considering the uncertain relations between the U.S. and China, many pharma companies could near-shore API manufacturing. This could significantly boost demand for production equipment locally. The F&B sector can also look to invest in non-contact, low-cost quality testing machines, which will ensure higher quality and reduce packaging time.

HVAC Systems

The supplier sentiment in this segment is positive, and most manufacturers have enough inventory to meet distributors’ short-term demand. Beyond this, there could be concerns; China, France and Italy are sources of highly engineered HVAC (heating, ventilation and air conditioning) systems, and as of now U.S. manufacturers may not have a complete mitigation plan ready. The silver lining is that Chinese factories have started resuming operations in Q2, which coincides with the season of peak demand in North America. We suggest that our clients continue with their current sourcing plans for this category.

Looking Ahead

Going forward, contractual terms will be renewed and emphasis on employee safety could change the usual business practices. Procurement leaders will have to think beyond tariffs and labor rates, and focus on supply chain optimization. Category managers will have to shift from a reactive to a proactive procurement process by integrating with business stakeholders and contractors ahead of time. Suppliers and contractors that have embraced digital technology and practice sustainable corporate policies should be preferred over savings. CxOs should not redesign their long-term supply chain strategies based on the pandemic, as the crisis is not yet over. However, they must invest this time in evaluating smart CapEx options and remain flexible with their nearterm supply chain policies to avoid failure.

Market Opportunity — CapEx

| Category | Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|---|

| Construction | Equipment | No impact | No impact | No impact |

| Material & Services | High impact; price drop in indexed commodities | Price drop continues | Prices remain stable until market corrects itself | |

| Engineering & Technical Consulting | Increased demand for offshoring; prices remain stable | Plateau may continue for 3–6 months | Higher and newer offerings at lower prices | |

| Material Handling Equipment (Forklift) | Anticipated hike in forklift demand leading to price increase | Prices continue to rise | Continue to monitor; look to deploy fully autonomous capabilities as possible | |

| Packaging Equipment | Higher demand and delayed delivery | The trend continues with possible bankruptcy for smaller suppliers | Business as usual with M&As | |

| Processing Equipment | Payment terms requested by suppliers may shorten | Monitor suppliers’ financial risk | ||

| HVAC Equipment | Lower demand with significant hit on larger suppliers | Low demand continues | Demand market may start growing after 12–18 months |

ENERGY AND UTILITIES

The global utilities market has seen major shifts in the first quarter of the year. Both the supply and demand sides have experienced significant shocks, altering the landscape completely compared to the close of 2019. Demand has plunged as countries implement lockdowns and practice social distancing to limit the spread of COVID-19. Compounding this shift is the drop in crude oil prices to historic lows as supplier nations flood the market and wage a price war. The outlook for the rest of 2020 looks extremely unpredictable as a result of these two major disruptions.

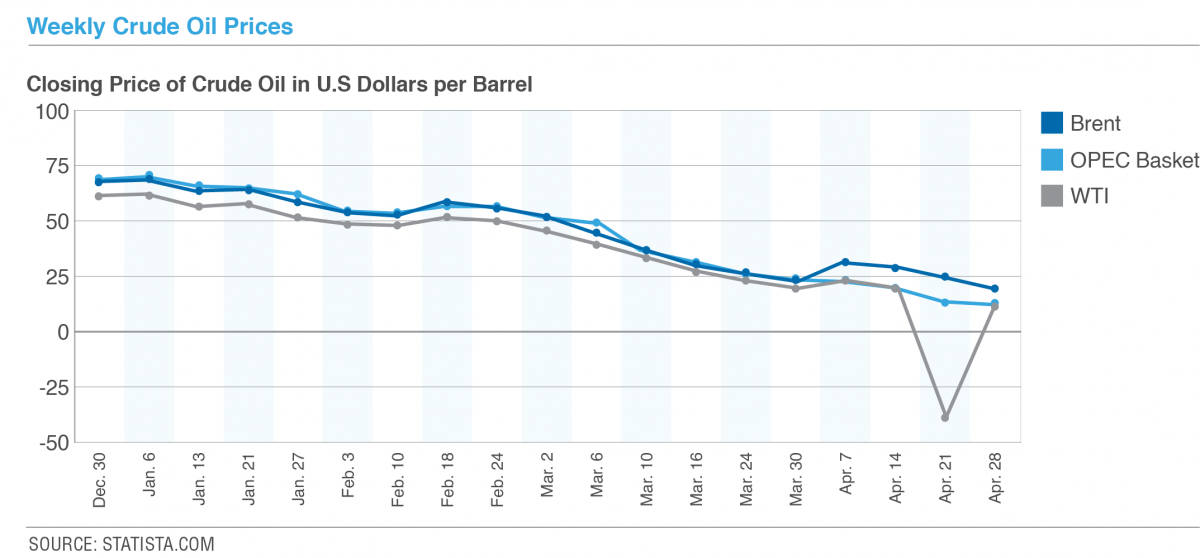

Crashing Oil Prices

In early March, a production cut agreement between OPEC and Russia fell apart, leading to the abandonment of production quotas. As a result, the crude market has been flooded with excess supply as both Russia and Saudi Arabia wage a price war. Further complicating the situation, Saudi Arabia and UAE have announced plans to increase production. Crude oil prices continue to be volatile with a downward average trajectory since the beginning of 2020. Price points since April 7, 2020 (USD/Barrel) are as follows:

| April 7 | April 14 | April 20 | April 28 | |

|---|---|---|---|---|

| OPEC | $22.67 | $19.70 | $14.19 | $12.41 |

| Brent Oil | $31.87 | $29.60 | $25.57 | $20.46 |

| WTI Oil | $23.63 | $20.13 | -$37.63 | $14.22 |

SOURCE: STATISTA.COM

Disruptions in both supply and demand caused oil futures to fall by approximately 40% in March.29 However, with the recent OPEC+ production cut deal, major oil producers will begin to reduce production, aimed at an aggregate decrease of 9.7MM BPD.30 Considering the reduced demand — standing at approximately 30MM BPD — the market disequilibrium still exists and recovery will be slow as we head into the second half of the year.31 The rate of recovery will largely depend on nations’ ability to return their economies to a working state. Until the global economy reaches this state, crude oil prices are expected to be volatile.

Falling Electricity Demand

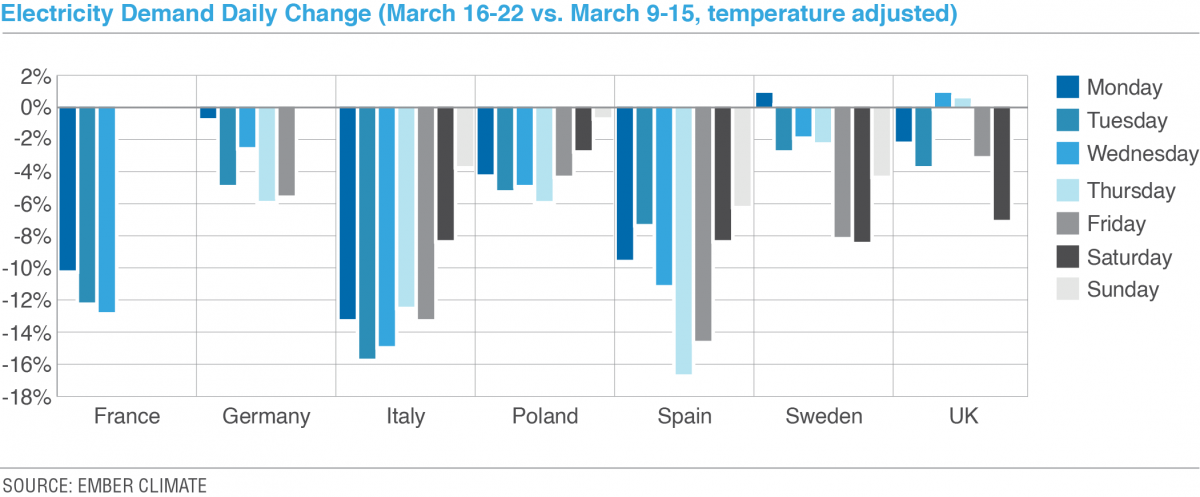

- Europe

Despite the winter season and increased household consumption, demand in the overall European utilities markets is falling continuously due to social distancing, lockdowns and closure of nonessential businesses. Lower demand in commercial and industrial sectors has outweighed the increase in residential consumption. There were also unprecedented highs in solar and wind energy supply compared to Q1 in 2019 — an increase from 67 BN kWh to 77 BN kWh.32 This has resulted in half of the nations’ domestic consumption coming from renewable sources.- Italy

Europe’s first and worst-hit case provides insights into what we can expect in other affected countries, such as Germany, Spain, France and Switzerland, among others, where the impact is rapidly escalating. According to the Electric Power Research Institute (EPRI), Italy saw peak demand in electricity drop by ~20% seven days after the country locked down.33 - Germany

Following the trend set by Italy, most European nations have seen demand for power drop significantly. Germany’s demand fell approximately 6%, and is expected to drop further.34 Industries make up 44% of Germany’s electricity consumption, the highest in Europe, which will likely be hit dramatically.35

- Italy

- United States

New York City, the epicenter of the outbreak in the continent, has seen a significant drop in power consumption. During the work week of March 23, there was a 12% drop in the average hourly electricity load in the city’s five boroughs compared to the same period in 2019.36 This impact is largely due to the closure of commercial businesses as stay-at-home orders are being enforced and general economic activity has slowed down. Other major regions in the U.S. have also recorded drops in demand, though at lower ranges, as the impact of the outbreak has not yet been fully realized and regulations were not implemented until later. - China

The first country impacted by the outbreak may provide a more accurate medium- to longer-term forecast. Reporting fewer locally transmitted cases daily, Wuhan’s two-month lockdown has now been eased. In the month of February, when the outbreak was at its peak, the nation saw a 16% decrease in demand.37 Hubei, the province where the pandemic began, saw a 30% decrease in electricity demand year over year.38

Clean Energy

Due to surplus supply, electricity prices have been falling across Europe, which means the revenues of all energy generators are likely to take a hit in 2020. This has already triggered a domino effect as it has started delaying utilities’ purchasing agreements, which can cause risks and disruptions in development of renewables projects. Sliding power rates do not allow for new investments, creating a grim outlook for the short- to mediumterm future of the renewables market. The long-term impact, however, remains unchanged as corporations and nations retain their ambitious targets to utilize renewable energy sources.

Looking Ahead

There is major disequilibrium in the market from excess supply and plummeting demand. In this volatile environment, demand and future prices will hinge on the scope and duration of lockdowns; shifting oil prices; and global economic conditions after lockdowns are lifted. The benchmarks from “normal” times will not be of much use here, so constant monitoring will be necessary to fully assess the situation.

We recommend companies leverage market conditions and utilize live pricing through competitive bidding of suppliers in deregulated markets for electricity. Supplier responses will indicate the most accurate market conditions, as conventional benchmarks will not be applicable.

Market Opportunity — Energy and Utilities

| Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|

| Electricity | Live pricing through competitive bidding in deregulated markets | Monitor | Monitor |

TRAVEL

The pandemic has had a profound impact on the business travel industry’s bottom line. Business travel has ground to almost a complete halt globally, as companies have canceled or suspended almost all business travel, regardless of country or region. Companies are also modifying travel and traveler safety policies, including instituting new policies pertaining to travel approval.

The World Travel and Tourism Council has stated that the pandemic could lead to a loss of 50 million jobs around the world.39 The industry will most probably take the rest of 2020 and beyond to recover, assuming travel restrictions start to be lifted by June. There has been a resurgence in China, with domestic travel almost back to normal, which provides some hope to businesses in other regions.

Potential 2020 Business Travel Spend Revenue Loss Due to Coronavirus*

| Potential 2020 Monthly Revenue Loss ($ Billions) | % Companies Cancelling/ Suspending All or Most Trips to Region/Country | |

|---|---|---|

| China | ($35.1) | 99% |

| Hong Kong | ($0.32) | 99% |

| Taiwan | ($0.34) | 98% |

| Asia Pacific (minus China, Hong Kong and Taiwan) | ($19.3) | 97% |

| Europe | ($31.0) | 96% |

| United States | ($23.1) | 85% |

| Canada | ($2.0) | 89% |

| Latin America | ($4.5) | 92% |

| Latin America | ($4.5) | 92% |

| Middle East/Africa | ($3.7) | 95% |

| Total Potential Monthly Revenue Loss | ($119.4) |

SOURCE: GBTA BTI™ OUTLOOK ANNUAL GLOBAL REPORT & FORECAST40

*Methodology: GBTA (Global Business Travel Association) conducted a worldwide poll of 1,155 members from March 18-21, 2020.

Airlines

The airline industry is experiencing a deep, immediate demand shock greater than the impact of 9/11 or the 2008 financial crisis. Government restrictions on travel and mandatory quarantines have absolutely decimated flight capacity. As of late April, airports were indicating that more than 160 airlines operating 10 weeks prior had no service scheduled, and an additional 91 — including Lufthansa, KLM, Qantas and Iberia — were operating at less than 10 percent of their normal capacity levels.41

U.S. airline executives are discussing the possibility of submitting a proposal to the U.S. Department of Transportation (DOT) that would allow them to consolidate services on routes during the crisis so that passengers with tickets across various carriers could all fly on a single flight. In addition to reducing capacity, low oil price expectations for the short term have been keeping operating costs low.42

Most airlines are spending more money reimbursing fliers than receiving new booking revenues. The U.S. DOT has issued an enforcement notice to airlines ordering them to provide refunds and not vouchers for future travel for flights that have been canceled or have required a significant schedule change. The IATA has estimated that the airlines’ liability for refunds globally is around $35 billion.43 Some countries — including Brazil, Colombia, the Netherlands and Canada — have eased regulations so that airlines can give passengers vouchers in place of refunds.44

Singapore, Australia, China, New Zealand and Norway have introduced financial or regulatory aid packages of either grants, loans or tax relief to supplement cash flow and ensure that there is no liquidity crisis. However, demand may not soon recover to earlier levels, as consumer confidence may be shaken and employers adjust work-from-home policies to support greater reliance on remote technologies. Considering these conditions, airlines are now hesitant to enter into long-term contracts or provide higher discounts to clients without assurances/commitments from clients about future demand. In the case of contracts that are near expiration, airlines are offering short-term extensions to allow time for a post-pandemic strategy assessment.

Rental Cars

Car rental providers have reported a sharp drop in bookings for the months ahead, especially at airports, which are the main business of operators such as Hertz and Avis Budget. Within the U.S., domestic car rental deman has dropped between 50% and 80% month over month from February into March 2020.45 Despite the reduction in demand, many car rental branch locations continue to operate, though some are closed.

Car rental companies are looking to cut costs by downsizing both vehicles and staff to match demand. Companies are offering home delivery services and no-fee cancellation policies on pre-paid rentals — incentives to young travelers and students who must unexpectedly return home. Companies such as Hertz have also been providing free rental vehicles in New York City to health care workers.

Ride-share companies have also registered a sharp decline in bookings, especially in cities badly affected by the coronavirus outbreak. Most companies have suspended their carpooling services in major markets. When demand began to fall, companies pivoted and began striking partnerships with local businesses to help fulfill delivery needs ranging from takeout meals to supplies and groceries. For example, Lyft announced that it was piloting meal delivery services in the San Francisco Bay Area in partnership with government agencies and local nonprofits, and also suggested its drivers could find work at Amazon, which continues to hire distribution workers for its Prime delivery service.

Hotels

Since the coronavirus outbreak began escalating in the U.S. in mid-February, hotels have lost more than $5 billion in room revenue.46 This figure is rapidly accelerating, with hotels currently on pace to lose more than $500 million in room revenue per day based on current and future reported occupancy rates.47 This means a loss of $3.5 billion every week — and the figures are expected to escalate further as the situation worsens.48 Overall, the hotel industry is expecting a 60–65% decline in revenue for Q1.49 And most hoteliers are already reporting projected revenue losses of 80% for the second quarter of 2020.50

Based on current occupancy estimates for the immediate future and historical employment impact rates, nearly 3.9 million total jobs have either been eliminated or will be eliminated in the coming weeks.51 With 70% of direct hotel employees laid off or furloughed, hotel workers are losing more than $2.4 billion in earnings each week.52 Individual hotels and major operators are projecting occupancies below 20% for the upcoming months.53 At a sustained occupancy rate of 35% or lower, hotels may simply close their doors, putting 33,000 small businesses at immediate risk in the U.S.54

Hotels have been offering better cancellation terms in the hope of trying to retain/delay refunds for reservations made for June and July. For example, Marriott is offering an updated new and existing reservation cancellation policy that allows guests to get full refunds for any trips planned until June 30 even if prepaid, if they are canceled or changed up to 24 hours prior to the reservation date. However, the refund will be processed with a delay of up to 90 days.55

Hotel chains such as Hilton, IHG and Marriott have made public announcements related to substantial pay cuts for executives and some pay cuts for non-furloughed employees. Hotels are also looking to eliminate nonessential and discretionary expenses, including marketing and capital investments, to manage costs during this crisis. Leased properties may face a greater cash flow risk and are either searching for corporate-backed options or negotiating with lenders to survive this period. Chains are deferring brand standards to allow local properties to avoid the investments needed to remain a part of the chain.

At present, hotels are continuing to accept reservations planned well in advance of stay. Most have not reduced rates drastically to attract travelers as offering deeper discounts or reduced pricing will only extend the recovery period for the industry.

Looking Ahead

For companies trying to negotiate better discounts/pricing with airlines, hotels or car rentals and fleet providers, negotiations may not yield any better-than-usual results as the entire industry is in survival mode. Offering deeper discounts or reduced pricing will only delay the recovery process, leading to longer-term impact on supply. Once travel demand bounces back, depending on the extent and duration of this restrictive period, there may be a general increase in pricing if supply remains constricted due to business closures, due to the demandsupply gap.

The current cash-strapped, no-guaranteed-revenue situation puts hotels under significant strain for any corporate negotiations. We see hotels being hesitant about making new long-term commitments with companies at least for the next few months. Room rates are typically negotiated on an annual basis and follow the calendar year cycle. However, we expect hotels to hold their pricing commitments for the remainder of the year.

Market Opportunity — Travel

| Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|

| Airlines | Limited negotiation opportunity as industry is in revenue crunch Extend current contracts if expiring Build plans for leveraging previously accrued “Travel Credits” and ensure no credit loss or expiry |

Continue to monitor industry trends to reassess longer-term sourcing strategy and travel category targets (revenue vs. market share goals) Ensure extension of corporate status and soft benefits programs for travelers |

Potentially revisit travel policies and guidelines to retain cost benefits from new ways of working (virtual collaboration) and opportunities to decrease travel spend |

| Rental Cars | Limited negotiation opportunity as industry is in revenue crunch Extend current contracts if expiring |

Monitor and revisit sourcing strategy | Business as usual |

| Hotels | Limited negotiations opportunity as industry is in revenue crunch Extend current contracts if expiring |

Leverage hotel marketing offers to ensure soft benefits are extended to travelers Continue extending current contracts as negotiations may not lead to desired outcomes |

Sourcing strategy needs to be revisited; many local properties may be out of business leading to changes in traveler preferences |

FLEET

The pandemic has affected many areas in this sector, including the wide range of industry partners, such as fleet management companies (FMCs), original equipment manufacturers (OEMs), dealerships, transportation and logistics, service providers, and others. It has greatly impacted the suppliers’ ability to source, lease and manage vehicles across different markets. The total fleet sales, including commercial, government and rental sales, measured across nine different manufacturers, dropped by more than 30% in March, representing an 11.4% drop year-over-year.56

The U.S. DOT’s National Highway Traffic Safety Administration (NHTSA) and the U.S. Environmental Protection Agency (EPA) have lowered the corporate average fuel economy targets and CO2 emissions standards through model year 2026 to 1.5% improvement year-over-year from the previous target of 5%.57 As the risk to revenues grows, businesses are increasing their focus on means to access funds, loan forgiveness details, understanding federal guidance, and the status of future funding legislation.

OEMs

The impact on the auto industry is being felt beyond China’s borders, as shortages of supplies from China and lockdowns have stalled production around the world. To illustrate:

- The largest automakers in the U.S. — General Motors, Ford Motor and Fiat Chrysler — closed plants after the United Auto Workers union pressured them to do so to protect their workers. Ford has partnered with 3M and GE Healthcare to shift production toward making medical equipment and supplies

- Hyundai and Kia recently stopped several assembly lines in Korea, while Nissan announced it would suspend its auto production in Japan

- Jaguar Land Rover, BMW, Toyota, Honda, Nissan and Vauxhall have all stopped production at their assembly plants in the U.K. until the end of April. The number of cars built in the U.K. is predicted to drop by 200,000 units this year because of factory closures as well as the fall in demand58

Over an eight-week period, the stocks of General Motors, Ford Motor and Fiat Chrysler plummeted by over 60%, and the entire Auto Manufacturers index has lost up to 20% of its total market capitalization, or $56 billion in a single month.59

Commercial fleet sales from nine manufacturers totaled 65,135 in March 2020, representing a 17.7% year-over-year decrease.60

FMCs and Lessors

Fleet management companies (FMCs) are working closely with their partners to ensure business continuity and to minimize the impact on clients. However, as several OEMs have halted production in North America and Europe, the FMCs’ ability to procure vehicles is affected; vehicle deliveries are already delayed.

As a result of the uncertain economic environment, the cost of sourcing funds on the bond market has increased threefold in recent weeks. The increase in spreads in the corporate bond market has a direct impact on the cost of funds and makes it difficult to price proposals effectively.

Initial calculations and suppliers’ proposal data show an uptick of up to 6% on lease costs.61

FMCs are considered essential business in many cases; they provide support to companies deemed essential services such as grocery stores, law enforcement, and hospital supplies. As a result, FMCs are operational and supporting clients for the time being.

Looking Ahead

FMCs have started recommending to clients that current contracts that are set to expire in the next few months be extended to ensure the continued mobility of drivers.

The current uncertainty has resulted in suppliers shortening the tenure of their proposal pricing validity (to a maximum of two weeks) and recommending that ongoing RFPs be halted due to extreme volatility. This, combined with production shortages, can lead to increased car costs in the near term, after the crisis passes.

Clients with urgent requirements will need to review alternatives such as out-of-stock cars and rentals, which will drive their costs up.

Possible discounts on extensions may be provided locally and free early termination is a possibility for extended contracts. Although only a few FMCs may be facing financial difficulties as of now, many firms will need to take decisions regarding the extension of contracts during the lockdown, or they will face increased costs from excess mileage charges.

Market Opportunity — Fleet

| Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|

| Fleet | Extend current contracts Evaluate alternatives and mitigate potential delay in vehicle delivery |

Expect tighter market conditions as vehicle availability may still be impacted Continue extending current contracts/leases as delays of new vehicle orders are expected |

Business as usual with continued industry favorability for leasing vs. owned fleet Restart negotiations |

GENERAL AND PROFESSIONAL SERVICES

The COVID-19 pandemic has profoundly impacted the General and Professional Services (GPS) supply chain and presents a unique juxtaposition of short-term priorities and longer-term opportunities for GPS sourcing professionals. The fast pace of developments requires proactive problem-solving, opportunistic strategies, and close and continuous business partnering.

Critical short-term goals in GPS purchasing include maintaining supply continuity, managing operating cash flow needs, and capitalizing on emerging sourcing opportunities. For many clients, addressing supply continuity issues is the highest priority.

The pandemic has created short-term operating cash flow challenges and therefore a need for quick savings to make an impact on the P&L. Strategies that can be considered are: developing budget freezes with spend to date and criticality factors; conducting current project/budget ROI reviews; finding alternatives for ongoing purchase needs; and instituting ongoing spend approval processes. Areas under GPS to consider for short-term P&L impact strategies include meetings and events, recruiting, consulting, and learning and development.

GPS purchasing professionals should also capitalize on opportunities to adjust supply strategies in some categories. For example, they should take advantage of a greater appetite for performance-based compensation deals in professional services, and should try leveraging deals with airlines and hotels given the supply-demand shifts.

We examine key areas in GPS that the COVID-19 crisis will impact significantly:

Consulting and Professional Services

The consulting market in North America is expected to witness a slump of 17-19% in revenue for 2020.62 The highest declines in demand will come from clients in the health care, energy, travel and hospitality, and manufacturing sectors — all facing a significant slowdown because of the business impact of the pandemic. However, we believe this drop in demand is likely to be short-term, as many major firms will shift their resources to industries with higher demand as businesses recover. For procurement teams that have immediate or midrange active projects, this presents an opportunity to leverage the demand crunch in tactical negotiations, primarily in strategy, finance and technology consulting engagements that continue to see a business need in the market.

Due to the decline in demand, many companies are slowing their hiring pace for 2020 by rescinding or delaying job offers, deferring promotions, cancelling summer internships, and implementing pay cuts for senior executives.63 For example, PwC has announced a pay cut of 25% for partners and put hiring on hold.64

Several risks will emerge that purchasing professionals must manage in the aftermath of the pandemic. Firms will reposition their internal resources from low-growth to high-growth opportunities, thereby mitigating business disruption. We will also see higher rates of attrition in many firms through 2020. Purchasing personnel should monitor consultancies closely to ensure they are allocating appropriate quality resources to engagements in light of such staffing dynamics. Furthermore, small- to mid-size consultancies may face severe business disruption and should be monitored for business continuity and sustainability. We expect some business closings and, in the longer term, greater M&A activity among the more stable firms.

Once the world begins to get back to business, there are several impacts on consultancies that we anticipate:

- First, for clients, we believe there will be a short-term price adjustment as firms seek to gain market share at reduced margins, including a greater appetite for risk-based compensation. Companies that have business needs and are in a position to move on negotiations quickly can benefit from these short-term opportunities

- Second, branded firms are likely to fare better than smaller firms because of tenured projects, greater remote technology investment, and more stable cash flow. M&A activity will increase as they look to acquire smaller, less successful firms

- Third, as we move into summer, several service areas will see an increase in activities and new client projects, including finance, private equity and M&A firms, as well as IT and supply chain, as companies move to secure their balance sheets while minimizing the risks they may have been exposed to during the crisis. These developments will likely drive pricing upward beginning in Q3

Contingent/Temporary Labor

Unemployment in the United States was at an all-time low in the beginning of 2020, but is now expected to reach double digits as job losses accelerate, with over 10 million people filing for unemployment benefits in March 2020.65 Labor force participation also showed a decline as many workers are choosing to stay at home amid various state-mandated lockdowns. This, in turn, has led to a short-term increase in labor cost, as it has driven companies like Walmart and Amazon to pay bonuses and higher wages to attract laborers. These substantial macro changes to the labor market present purchasers of contingent labor with a mix of risks, required mitigations and opportunities.

Supply continuity of contingent labor is a major risk for businesses in the short term. Organizations that rely on contingent labor for production must move fast to meet the new operating challenges. The pandemic is forcing businesses to rethink how work gets done. In the immediate term, labor supply continuity risks are being managed by leveraging preferred partners for joint mitigation planning; by finding channels for staffing through referral networks; and by applying focused recruitment process outsourcing (RPO) solutions.

In the medium to longer term, we expect that companies will strengthen their preferred partnerships to reduce risk, and will develop and employ alternative solutions such as online staffing portals. We also expect an increased focus on automation for a wide range of business activities and functions. The use of technology and automation will be paired with greater application of lean operating principles in order to drive down corporate reliance on contingent labor.

While some companies are facing supply continuity challenges, others are reducing labor operating costs in the short term by cutting or furloughing significant percentages of their workforce. So, while certain industries (travel and hotels, for example) are cutting contractors, other industries such as finance, FMCG, online retail, and health care/pharma are hiring to deal with the surge in demand.

In the next three to six months, contingent labor sourcing professionals should work to recalibrate labor supply relationships and sourcing strategies to meet the new market dynamics. Temporary labor firms will have a long road to recovery, with urgent need for revenues and cash flow. This, paired with greater availability of labor, will give purchasers an opportunity to negotiate competitive deals and strengthen preferred supply agreements.

During this period, purchasing personnel should work closely with their human resources and business stakeholders to plan for and begin re-engineering aspects of labor usage and the supply system. This can include elements of preferred temporary labor partnering, alternative labor supply channels, adjusted operating principles and organization structures, insource/sourcing, use of derivatives of RPO, and other solutions. Procurement and business stakeholders can drive change by applying new solutions in 2020 to a new world recovering from the impacts of the pandemic.

Recruitment

The pandemic has substantially disrupted corporate recruiting activity, including the use of RPOs and other talent acquisition service providers. Nearly every aspect of business hiring, from interviewing to onboarding, has changed drastically and will continue to do so. In cases where there is still hiring, companies are looking for candidates locally and through unique and alternative channels.66

Corporate recruiting and associated purchasing will see a significant influence of the COVID-19 crisis in the medium and long term. The use of automation technology for talent acquisition processes will advance more rapidly, as will changes to fundamental ways of working with a greater reliance on remote working solutions, lean staffing and the development of risk-proof solutions such as scalable process outsourcing. Face-to-face interviews will be increasingly replaced with video interviews through online platforms. These shifts must be accounted for in future sourcing strategies and will require the development of new processes, supply sources and technology applications.

The fundamental shifts in remote working, organizational “right-sizing,” and use of supplier managed services will drive short- and longer-term requirements for sourcing professionals. Having a talent intelligence and process management technology platform that can provide end-to-end visibility and personalization will become highly critical to support effective adoption of the recruiting model. Purchasing teams will need to focus on remote work software, virtual reality tools and remote meeting software when working with business stakeholders.

Underlying the development of new recruiting strategies will be a significant move toward organizational “rightsizing” and process efficiency. Past studies have indicated that more than 40% of companies prefer that their employees not work from home due to productivity concerns.67 After the pandemic, we will find that remotely conducted, risk-controlled business activity is a new normal for many companies. Sourcing professionals can contribute to finding new suppliers and solutions as well as helping eliminate costs for office space, overheads, and insurance/indemnity coverages, among others. Furthermore, the shift to remote working will offer employers some flexibility in controlling total employment costs just as flexible work arrangements offer meaningful value to many workers. According to Global Workplace Analytics, 37% of remote employees would take a 10% pay cut to continue working from home.68

In the medium to longer term, organizations will have to adjust their fundamental talent use and acquisition strategies. Sourcing professionals must be positioned to assist with adjustments to purchasing strategies around the use of recruiting agencies, hiring portals, process management technologies and new supplier capabilities, including RPO applications. And, talent acquisition strategies should be developed and coordinated with other talent needs, such as temporary and contingent labor, in order to move toward a more unified total talent strategy.

HR Benefits

Health care costs are expected to rise rapidly in 2020, and employers could face significant cost increases as a result of the pandemic. Despite precautions and lockdowns, the number of coronavirus cases has been rising in the United States and is putting tremendous pressure on its health care system. Preliminary estimates are that the employer cost per infection could vary anywhere from less than $1000 for a mild case to $100,000 for an acute case requiring a stay in the intensive care unit.69 As many U.S. companies are self-insured, these costs will likely result in an overrun of health care budgets, or out-year cost increases in premiums for fully insured companies. Even after social distancing guidelines are relaxed, it is highly recommended that companies encourage their employees to work from home for an extended period — especially for employees with chronic conditions — to reduce the possibility of infections and minimize employee health concerns as well as health care costs.

Alarming statistics, like the one highlighted by the Federal Reserve stating that 40% of Americans struggle to come up with $400 for unexpected expenses, will come to bear in the current situation.70 More employers will need to rethink and develop a financial wellness strategy with customizable programs to meet the unique needs of a post-pandemic world further colored by a multigenerational workforce.

In the longer term, the trend of employers contracting directly with doctors and hospitals to provide better-quality and lower-cost care will likely see an uptick. Cost pressures will also challenge health care providers to transition from traditional fee-for-service (FFS) care models to value-based care (VBC). VBC models are intended to reduce total health care costs in the long term as they place more emphasis on managing the patient’s condition and outcomes more effectively.

Other examples of fundamental shifts in health care coverage and provision are the increased use of telehealth and remote care services for precaution, prevention and treatment.71

Sourcing professionals involved in health care and benefits buying must be positioned close to business stakeholders to evaluate and address short-term impacts on sourcing plans and supplier costs. This includes helping source and evaluate benefit carrier offerings, as well as applying effective supplier relationship management to existing brokers and HR consultants to reduce risks and offer creative solutions for future needs.

Legal Services

The global legal services market reached a value of over $766 billion in 2019, having grown at a compound annual growth rate (CAGR) of 5.4% since 2015.72 Through 2023, this market was expected to grow at a CAGR of 6.5%, to nearly $987 billion.73 Going into 2020, many law firms, especially the elite AmLaw100 cadre, had been running at high capacity and pushing through annual rate hikes more aggressively after a period of stagnation following the 2008 recession.

Given the breadth of the challenges that corporations (and humanity) are now facing, we expect that demand for legal services will rise dramatically except in niche practice areas such as intellectual property and environmental law. Key areas of growth will include:

- Contract Law

Expected increase in matters relating to force majeure and third-party indemnities as entire supply chains are disrupted - Employment/Labor Law

Demand will spike as layoffs and furloughs continue. Benefit entitlement issues will be numerous and more complex as employers and employees try to make sense of their rights based on federal relief programs that vary by state and municipality - Corporate Law

Demand for restructuring support and bankruptcy proceedings will increase as smaller or highly leveraged businesses run out of working capital - M&A

Large deals will stall because of heightened uncertainty in the short term; however, we can expect a significant uptick in small- and mid-sized deals as more distressed firms put themselves up for sale and cash-rich competitors seize these opportunities. Look for more acquisitions in the legal sector as the trend towards consolidation continues and accelerates

In general, the legal market will see a surge in activity in the next few quarters that will put a premium on top lawyers’ time and experience. Companies should partner strategically and collaboratively with their top advisors while leveraging in-house staff and mid-tier firms where possible to mitigate capacity risks and to manage growing caseloads efficiently.

Looking Ahead

Once economies start to emerge from the pandemic, we believe that substantial opportunities to adapt internal and external GPS supply strategies will arise due to fundamental shifts in business operations and risk management considerations. Procurement must be positioned to take advantage of greater organizational appetite to find supply alternatives, build flexibility into the supply chain, and apply lean operating principles by re-engineering sourcing strategies and adopting greater total cost savings approaches.

Market Opportunity — General and Professional Services

| Category | Subcategory | Immediate | 3-6 months | Beyond |

|---|---|---|---|---|

| Consulting / Professional Services | All | Leverage short-term needs for reduced pricing, greater risk-sharing deals Manage project staffing to ensure appropriate resources |

Negotiate reduced pricing, greater risk-sharing deals Manage project staffing to ensure appropriate resources Kick off new preferred partnering discussions |

Resource attribution in some firms Increased M&A activity Leverage preferred relationships |

| Contingent / Temporary Labor | All | Resolve supply continuity issues, find alternative labor channels, preferred partnering, short-term demand management | Develop alternative supply channels (plan, pilot, expand) Automation and lean operating planning Preferred supply strengthening |

Apply and expand alternative supply channels Automation Preferred partnering Assist business to drive lean operating principles |

| HR / Recruiting | All | Assist the business in managing in-flight projects and mission disruptions/needs Assist with supplier partnering/ engagement to meet criticalities |

Close alignment with business stakeholders on short- and longer-term adaptations to process and supplier needs Support consideration of new solutions and suppliers |

Close partnering and working with business stakeholders to adapt fundamental staffing and recruiting strategies and processes Develop tools and suppliers to deliver new environment with appropriate SLAs, KPIs, process management |

| HR Benefits | All | Identify employees with chronic conditions and send targeted communications to help protect them from COVID-19 infection | Initiate health care budgeting early and consider benefit plan programming / sourcing timelines Plan new strategies and mitigations |

Comprehensive adaptation of benefit offerings incorporating new carrier plans, new employee base demographics or sizing, new staff working models Holistic health and financial planning to improve overall health and well-being of employees |

| Legal | All | Select spot buy opportunities exist; look to enter into risk-share options if under extreme pressure | Business as usual Anticipate some price increases in M&A or bankruptcy service offerings |

Expect increase in M&A activities Anticipate some price increases in M&A or bankruptcy service offerings |

LOGISTICS

For logistics, 2019 was a year of uncertainty, but now 2020 has become a year of unprecedented challenges. According to an IMF report released in October 2019, global growth was expected to be 3% in 2019 — down from 3.6% in 2018, mostly because of damage caused by protectionism.74 In addition to a synchronized global slowdown, procurement managers were forced to deal with supply chain distortion due to capacity issues, economic tariffs and Brexit-related fears. Despite these uncertainties, cost increases were moderate compared to the prior year because of softening demand.

Now, 2020 is a whole new ball game. Economic shutdowns due to the pandemic, fuel price uncertainty, regulatory shifts, and the looming fear of a prolonged global recession are all key drivers that affect this year’s logistics outlook.

After several quarters of significant rate increases, 2019 provided cost relief not witnessed in the previous 12 to 18 months. However, the first quarter of 2020 added a new catalyst for uncertainty — the coronavirus outbreak. The virus has manipulated supply and demand while obscuring procurement forecasts, and will play a significant role in influencing the way logistics managers utilize transportation modes within their global supply chain network.

Road Freight

2019 saw an easing for shippers both in terms of finding capacity and keeping downward pressure on spot rates, after 2018 saw record peaks in demand. After two consecutive years of significant rate increases, in 2019 there was moderate price relief of 4–7%.75 As we began 2020, our initial forecast models indicated some tightening in the market with rate increases forecasted to kick off in Q2, but the pandemic has caused substantial market upheaval, leading to fluctuations in costs, capacity levels and demand.