Chemical Procurement in 2025: Five Trends You Cannot Ignore

- Chemicals companies are involving procurement in R&D at the design stage of product development to identify potential bottlenecks.

- As part of a larger risk mitigation strategy, they are diversifying their supplier base to reduce geographic and operational exposures at the plant level.

- Instead of maintaining buffer stock, manufacturers now engage in selective stockpiling with the help of predictive analytics and digital tools.

August 29, 2025 | Procurement Strategy 7 minutes read

How has procurement changed five years after the COVID-19 pandemic disrupted global supply chains? While early pandemic responses such as panic buying and fragmented sourcing have faded, new behaviors born from crisis are here to stay.

In several industries, procurement has evolved from firefighting to foresight – stepping in earlier to act proactively.

GEP sees five strategic shifts shaping the future of chemical procurement: integrated risk planning, intelligent safety stockpiling, purposeful supplier diversification, real-time data usage, and the usage of Buy, Hold, Sell inventory orchestration framework.

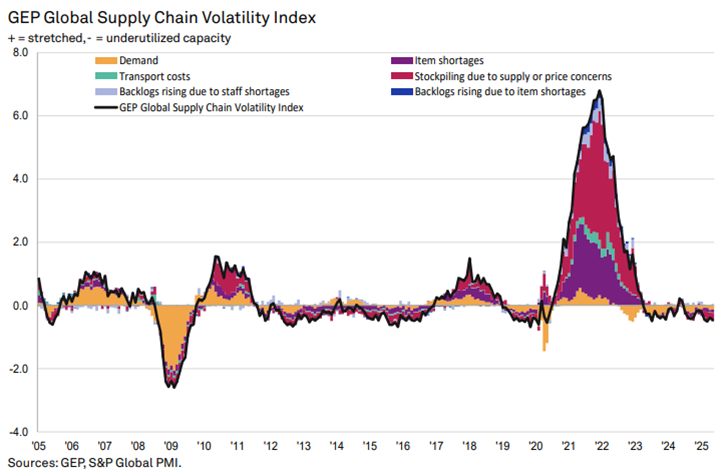

This article draws on interviews with procurement leaders from two global chemical manufacturers (names withheld) and insights from GEP’s proprietary tools like the Supply Chain Volatility Index and the Buy | Hold | Sell inventory orchestration framework (BHS Framework).

Procurement is Playing an Increasingly Strategic Role

Learn How to Align Procurement with Business Goals

From Crisis to Command: Why Procurement Can’t Go Back

COVID didn’t just disrupt supply chains. It exposed the limits of a cost-only procurement model. In the chemical sector, buyers found themselves chasing containers, revisiting suppliers they had deprioritized, and facing production stops not because of cost, but because of blind spots.

The takeaway is clear: the old playbook — optimize prices, negotiate hard, manage later — is no longer viable. The companies that came out ahead weren’t just digital or diversified, but the ones who redefined procurement as a risk orchestration function, engaging R&D early, and treating supplier intelligence as a strategic asset.

Going forward, maintaining operational continuity and real-time insight must become procurement’s new default settings, not reactive responses.

1. Early-Stage Risk Planning Through Procurement–R&D Collaboration

The pandemic taught procurement the cost of being reactive. GEP has since supported many clients in embedding procurement at the design stage of product development, particularly for regulated substances identifiable at the Chemical Abstracts Service (CAS) level, where sourcing constraints and compliance risks are higher.

Early involvement allows for dual sourcing qualification, better supplier alignment, and proactive mitigation of supply bottlenecks. As one global category manager at a leading chemical manufacturer explained during a GEP interview in March 2025: “We are now involved in the R&D stage right from the beginning. It’s no longer just about price—it’s about continuity.”

By contrast, delaying procurement involvement or failing to assess upstream risks often results in supply constraints, last-minute changes, or costly requalification processes. These reactive fixes ultimately increase the Total Cost of Ownership (TCO), making early collaboration not just strategic, but financially sound.

2. Intelligent Buffer Strategies Over Panic Stockpiling

During COVID, many manufacturers faced unexpected disruptions in supply — including being allocated limited quantities of raw materials by their suppliers due to overall shortages. As a result, even long-term partners could no longer fulfill full order volumes, forcing buyers to hold excessive buffer stocks as a protective reflex. While understandable during crisis, this approach proved financially and operationally unsustainable.

According to the GEP Supply Chain Volatility Index, inventory accumulation is now at its lowest level since 2016. Buyers have shifted to selective stockpiling, informed by geopolitical risks and supply chain analytics.

As one global procurement leader at a pharmaceutical company explained during a March 2025 GEP interview, reflecting a broader trend across the industry: “We don’t stock more because we’re scared. We stock smarter because we know more.” This shift followed a multi-year transformation program supported by GEP, combining predictive analytics, supplier segmentation, and regional buffering strategies — particularly in North America and APAC.

The emphasis is no longer on volume, but on value-at-risk. Companies use digital tools to simulate disruption scenarios and identify which specific feedstocks or intermediates merit additional buffers and where buffers can be safely reduced.

In chemical procurement, this matters even more: shortages in one CAS-level precursor can paralyze entire product lines. Intelligent buffering allows companies to prioritize continuity while preserving working capital.

Some U.S.-based firms continue to maintain strategic stockpiles in response to Trump-era tariffs and evolving trade policy — a trend tracked via GEP’s Tariff Resource Center, which enables clients to dynamically adjust stock levels based on regulatory outlook.

3. Supplier Diversification with Geopolitical Awareness

The term "supplier diversification" has evolved. It now includes geographic, regulatory, and ownership exposure.One global manufacturer supported by GEP restructured its sourcing strategy to localize procurement near production plants and reduce overdependence on any single country.

Simultaneously, industry consolidation, such as DSM–Firmenich, Celanese–DuPont, and LANXESS–DSM, has reduced the number of distinct supply sources available.

One global procurement lead at a GEP chemical sector client summarized the evolving mindset during a March 2025 interview: “It’s no longer enough to know who your supplier is. You need to know where they manufacture, how, and under what risks.”

This insight reflects a broader shift observed across the industry. In recent GEP engagements, companies have increasingly moved beyond Tier-1 visibility to assess geographic, regulatory, and operational exposures at the plant level. GEP supports this transformation by helping clients map hidden dependencies and implement true dual sourcing — not only by supplier name, but by ownership structure and physical location.

Across recent client engagements in the chemical and life sciences sectors, GEP is observing tangible acceleration in nearshoring and regional dual-sourcing strategies.

What was once considered a long-term ambition is now being integrated into current sourcing decisions — not just for finished products, but at the intermediate and feedstock levels.

We’re seeing more procurement teams apply regional risk scoring during supplier selection and uncover cases where dual sourcing arrangements unintentionally rely on common upstream nodes. This shift highlights the growing need for procurement to gain visibility beyond Tier-1 suppliers, into Tier-2 and Tier-3 dependencies. Without this depth, supply resilience may appear robust but can prove fragile under pressure.

4. Predictive Procurement Powered by Real-Time Data

The chemical industry is increasingly embracing predictive procurement and using data to foresee disruptions and adapt proactively. GEP SMART, powered by the GEP Quantum AI engine, enables buyers to dynamically analyze risks and performance using real-time data. Through customizable dashboards and AI-assisted queries, teams can surface actionable insights related to energy price swings, logistics bottlenecks, supplier lead times, or market shifts.

For regulatory risks, GEP SMART integrates compliance and third-party risk management tools that track updates to certifications, ESG standards, and emerging regulations, including changes that may affect specific raw materials identified by their Chemical Abstracts Service (CAS) numbers.

As noted by a global category manager during a March 2025 GEP interview: “We track signals on volatile chemicals like butyl acetate or isopropanol and adjust sourcing windows accordingly.” –

As future disruptions become more localized — driven by CAS-level regulatory decisions, regional energy volatility, or targeted policy shifts — predictive visibility will become increasingly vital. Without real-time data and systems, buyers risk reacting too late in increasingly granular and fast-moving environments.

5. Inventory Orchestration with GEP’s Buy | Hold | Sell Framework

Managing strategic or high-value raw materials often means balancing capital exposure with supply assurance. This is where GEP’s Buy | Hold | Sell (BHS) framework solution provides a strategic approach.

Acting as an intermediary, GEP can hold materials, finance supplier payments, and manage receivables, enabling clients to access critical stock without tying up cash flow.

How the BHS framework benefits chemical procurement:

- Lower working capital: Reduces the cash conversion cycle from 10–14% to as low as 2%.

- Improved visibility: Forecasting tools and supplier coordination reduce excess inventory and avoid shortages.

- Operational simplicity: GEP handles supplier, logistics, and payment orchestration, especially useful when managing volatile, high-stakes commodities.

The Buy | Hold | Sell inventory orchestration framework enables companies to secure sensitive materials while preserving balance sheet health, effectively balancing supply assurance with capital efficiency. For chemical procurement teams, it’s a powerful lever to maintain both operational continuity and financial agility in today’s high-risk environment.

Chemicals Procurement Isn’t the Same Today

Learn New Sourcing Strategies and Priorities for the Chemicals Sector

From VUCA to BANI: Redefining Procurement Resilience

Procurement leaders today no longer operate in a merely volatile world. They face a system that is brittle, anxious, nonlinear, and incomprehensible — a BANI world. The traditional tools of supplier consolidation and cost optimization no longer suffice. Procurement must adapt to:

- Raw material shocks without historical precedent,

- Sudden regulation shifts,

- Tariff impacts,

- And rising organizational and data complexity.

According to GEP’s Supply Chain Volatility Index (May 2025), global supply chains appear calmer but beneath the surface, signs of fragility are emerging. Activity across Asia has slowed sharply, particularly in manufacturing hubs impacted by ongoing tariff tensions. Meanwhile, North American companies are beginning to front-load inventories in anticipation of policy shifts, and European supply chains remain underutilized, despite early signals of recovery in core markets.

This apparent slowdown should not be misread as stability. Rather, it points to a fragile balance: with lower safety stock levels, leaner inventories, and tighter margins, procurement teams now operate with reduced buffers and shorter response windows.

In this environment, the absence of disruption does not equal resilience. On the contrary, it increases the need for predictive analytics, proactive planning, and cross-tier visibility. Procurement must deliver continuity not by reacting to shocks, but by anticipating them before they occur.

How Leading Companies Are Redesigning Procurement for a New Era

The shift toward resilient, capital-efficient procurement is no longer aspirational — it’s currently happening. Across the entire chemical industry, leading companies are rethinking how procurement contributes to business continuity, cost control, and risk management.

For example, several GEP clients have restructured their sourcing strategies to enable dual sourcing, reduce exposure to geopolitical disruptions, and improve their ability to respond to market volatility. These transformations were not driven by generic digitalization efforts, but by targeted initiatives grounded in predictive analytics, cross-tier visibility, and smarter inventory orchestration.

These shifts are enabled by integrated platforms and tools designed to address real buyer concerns like balancing agility with cost control, gaining early visibility into supply risk, and ensuring continuity without overstocking.

Rather than relying on reactive firefighting, these companies are building procurement functions equipped to anticipate and act — with a clear focus on resilience, precision, and long-term value creation.